Editorial notice: Reviewed for underwriting accuracy by the RJI Institutional Review Team | Published: June, 2026 | Updated: June, 2026

—————————————————————————————————————————

Executive Summary

Tower climbing insurance is heavily influenced by catastrophic fall severity, rescue-response complexity, disability exposure, and operational risk classification. Insurers evaluate tower height, rescue accessibility, subcontract exposure, environmental instability, and long-duration claim potential when determining underwriting eligibility, pricing structures, liability restrictions, and specialty-market placement for telecommunications tower operations.

What the worker experiences

For a tower technician, the daily “office” is an open-air lattice of steel swaying in high winds, hundreds of feet above the ground. The physical reality of the job is a continuous battle against environmental and physiological friction. On long ascents, workers face relentless grip fatigue, rapid dehydration, and thermal stress, whether from blistering heat radiating off steel or freezing winds that numb fingers.

The most acute friction occurs when something goes wrong. If a climber slips and their fall-arrest system engages, the operational hazard shifts from fall prevention to rescue-response severity. Suspended in mid-air, the worker faces rapidly escalating suspension-trauma risk. Suspended workers may experience rapidly worsening circulatory restriction and physiological deterioration during delayed rescue scenarios.

Insurers ultimately convert these operational realities into formal occupational classifications that determine pricing eligibility, underwriting restrictions, and market placement.

How systems label the worker

Because insurance algorithms cannot measure an individual climber’s bravery or skill, they rely on standardized occupational classifications to evaluate and categorize operational exposure. Underwriters start by filtering companies through standard Occupational Hazard Classification in Insurance indices like the 2018 Standard Occupational Classification (SOC) system:

-

SOC 49-2021: Radio, Cellular, and Tower Equipment Installers and Repairers

-

SOC 49-9052: Telecommunications Line Installers and Repairers

To translate this further into underwriting eligibility, carriers evaluate operations against the “Rescue-Height-Frequency” triad. This matrix determines whether an employer’s payroll qualifies for standard, admitted coverage or is rejected and pushed to surplus markets:

| Risk Tier | Operational Exposure Profile | Primary Underwriting Category |

| Tier 1: Ultra-Severity | Broadcast television/radio towers (2,000 ft+ guying systems) | Non-Admitted Excess & Surplus Only |

| Tier 2: High-Exposure | 5G/LTE cellular macro sites, structural monopoles, wind turbines | Specialty Lines / Heavy Exclusions |

| Tier 3: Managed Risk | Rooftop stealth shrouds, small cell street nodes, utility distribution poles | Admitted Standard Markets |

How carriers price the labeled exposure

Once an employer is assigned to an occupational classification tier, underwriters calculate the financial premium, a process that directly illustrates Why Elevated Workers Pay More for Insurance. Standard commercial insurance is built to price Frequency Risk, using thousands of minor, predictable data points (like ankle sprains or tool-handling cuts) to mathematically forecast next year’s loss ratios.

This is where Tower climbing insurance entirely breaks this traditional pricing model. It is underwritten strictly as a severity-driven risk. The probability of a catastrophic event is very low, but the financial exposure generated by a single event can be extraordinarily large.

In practical terms, this means insurers care less about how often tower incidents happen and more about how financially severe a single tower-climbing claim can become.

Because a solitary total-loss claim can materially disrupt underwriting profitability for severe occupational classes, underwriters heavily discount standard safety metrics. A company can have a flawless five-year loss-free record and a low Experience Modification Rate (EMR), yet still face substantially elevated premium structures. This reflects the distinction explained in NCCI Occupational Classification and EMR Systems, where historical loss performance and classification data influence underwriting, but catastrophic severity exposure can override favorable experience metrics.

Many tower contractors must also maintain elevated liability limits, umbrella structures, and contractor-specific coverage requirements to satisfy contractual obligations imposed by wireless carriers, tower owners, and telecommunications infrastructure operators.

