Editorial notice: Reviewed for underwriting accuracy by the RJI Institutional Review Team | Published: June, 2026 | Last reviewed: June, 2026

————————————————————————————————————–

Executive Summary

Navigating the complexities of ironworker insurance underwriting requires an understanding of how carriers calculate extreme physical hazards. This occupation faces strict guidelines because it uniquely combines elevated structural work, severe fall exposure, heavy steel handling, crane interaction, and catastrophic injury potential. Insurers closely evaluate work height, structural environments, disability exposure, industrial construction severity, and safety history when determining pricing, eligibility, and coverage restrictions.

Ironworker insurance underwriting represents one of the most restrictive segments within the broader construction workers insurance market because carriers must account for elevated fall exposure, structural-collapse potential, crane interaction hazards, and long-tail disability risk.

What Ironworker Insurance Means in Practice

For ironworkers and contractors, insurance affects far more than premium costs. Coverage terms influence project eligibility, contract requirements, claim outcomes, and whether workers remain financially protected after a catastrophic injury.

Because ironwork combines elevated steel work, crane interaction, suspended loads, and severe fall exposure, many standard policies impose restrictions that are not fully understood until a claim occurs.

This explains why ironworker insurance underwriting differs significantly from roofing and general construction underwriting. Structural steel work combines elevated exposure, suspended loads, incomplete structures, and complex rescue conditions simultaneously, creating a severity profile that few other construction trades share.

Why Ironworkers Face Unique Physical Hazards

When an insurance company looks at a structural steel job site, it does not see standard construction. It sees an environment defined by extreme physical exposure. On any given shift, an ironworker experiences intense physical and environmental friction that sets their trade apart from almost all other fields.

[Height Exposure] + [Crane Interaction] + [Structural Instability] + [Weather Exposure]

│

▼

[Stacked Exposure System]

│

▼

[Extreme Underwriting Severity & Premium Hikes]

The Reality of Exposure Stacking

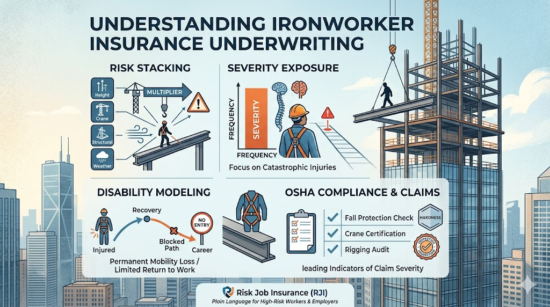

Most high-risk occupations face one or two major hazards. Roofers face fall risks; warehouse workers face heavy lifting hazards; heavy equipment operators face machinery risks. Structural steel projects, however, experience exposure stacking—they operate at the intersection of all these risk systems simultaneously.

An ironworker on a high-rise or industrial project may face severe fall exposure, crane-related hazards, unstable structural environments, heavy-material injuries, and long-term disability concerns all within a single shift.

This stacking effect multiplies the mathematical probability of an accident. If a sudden gust of wind occurs while a crane is positioning a multi-ton truss, the ironworker is exposed to a combined threat of a fall, a crush injury, and a structural collapse. Because these risks compound rather than occur in isolation, carriers model ironwork as a highly volatile exposure system.

How Insurers Classify Ironworkers

Not all ironwork carries the same level of risk, and underwriters use highly specific occupational classification codes to validate the risk level and match premiums to actual exposure. Workers’ compensation underwriting frequently relies on standardized classification frameworks developed by the National Council on Compensation Insurance (NCCI) to align occupational exposure with premium calculations and loss expectations.

These classification systems form part of the broader occupational class rating framework used by insurers to estimate expected losses, determine eligibility, and assign risk-based premiums across high-risk industries. This process is explored further in Occupational Class Ratings, which explains how insurers translate job duties into insurance pricing models.

These classification systems help insurers assign expected loss characteristics to specific occupations before a policy is priced or issued.

Insurers also reference standard federal tracking frameworks when evaluating structural steel exposure categories. For example, structural iron and steel workers are commonly associated with SOC Code 47-2221 within the Standard Occupational Classification (SOC) System, helping insurers align underwriting classifications with standardized labor-risk databases.

SOC 47-2221 encompasses a wide range of structural steel occupations, including bridge ironworkers, construction ironworkers, ornamental ironworkers, structural steel erectors, metal tank erectors, and wind turbine erectors. While these occupations share a common classification framework, insurers frequently apply different underwriting standards depending on work height, environmental conditions, rescue complexity, crane interaction, and catastrophic injury potential.

