Editorial notice: Reviewed for underwriting accuracy by the RJI Institutional Review Team | Published: May, 2026 | Last reviewed: June, 2026

Rescue Difficulty in High-Elevation Underwriting is an important insurance concern for occupations involving towers, offshore structures, bridges, wind turbines, and other elevated environments where emergency extraction may be delayed.

Executive Summary

Rescue difficulty is a major underwriting concern in elevated occupations because delayed emergency response can significantly increase injury severity, permanent disability exposure, and fatality risk. Insurers often apply stricter underwriting to workers on remote towers, offshore structures, bridges, wind turbines, and isolated elevated environments where emergency extraction may be difficult or delayed. Rescue Difficulty in High-Elevation Underwriting affects how insurers evaluate emergency extraction delays, offshore evacuation exposure, and catastrophic disability severity in elevated occupations.

The “Golden Hour”: Why Your Location Changes Your Rates

In emergency medicine, the “Golden Hour” is the critical window during which rapid treatment is most likely to prevent permanent disability. Insurers know that if you are on a remote tower or offshore rig, your “Golden Hour” might be spent just waiting for a transport team.

When an underwriter sees “High Rescue Difficulty,” they aren’t just looking at a height; they are calculating how much more likely you are to suffer a career-ending injury because help couldn’t reach you in time. This is why premiums for remote workers are higher than for those on urban sites; you are essentially paying for the “rescue gap”.

What Is Rescue Difficulty in Insurance Underwriting?

In insurance underwriting, rescue difficulty refers to how hard it may be to quickly reach, stabilize, and transport an injured worker after a fall, collapse, medical emergency, or equipment incident in an elevated work environment. Insurers evaluate the difficulty of the rescue because emergency delays often increase the severity and cost of occupational injury claims.

This includes situations involving:

-

Tower rescues

-

Offshore platform evacuations

-

Bridge rescues

-

Wind turbine extractions

-

Confined elevated industrial structures

-

Remote elevated maintenance operations

For example, a worker injured on a downtown construction site may receive emergency treatment within minutes. A worker injured hundreds of feet above ground on a remote communications tower or offshore structure may face much longer rescue timelines.

Key Rescue Factors Insurers Evaluate

From an underwriting perspective, insurers evaluate:

-

How quickly can injured workers be reached

-

Whether specialized rescue equipment is available on-site

-

How difficult physical extraction may be

-

How long does transport to a Level 1 trauma care facility (advanced emergency trauma center) take

-

Whether regional weather conditions consistently delay rescue operations

The harder the rescue environment becomes, the greater the insurer’s concern about severe claims. This underwriting logic closely connects with broader elevated-risk classification systems explained in Height Exposure Underwriting: How Insurers Evaluate Elevated Workers.

Why Rescue Difficulty in High-Elevation Underwriting Matters to Insurers

Insurers evaluate rescue difficulty because delayed emergency response can significantly increase claim severity, disability exposure, rehabilitation costs, and fatality risk in elevated occupations.

Why Do Rescue Delays Increase Insurance Risk?

Insurers are highly concerned about rescue delays because injury severity often worsens when workers cannot receive rapid medical treatment. A serious fall may initially be survivable, but delayed extraction can increase complications such as:

-

Spinal trauma deterioration

-

Internal bleeding

-

Shock

-

Hypothermia exposure

-

Crush injuries

-

Oxygen deprivation

-

Traumatic brain injury complications

Worker’s Note: The 20-Minute Clock

Even if your harness saves your life in a fall, Suspension Trauma (blood pooling in the legs) can become fatal in as little as 10 to 20 minutes if you aren’t rescued or transitioned to safety. Underwriters actively look for “Self-Rescue” training, rescue times under 15 minutes, and relief straps in your company’s safety profile. If you can prove you have the tools to keep yourself stable while waiting for a crew, you are viewed as a lower risk, which helps justify better policy terms.

Worker’s View: The “Waiting Period” Trap

If you work in a remote or elevated environment like an offshore platform or a wind turbine, a standard disability policy might force you to wait 30 to 90 days longer before your monthly payouts kick in compared to a ground-based mechanic.

Why? Insurers assume your medical recovery will take longer because of the initial rescue delay. When shopping for personal coverage or reviewing your company’s benefits, always check the Elimination Period (the waiting window), don’t just look at the baseline premium.

A fall injury that may be survivable in an urban construction environment can become far more severe if rescue crews cannot quickly reach a worker on a remote tower or offshore structure. Insurers specifically evaluate:

Critical Policy Gap

This physical delay creates a distinct financial exposure known as an Evacuation-Only Gap, where an insurer will cover the ultimate hospital bills but entirely exclude the six-figure cost of the helicopter or specialized rigging team required to get the worker off the structure. For a deep dive into how to audit your policy for this hidden void, read our full analysis on Evacuation-Only Gaps in High-Risk Commercial Insurance.

Delayed Medical Treatment

The longer emergency treatment is delayed, the greater the probability of severe, permanent disability exposure.

Weather-Related Rescue Delays

Storms, high winds, lightning, rough seas, or heavy rain can completely ground helicopter operations or delay marine rescue crews.

Helicopter Access Problems

Many elevated offshore jobs depend heavily on helicopter extraction. If helicopters cannot safely operate, evacuation timelines may increase substantially.

Confined Rescue Environments

Workers trapped inside turbines, narrow bridge structures, or industrial towers may require specialized technical rescue teams.

Fatality Exposure

Insurers recognize that inaccessible rescue environments increase fatality probability during catastrophic incidents.

From an underwriting standpoint, the relationship is direct:

This severity relationship is also closely tied to concepts explained in Catastrophic Fall Risk in Occupational Insurance and Fall Severity Modeling in Disability Insurance.

How Do Insurers Evaluate Rescue Complexity?

Insurers typically analyze several underwriting factors when evaluating rescue difficulty exposure.

How Rescue Time Changes Underwriting Severity”

| Rescue Window | Underwriting Interpretation |

|---|---|

| Under 15 min | Lower catastrophic severity concern |

| 15–30 min | Elevated disability exposure |

| 30–60 min | Significant claim severity concern |

| Over 60 min | High catastrophic underwriting exposure |

Common Rescue Complexity Tiers

| Rescue Tier | What it Means for You | The Insurance Impact |

| Tier 1: Ground Access | An ambulance can drive directly to your side in under 15 minutes. | Lowest premiums; standard disability terms. |

| Tier 2: Technical Access | Requires specialized rope teams or high-angle extraction gear to reach you. | Increased “Life & Limb” surcharges on most policies. |

| Tier 3: Remote/Aerial | Extraction depends entirely on weather windows and helicopter availability. | Stricter “Waiting Periods” before disability pay begins. |

| Tier 4: Confined/Extreme | You are trapped inside a structure, such as a turbine nacelle or bridge pylon. | Possible “Occupational Exclusions” for specific high-hazard tasks. |

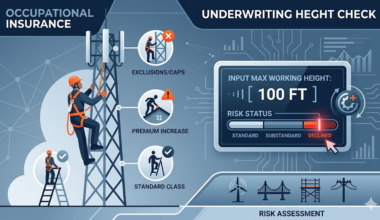

Why Working Height Matters

Very high structures increase both fall severity and rescue difficulty. Reaching injured workers safely may require specialized climbing teams or aerial extraction.

As working height increases, insurers may impose stricter eligibility rules, policy limitations, or occupational restrictions, as explained in Height Restrictions in Occupational Insurance Policies.

Why Remote Locations Increase Underwriting Concern

Insurers evaluate how far workers are from hospitals, trauma centers, and emergency responders. Remote industrial operations often receive stricter underwriting because rescue timelines may be unpredictable.

Why Offshore Work Receives Extra Scrutiny

Offshore evacuations frequently depend on helicopter availability, volatile weather windows, marine rescue support, and limited on-site offshore medical facilities. If evacuation systems fail or become delayed, claim severity can escalate rapidly. These underwriting issues are heavily connected to Offshore Risk Underwriting.

Which Occupations Have High Rescue Difficulty Exposure?

Some elevated occupations consistently receive additional underwriting scrutiny because emergency extraction may be difficult or delayed.

Tower Climbers

Workers on communications towers often operate at extreme heights in isolated locations where rescue access is difficult.

Tower operations represent one of the clearest examples of rescue-difficulty underwriting because extreme working heights, limited access routes, and delayed emergency extraction can materially increase claim severity, as discussed in Tower Climbers Insurance.

Wind Turbine Technicians

Wind turbines often involve confined internal ladders, remote terrain, and difficult extraction conditions.

These rescue challenges closely align with the underwriting concerns examined in Wind Turbine Technicians Insurance, where insurers evaluate the combined impact of height exposure, confined access, and remote rescue limitations.

Offshore Maintenance Workers

Offshore structures often depend entirely on helicopter evacuation during emergencies.

Bridge Workers

Large bridge systems often create complicated rescue environments involving suspended structures and difficult equipment access.