Once a worker is classified, the insurer must translate those real-world physical exposures into financial pricing models. In insurance terms, the structural ironwork hazard profile triggers a fundamental shift in how risk is calculated.

As working height increases, the insurer’s exposure shifts from Frequency Risk (minor, predictable injuries) to Severity Risk (rare but catastrophic injuries). For a low-rise carpenter, a slip might result in a sprained ankle—a frequency problem. For an ironworker on a high-rise skeleton or a bridge deck, a fall or structural collapse almost guarantees a fatality or a permanent, life-altering injury.

Because the financial cost of a single severity-risk claim can run into millions of dollars, commercial insurance carriers must enforce strict underwriting standards from day one. This concept is explored deeply in Height Exposure Underwriting: How Insurers Evaluate Elevated Workers, which establishes the foundational rules for how gravity alters insurance mathematics.

When analyzing these heights, underwriters look closely at the physics of a drop. The structural dynamics of a multi-story fall are modeled using specialized actuarial parameters outlined in Catastrophic Fall Risk in Occupational Insurance, which explains why insurers prioritize catastrophic claim exposure over routine injury frequency.

Ultimately, this mathematical shift directly impacts the commercial insured’s bottom line. The severe financial tail of these claims is the primary reason behind the pricing premium spikes detailed in Why Elevated Workers Pay More for Insurance, where premium structures are weighted heavily against high-severity trades.

Operational Factors That Increase Insurance Risk

Underwriters do not look at exposure in a static vacuum; they evaluate real-world operational variables that change the severity potential of a project.

-

Rescue Complications: If an ironworker suffers a medical emergency or becomes suspended in a safety harness at an extreme height, standard emergency medical services cannot simply walk over. Specialty high-angle rescue teams are required. This operational problem is explored further in Rescue Difficulty in High-Elevation Underwriting, where delayed extraction timelines directly alter fatality modeling and severity-risk calculations.

-

Weather Exposure: High winds, freezing rain, and extreme heat directly degrade physical grip, balance, and cognitive function, compounding structural instability risks.

-

Union vs. Subcontract Crews: Insurers often view union crews favorably due to standardized, mandatory apprenticeship and safety training programs. Conversely, heavily subcontracted crews face deeper scrutiny regarding safety enforcement consistency.

-

Owner/Operator Steel Contractors: Small firms where the owner is also on the steel are underwritten tightly. If the owner-operator is injured, the business loses both its primary worker and its management, spike-loading the risk of business interruption and long-term disability claims.

Common Reasons Ironwork Claims Are Denied

The primary failure path in ironwork insurance stems from inaccurate occupational disclosure. Because ironwork premiums are high, there is a dangerous temptation to misrepresent the work on insurance applications to secure lower rates.

[Undisclosed Bridge/High-Rise Work] ──> [Catastrophic Accident] ──> [Intense Claim Investigation] ──> [Claim Denial & Fraud Charges]

Common Failure Paths in Underwriting Disclosures:

-

Undisclosed Bridge or Industrial Work: Labeling a bridge project as a standard “low-rise commercial structural” job.

-

Hidden Subcontract or Crane Operations: Failing to disclose that the crew performs its own heavy crane rigging and crane interaction duties.

-

Understated High-Rise Duties: Telling an insurer that the company only builds up to three stories, then taking a contract for a ten-story building.

-

Occupational Class Downgrades: If an employer cannot clearly document that a worker splits time between ornamental work and structural work, the insurer will automatically downgrade the classification to the highest-risk category, applying the most expensive rates across the board.

Because ironwork claims involve such large sums of money, insurance companies deploy specialized investigative units to review catastrophic accidents. If they discover that the actual exposure was intentionally hidden or misclassified during evaluation, the insurer has the legal right to dispute the claim, deny coverage, cancel the policy retroactively, and pursue insurance fraud charges.

How Different Insurance Policies Evaluate Ironworkers

An ironworker’s risk is not viewed the same way across all insurance products. Different policy types evaluate the identical worker through different risk lenses:

Workers’ Compensation & Liability: Catastrophic Site Exposure

From an institutional underwriting standpoint, the greatest threat to a commercial insurance carrier’s portfolio is a correlated site event.

[Rigging/Bracing Failure] ──> [Structural Collapse/Crane Failure] ──> [Multi-Worker Catastrophic Claim]

Insurers evaluate structural collapse exposure and crane failures as correlated risks. If a crane drops a structural member or a temporary guy-wire snaps, it rarely affects just one person. It brings down sections of the iron framework, endangers the crane crew, impacts reinforcing crews below, and traps workers at height. This means a single site failure can instantly trigger multiple, simultaneous policy limits across workers’ compensation, general liability, and commercial umbrella coverages.