Bridge operations often combine elevated work, suspended access systems, environmental exposure, and complex rescue logistics, all of which influence underwriting decisions, as examined further in Bridge Workers Insurance.

Structural Steel Erectors

Structural steel erectors work on partially completed buildings, bridges, and industrial frameworks where suspended steel, crane-assisted construction, and limited rescue access significantly increase catastrophic injury exposure. Insurers evaluate these operations for elevated fall severity, complex rescue logistics, and structural access challenges, as explored in Structural Steel Erector Insurance.

Offshore Ironworkers

Heavy offshore structural work combines fall exposure with delayed emergency access.

This combination of structural steel work, offshore evacuation dependency, and catastrophic fall exposure creates a particularly challenging underwriting profile, as explored in Offshore Ironworkers Insurance.

Utility Linemen

Linemen frequently work in remote storm conditions where rescue operations become hazardous.

Elevated Offshore Crane Operators

Crane operators on offshore platforms may work far from trauma care facilities.

Remote Industrial Workers

Workers on isolated industrial infrastructure may face major evacuation delays during severe incidents.

These occupational classifications are part of broader insurer risk systems explained in Occupational Hazard Classification in Insurance.

How Does Rescue Difficulty Affect Insurance Coverage?

Rescue-risk exposure directly affects underwriting decisions and policy structure.

Higher Premiums

Insurers charge more because delayed rescue environments increase the financial probability of severe claims. This pricing structure closely connects with Why Elevated Workers Pay More for Insurance, where insurers evaluate how rescue delays increase catastrophic claim severity exposure.

Stricter Underwriting

Applicants face more detailed occupational questionnaires and extensive medical review requirements.

Occupational Exclusions

Some policies may completely exclude certain offshore, climbing, or elevated duties.

Disability Insurance Restrictions

Insurers may reduce available monthly disability benefits for workers in difficult rescue environments.

Policy Caps

Total coverage limits may be reduced due to elevated catastrophic claim exposure.

Waiting Periods

Disability policies regularly impose longer waiting periods before benefit payouts begin.

Limited Carrier Availability

Certain standard commercial insurers avoid extremely difficult rescue-risk occupations altogether.

Underwriting decisions often become significantly stricter when difficult rescue environments combine with additional risk factors such as offshore exposure, extreme heights, severe weather operations, or prior injury history. At certain severity thresholds, insurers may reduce available coverage, impose occupational exclusions, require full medical underwriting, extend waiting periods, or decline coverage entirely.

Severe Claim Concerns

Insurers understand that delayed rescue situations can lead to permanent impairment, long-term disability, high rehabilitation costs, major income-loss claims, and fatality exposure. This is why rescue complexity often influences both pricing and eligibility decisions.

Why Do Offshore and Remote Elevated Jobs Receive Extra Insurance Scrutiny?

Rescue Difficulty in High-Elevation Underwriting becomes significantly more severe when elevated work is combined with offshore evacuation dependency and remote emergency-response limitations.

Offshore and remote elevated operations combine several underwriting concerns simultaneously. These environments often involve helicopter evacuation dependency, severe weather exposure, long transport times, isolation from trauma centers, limited rescue infrastructure, and delayed emergency response capability.

For insurers, this creates elevated uncertainty during catastrophic injury events. A worker injured onshore near emergency services may receive trauma care within minutes. An offshore worker may wait significantly longer due to weather conditions, aircraft limitations, or transport logistics.

Underwriters, therefore, view remote elevated work as carrying both high injury severity exposure and high rescue-complexity exposure. This combination frequently results in stricter underwriting outcomes.

Real-World Underwriting Examples

-

City Roofer vs. Offshore Tower Technician: A city roofer has rapid ambulance access and nearby trauma care. An offshore tower technician may require helicopter extraction from a remote structure during difficult weather conditions. Insurers assign a higher severity concern to the offshore role because rescue delays worsen injuries. Although roofers usually operate closer to emergency response infrastructure than offshore workers, insurers still classify roofing occupations aggressively because elevated fall frequency remains extremely high. This classification logic is explored further in Why Roofers Face Strict Insurance Underwriting. When serious falls occur, insurers closely examine injury severity, rescue timelines, employer safety compliance, and claim documentation during the adjustment process, as explained in Commercial Roofing Insurance Claims Process.

-

Urban Bridge Worker vs. Remote Wind Turbine Technician: Urban bridge workers operate near municipal emergency infrastructure. Remote wind turbine technicians may work hours away from advanced trauma care. The remote technician receives stricter underwriting scrutiny.

-

Warehouse Maintenance Worker vs. Offshore Platform Worker: A warehouse maintenance worker injured indoors receives immediate emergency response. An offshore platform worker depends entirely on marine or helicopter evacuation. Evacuation limitations significantly increase claim severity.

-

Utility Worker Near a City vs. Utility Worker in Storm-Damaged Areas: Urban utility crews have nearby support systems. Rural storm-response workers operate in isolated areas with blocked access routes and delayed rescue capability. Insurers classify the remote worker as carrying greater rescue-risk exposure.

How Rescue Difficulty in High-Elevation Underwriting Affects Disability Insurance Claims

Disability insurers evaluate not only whether injuries occur, but also how severe those injuries may become after a delayed rescue. When emergency extraction takes longer, injuries worsen, recovery periods increase, permanent impairment risk rises, rehabilitation becomes more expensive, and long-term income-loss exposure grows. This is one reason insurers closely connect delayed rescue environments with Permanent Disability Risk from Elevated Work.

For example, spinal injuries that receive immediate treatment produce better recovery outcomes than injuries involving delayed extraction and transport. From a disability underwriting perspective:

This underwriting logic directly affects disability eligibility, monthly benefit limits, occupational classification, premium pricing, and policy restrictions. These concerns are closely connected to broader disability severity systems explained in Disability Insurance for High-Risk Workers.

How Do OSHA Emergency Planning Systems Affect Underwriting?

Insurers evaluate rescue preparedness because strong emergency systems reduce claim severity exposure. Underwriters review rescue plans, evacuation procedures, fall-protection systems, emergency communication networks, rescue training programs, emergency drills, and employer preparedness documentation.

Insurers are not simply evaluating safety compliance; they are evaluating whether injured workers can realistically be rescued quickly enough to reduce catastrophic claim severity. Insurers also evaluate whether employers follow established OSHA fall-protection and rescue-planning standards during elevated operations, as discussed in OSHA Fall Protection Standards for High-Risk Work. Strong emergency planning improves underwriting outcomes because insurers view organized rescue capability as reducing financial uncertainty during severe incidents.

Insurers also review prior OSHA fall-protection violations because repeated safety failures may indicate elevated rescue-risk exposure and poor emergency preparedness systems. These underwriting concerns are explained further in OSHA Fall Violations and Insurance Costs.

How Employers Can Improve Rescue-Risk Underwriting Outcomes

Insurers use “desk logic” unless you provide them with real-world field data. If your business operates in high-rescue-difficulty environments, you can actively pull your company out of a high-premium tier by providing a Rescue Preparedness Packet with your insurance application.

Why Does Misclassification Create Problems in Rescue-Risk Occupations?

Misclassification is a major underwriting concern in elevated rescue-risk occupations. Failure-path examples include:

-

Undisclosed tower work

-

Omitted offshore duties

-

Hidden remote assignments

-

Inaccurate occupational descriptions

-

Undisclosed helicopter-dependent operations

-

Unreported subcontract elevated work

Insurers investigate severe claims involving difficult rescues very closely because catastrophic claims involve substantial financial exposure. If occupational duties were inaccurately disclosed during application review, insurers investigate classification accuracy, job-duty disclosures, policy eligibility, underwriting representations, and employer reporting consistency. This is one reason claim disputes occur in hazardous occupations. These issues strongly connect with topics discussed in Common Reasons Claims Are Denied for Risk Jobs.

How Can Workers and Employers Reduce Underwriting Problems?

Workers and employers can improve underwriting perception by demonstrating strong rescue preparedness and accurate occupational disclosure. Helpful measures include:

-

Accurate occupational descriptions

-

Documented rescue planning

-

Rigorous emergency-response training

-

Offshore evacuation procedures

-

Maintained rescue certifications

-

Full fall-protection compliance

-

Regular emergency drills

-

Strong communication systems

-

Updated evacuation protocols

Insurers respond more favorably when employers demonstrate organized emergency preparedness systems. This does not eliminate risk exposure, but it reduces underwriting concerns surrounding catastrophic rescue delays.

Frequently Asked Questions

I’ve never had an accident. Why is my premium still high?

Insurance pricing is based on the potential severity of a future claim, not just your personal safety record. If your job involves difficult rescue environments such as offshore structures, towers, bridges, or remote elevated worksites, insurers recognize that any serious incident has a higher mathematical probability of becoming a catastrophic disability claim. In many cases, you are paying for the complexity of the rescue environment as much as the physical job itself.

Does having an on-site rescue team help my insurance rates?