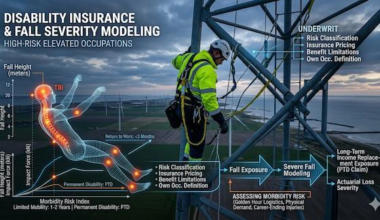

Disability Insurance: Career-Ending Logic

Disability underwriting focuses entirely on a single question: If this worker is injured, can they realistically return to their specific occupation? For a desk-bound professional, a broken leg or a fused vertebrae is inconvenient but rarely career-ending. For an ironworker, the same injury may permanently eliminate the worker’s ability to safely return to structural steel operations.

This underwriting framework closely connects with Fall Severity Modeling in Disability Insurance, where insurers evaluate how survivable injuries still create permanent occupational incapacity.

Disability underwriters evaluate the permanent physical demands of structural steel work, realizing that even minor physical degradations present a severe long-term threat to the worker’s career longevity. This specialized risk profile is detailed in Permanent Disability Risk from Elevated Work, which covers the specific physical limitations that bar high-elevation workers from returning to their trade:

-

Spinal Injuries & Fused Vertebrae: Eliminate the core flexibility needed to navigate steel beams.

-

Traumatic Brain Injuries (TBIs): Can permanently impair the fine motor balance required to walk a beam safely.

-

Orthopedic Destruction: Shattered ankles, wrists, or knees cannot withstand the heavy impacts and climbing demands of the job.

-

Limited Modified-Duty Opportunities: A structural steel contractor has very few light-duty roles. If an ironworker cannot walk the steel, they cannot work, forcing the claim to remain open as a long-term total disability payout.

Why Many Insurers Refuse Ironwork Risks

Because ironwork hazards are so extreme, the broader commercial insurance market reacts with aggressive structural boundaries, exclusions, and alternative risk placements.

The Specialty Shift

Many standard, well-known insurance carriers will completely decline to write a policy for an ironwork contractor. This restricted appetite stems from reinsurance sensitivity. Standard insurance companies purchase their own backup insurance (reinsurance) to protect against massive losses. Reinsurance treaties often contain strict exclusions against backing high-severity construction trades like structural ironwork, high-rise operations, and crane work.

As a result, the risk placement usually moves out of the standard market and into the specialized surplus lines market, where specialty underwriters build custom policies featuring higher premiums, larger mandatory deductibles, and tailored benefit structures.

Contractual and Project-Level Complexity

On large industrial or high-rise projects, insurers evaluate whether the site operates under an Owner Controlled Insurance Program (OCIP) or Contractor Controlled Insurance Program (CCIP). These wrap-up insurance structures centralize liability and workers’ compensation coverage across multiple subcontractors, significantly affecting how underwriters assess catastrophic exposure concentration.

This multi-employer environment creates severe liability ambiguity. If a structural connection fails during a lift, an immediate dispute arises: Was the crane rigged incorrectly by the subcontractor? Was the steel girder fabricated with a structural defect? Or did the general contractor fail to enforce proper site safety clearances?

Because of this interconnected liability risk, underwriters closely examine an ironwork contractor’s indemnity agreements and Hold Harmless clauses. Insurers require ironwork employers to maintain rock-solid contracts that clearly define where the steel erector’s liability ends and the crane operator’s or general contractor’s liability begins.

Policy Exclusions and Threshold Boundaries

To protect themselves, non-specialized insurance carriers insert strict limitations and exclusions into commercial policies. As detailed in Height Restrictions in Occupational Insurance Policies, a standard commercial policy may contain an absolute exclusion for any work performed above three stories or 36 feet. If an ironworker suffers a fall at 45 feet on an excluded policy, the claim can be denied, leaving the employer completely exposed to the loss.

Furthermore, policies may explicitly exclude work performed inside operating chemical plants, refineries, or heavy industrial facilities due to the added chemical and explosion hazards. Standard general liability and workers’ compensation policies also routinely exclude work over water or on marine vessels unless specialized maritime endorsements—such as those governed by the U.S. Longshore and Harbor Workers’ Compensation Act (LHWCA) or Jones Act coverages—are explicitly attached to the policy.

How Ironworkers and Contractors Can Improve Insurance Eligibility

While the underwriting environment for structural steel is naturally strict, employers and contractors can take proactive steps to lower their risk profile, secure better premium rates, and eliminate future claim disputes.

-

Provide Transparent Occupational Disclosures: Always document structural duties accurately. Clearly define the percentage of time spent on low-rise vs. high-rise, or structural vs. ornamental work, to prevent automatic premium downgrades.

-

Report Bridge and High-Rise Work Honestly: Ensure your policy explicitly permits the maximum working height and specialized environments your projects require before a worker ever steps onto the job site.

-

Maintain and Document Verifiable Training: Keep flawless records of ironworker certifications, qualified rigger credentials, crane operator licenses, and OSHA 30-hour cards. Insurers favor companies that can prove their workforce is highly trained.

-

Enforce and Audit Fall-Protection Compliance: Contactors should build rigid, documented safety cultures modeled after the OSHA Steel Erection Safety Guide, demonstrating internal safety audits focusing on harness inspections and tie-off compliance.

- Manage Regulatory History Impact: Insurers use historical safety data as a direct predictive indicator of future losses. This relationship is deeply examined in OSHA Fall Violations and Insurance Costs, which reveals how citation histories and worsening Experience Modification Rates (EMR) trigger immediate premium surges or policy non-renewals.

-

Proactively Update Insurers on Role Changes: If a business transitions from structural high-rise work to localized reinforcing or ornamental work, notify the broker immediately. Updating the insurer allows for a legitimate re-classification to a lower-cost risk tier.

Real-World Underwriting Scenarios

Scenario 1: Structural Ironworker vs. Warehouse Laborer

-

The Exposure: A structural ironworker bolts steel columns at 80 feet; a warehouse laborer moves pallets on the ground.

-

The Underwriter’s View: The warehouse worker represents high frequency risk (back strains, minor cuts). The ironworker represents pure severity risk (catastrophic fall, structural collapse).

-

The Outcome: The ironworker faces incredibly high premium rates, mandatory proof of fall-protection compliance, and strict policy limits, while the warehouse worker qualifies for standard, broad-market coverage.

Scenario 2: Bridge Ironworker vs. Low-Rise Construction Worker

-

The Exposure: A bridge ironworker connects spans over a river with high wind exposure; a low-rise carpenter builds a two-story framing skeleton.

-

The Underwriter’s View: The carpenter has a straightforward rescue path and manageable fall risks. The bridge ironworker faces remote rescue delays, severe weather exposure, and fatal fall potential over water.

-

The Outcome: The carpenter’s risk is easily placed in standard commercial markets. The bridge ironworker requires a specialized surplus-lines policy with explicit maritime or high-angle rescue underwriting provisions.

Scenario 3: Reinforcing Ironworker vs. Ornamental Installer

-

The Exposure: A rodman ties heavy rebar mats inside a deep foundation trench; an ornamental installer fastens an aluminum handrail inside a finished lobby.

-

The Underwriter’s View: The ornamental installer works in a controlled environment with minimal fall or crush hazards. The rodman faces heavy material handling, crush hazards from collapsing trenches, and chronic orthopedic strain.

-

The Outcome: The ornamental installer receives highly favorable occupational classifications and low premiums. The reinforcing ironworker faces stricter underwriting, focusing on lifting limits and trench safety, though without the severe height exclusions applied to structural workers.

Frequently Asked Questions

Why do insurers care more about an ironworker’s height exposure than a carpenter’s?

It comes down to the math of severity risk versus frequency risk. If a carpenter slips at a residential site, it usually results in a minor, predictable injury claim (frequency). Because ironworkers operate at extreme elevations on structural steel, any fall or structural collapse threatens a fatal or permanently disabling injury (severity). Insurers price ironwork higher because a single high-elevation claim can cost millions of dollars in long-term medical and wage payouts.

What is “exposure stacking” in ironworker insurance underwriting?

Exposure stacking occurs when an occupation encounters multiple high-risk environments at the exact same time. While a roof worker faces fall risks and a factory worker faces heavy machinery, a structural ironworker experiences height hazards, crane interaction, unstable steel frames, and weather volatility simultaneously. Underwriters heavily penalize stacked exposure systems because the compounding hazards dramatically raise the statistical likelihood of a catastrophic accident.

Can a structural ironworker qualify for standard disability insurance?

Rarely. Standard disability carriers closely scrutinize ironworkers because their injuries are frequently career-ending. Underwriting models assume that while many ironwork injuries are survivable, spinal damage, traumatic brain injuries, or balance impairments permanently prevent a worker from safely returning to the steel. Due to the lack of light-duty roles on a structural frame, ironworkers are typically routed to highly restricted, specialty, high-risk disability policies.

How do undisclosed OSHA violations affect an ironwork contractor’s insurance?

Insurers view OSHA citations—specifically fall-protection, crane-rigging, and structural-safety violations—as leading indicators of an imminent high-severity claim. If an employer has a pattern of citations, underwriters interpret it as evidence of a broken safety culture. This frequently results in immediate financial penalties during renewal, including major premium increases, extreme deductibles, or outright cancellation of coverage.