Yes. Employers that maintain documented, 24/7 rescue capabilities, emergency-response systems, and trained extraction teams can significantly reduce underwriting concerns. This is especially important in offshore operations, large bridge projects, and remote elevated environments where outside emergency responders take longer to arrive. Strong rescue preparedness improves carrier availability and reduces policy restrictions.

Will a rescue delay affect how my disability claim is paid?

A rescue delay does not automatically prevent a disability claim from being paid, but it affects how insurers structure your coverage. Longer extraction and transport times increase recovery periods, rehabilitation costs, and permanent impairment exposure. Because of this, insurers apply stricter waiting periods, lower monthly benefit limits, or additional underwriting controls for occupations involving difficult rescue environments.

Final Underwriting Insight

Rescue difficulty does not simply increase accident risk. It increases the probability that otherwise survivable injuries become permanent disability claims because emergency treatment cannot be delivered quickly enough. For insurers, rescue difficulty is not just a safety issue; it is a severity multiplier that fundamentally changes how elevated occupations are priced, classified, and insured.

Key Takeaways

-

Rescue difficulty is a major underwriting concern because delayed extraction increases injury severity and claim costs.

-

Remote elevated work receives stricter underwriting due to evacuation limitations and delayed emergency response.

-

Offshore, tower, bridge, and wind-energy occupations face additional insurance scrutiny.

-

Disability insurers evaluate how rescue delays worsen permanent impairment exposure.

-

Emergency preparedness systems improve underwriting perception by reducing rescue uncertainty.

-

Accurate occupational disclosure is critical because insurers closely investigate severe rescue-related claims.

-

Rescue complexity directly affects premiums, eligibility, policy restrictions, and carrier availability.

Institutional & Underwriting Reference

Institutional References

- Occupational Safety and Health Administration (OSHA) Fall Protection Standards — Federal fall-protection and rescue-planning standards used by insurers to evaluate elevated-work emergency preparedness, rescue capability, and employer safety systems.

- National Institute for Occupational Safety and Health (NIOSH) Traumatic Injury Research — Research on traumatic injury severity, emergency response limitations, occupational fatality exposure, and high-risk work environments relevant to underwriting severity modeling.

- Society of Professional Rope Access Technicians (SPRAT) — Technical rope-access and rescue-certification standards referenced in high-angle rescue environments involving towers, bridges, turbines, and industrial structures.

- Industrial Rope Access Trade Association (IRATA) — International rope-access operational and rescue standards commonly referenced in offshore and industrial elevated operations.

- American National Standards Institute (ANSI) Fall Protection Standards — Consensus standards related to fall protection systems, rescue planning, and elevated occupational safety procedures relevant to insurer risk evaluation.

- Bureau of Safety and Environmental Enforcement (BSEE) Offshore Safety Regulations — Offshore operational safety and emergency-response guidance affecting offshore evacuation risk and rescue-related underwriting concerns.

Reviewed for Underwriting Accuracy

This article was reviewed for underwriting relevance using the following elevated-risk insurance evaluation frameworks:

- Rescue-complexity severity modeling

- Offshore evacuation dependency analysis

- Disability severity exposure evaluation

- Occupational classification risk assessment

- Catastrophic fall-risk underwriting systems

- Emergency-response delay severity analysis

- High-angle rescue operational exposure review

- Remote-access claim escalation modeling

- Elevated occupational hazard classification systems

- Underwriting restriction and exclusion threshold analysis

Research & Underwriting Methodology

This article applies Risk Job Insurance’s elevated-risk underwriting methodology by analyzing how insurers evaluate rescue difficulty, delayed emergency response exposure, and catastrophic injury severity in high-elevation occupations.

The underwriting framework used in this article includes:

- Occupational hazard classification systems for elevated workers

- Rescue-delay severity escalation modeling

- Emergency extraction accessibility analysis

- Offshore evacuation dependency evaluation

- Catastrophic disability exposure assessment

- Trauma-response timing and claim severity analysis

- Underwriting restriction and exclusion frameworks

- Remote infrastructure and emergency-access evaluation

- Fall-severity and rehabilitation-cost modeling

- Employer emergency-preparedness assessment systems

The article also incorporates operational rescue realities commonly evaluated in offshore, tower, wind-energy, bridge, and remote industrial underwriting environments where emergency-response limitations may materially affect claim severity and long-term disability exposure.

Published: May 2026

Last reviewed: June, 2026.

Recommended Underwriting & Elevated-Risk Insurance Resources

For a deeper understanding of elevated-risk underwriting systems, see:

-

Height Exposure Underwriting: How Insurers Evaluate Elevated Workers

-

Offshore Risk Underwriting