Key Takeaways

-

Severity Rules the Steel: Ironworkers face highly restrictive underwriting because their exposure is defined by Severity Risk rather than Frequency Risk; one major fall or structural incident can trigger a multimillion-dollar claim.

-

Stacked Risks Multiply Costs: Unlike traditional trades, ironwork combines multiple underwriting systems simultaneously, including extreme heights, crane interactions, structural instability, and heavy material handling.

-

Disability is Often Permanent: Disability underwriters scrutinize ironworkers intensely because the physical demands of structural steel work mean that many survivable injuries permanently end an ironworker’s career.

-

Classification Directs Pricing: Occupational classifications directly dictate premium pricing and policy restrictions. Hidden or undisclosed bridge, offshore, or high-rise work frequently leads to denied claims and canceled coverage.

-

Specialty Markets are Required: Due to multi-worker catastrophic exposure and reinsurance limits, ironwork is often rejected by standard insurers and must be handled via specialized ironworker insurance underwriting markets.

-

Safety Culture Equals Savings: Maintaining clean OSHA records, formal rigging certifications, and clear contractual boundaries is the only reliable way for structural steel contractors to lower insurance costs and maximize eligibility.

- Ironworker underwriting illustrates how construction workers’ insurance carriers evaluate occupational risk through classification systems, severity modeling, operational exposures, and claim-cost projections.

Institutional & Underwriting Reference

Institutional References

Occupational Safety and Health Administration (OSHA) — Steel Erection Standards (29 CFR Part 1926 Subpart R)

Referenced for steel erection safety requirements, fall-protection standards, connection procedures, crane coordination requirements, and elevated structural-work exposures that directly influence underwriting severity assessments.

Occupational Safety and Health Administration (OSHA) — Top Cited Standards

Referenced for regulatory enforcement trends involving fall protection, rigging practices, and construction-site safety violations frequently reviewed during insurance underwriting and renewal evaluations.

Bureau of Labor Statistics (BLS) — Census of Fatal Occupational Injuries (CFOI)

Referenced for occupational fatality data, construction injury trends, and severity-exposure analysis supporting insurer evaluation of elevated-risk occupations.

Bureau of Labor Statistics (BLS) — Standard Occupational Classification (SOC) System

Referenced for occupational classification verification involving structural iron and steel workers, bridge workers, industrial steel erectors, and related elevated-construction occupations.

National Council on Compensation Insurance (NCCI)

Referenced for workers’ compensation classification methodologies, experience rating principles, occupational risk categorization, and premium determination frameworks used throughout construction underwriting.

U.S. Department of Labor — Longshore and Harbor Workers’ Compensation Act (LHWCA)

Referenced for maritime injury coverage requirements affecting bridge construction, waterfront projects, marine structural work, and over-water ironwork operations.

Reviewed for Underwriting Accuracy

This article has been reviewed against the underwriting principles commonly applied to:

- Structural ironworker occupational classification

- Elevated-work severity modeling

- Catastrophic fall-risk assessment

- Construction workers’ compensation rating systems

- Disability insurance occupational-risk evaluation

- Crane and rigging exposure analysis

- Multi-worker catastrophic loss scenarios

- Maritime and over-water construction exposures

- OCIP and CCIP project-insurance structures

- OSHA compliance and Experience Modification Rate (EMR) considerations

- Occupational misclassification and claim-denial pathways

- Specialty-market and surplus-lines underwriting practices

Research & Underwriting Methodology

This article was developed using a risk-system methodology that evaluates ironwork exposure through five primary underwriting lenses:

1. Occupational Classification Analysis

Assessment of how insurers classify structural, reinforcing, ornamental, bridge, offshore, and industrial ironworkers using occupational classification systems and workers’ compensation rating frameworks.

2. Severity Modeling

Analysis of how elevated work height, crane interaction, structural instability, rescue complexity, and weather exposure influence catastrophic claim severity and underwriting decisions.

3. Failure-Path Evaluation

Review of common claim-dispute scenarios involving occupational misclassification, undisclosed project environments, policy exclusions, underwriting misrepresentation, and coverage-boundary violations.

4. Insurance-System Interpretation

Comparison of how workers’ compensation, general liability, disability insurance, maritime coverage, and specialty-market policies interpret identical occupational exposures through different underwriting frameworks.

5. Market-Structure Assessment

Evaluation of insurer appetite, reinsurance limitations, surplus-lines placement, project-insurance structures, and contractor-liability allocation mechanisms affecting ironwork insurance availability and pricing.

Published: June 2026

Last Updated: June 2026