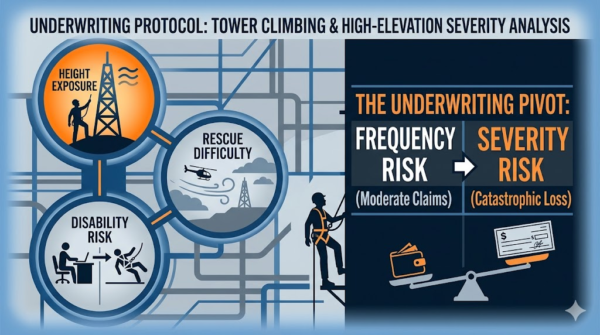

What operational variables move pricing

Actuarial models are highly dynamic and react directly to real-world field variables. In Height Exposure Underwriting: How Insurers Evaluate Elevated Workers, hazards are exponential rather than additive. Risk variables stack on top of each other, functioning as compounding multipliers:

Underwriters evaluate how multiple operational hazards compound one another simultaneously. Increased tower height, remote access limitations, structural movement, weather instability, and delayed rescue exposure collectively increase catastrophic-loss severity.

An underwriter looking at a crew retrofitting a cellular array on a downtown rooftop calculates a standard, manageable rescue window. If that exact same crew is dispatched to service a remote guyed tower in an unmapped rural corridor during a sudden high-wind or electrical event, the underwriting severity modeling changes rapidly. The operational reality of delayed high-angle EMS stabilization means an otherwise survivable fall-arrest incident escalates into a permanent, severe long-duration disability or fatality exposure.

Where systems break

Coverage disputes often emerge after severe tower-climbing incidents when actual field operations differ from the exposure disclosed during underwriting. Because the financial stakes of a tower claim are so severe, insurance companies deploy specialized forensic claims adjusters to conduct immediate material-misrepresentation investigations. Common system failure paths include:

-

Height-related liability exclusion disputes: A subcontractor’s technician is injured falling from a 150-foot cell platform; when the site owner passes the resulting severe third-party liability claim down to the contractor, the carrier denies the claim because the policy was explicitly endorsed with strict Height Restrictions in Occupational Insurance Policies.

-

Undisclosed subcontract climbing exposure: To meet aggressive carrier network deployment or storm-restoration deadlines, a contractor subcontracts climbing duties to uninsured or underinsured temporary subcontract climbing crews without verifying their standalone cell tower contractor insurance requirements.

-

Unreported Spectrum Hazards: Concealing specialized, ultra-hazardous secondary operations from the carrier, such as working near active high-voltage utility lines, structural welding at height, or handling high-power broadcast antennas without verified lockout/tagout protocols.

When these discrepancies are exposed during an investigation, the carrier has the legal leverage to deny the claim, limit policy benefits, or rescind the coverage entirely.

How different policies interpret the same exposure differently

When a climber falls or experiences an incident, separate insurance policies interpret the exact same event through vastly different legal lenses:

-

Workers’ Compensation: Views the event strictly as an acute trauma claim, bearing the financial weight of Catastrophic Fall Risk in Occupational Insurance. It covers the exceptionally high medical and trauma-related costs for specialized life-flight transport, high-angle extraction, acute trauma surgeries, and statutory wage replacement.

-

General Liability: Looks completely past the physical injuries to audit the commercial contractor chain. It parses complex indemnity agreements, cross-waivers, and hold-harmless provisions to determine if the tower owner, the carrier, or the contractor bears ultimate civil liability for structural damage or project interruption, looking closely for height-related liability exclusions.

-

Disability Insurance: Interprets the event through the lens of Fall Severity Modeling in Disability Insurance and the underwriting reality that tower climbing depends heavily on full physical capability. Tower climbing demands high levels of physical coordination, mobility, balance, grip strength, and vestibular (inner-ear balance) health. While a workers’ compensation policy aims to rehabilitate an injured worker until they can perform any basic labor, a long-term disability underwriter recognizes that even a minor permanent impairment, like slight residual dizziness from a concussion or a 15% reduction in hand grip, permanently ends a climber’s career. The worker suffers complete permanent occupational displacement, anchoring the carrier to a Permanent Disability Risk from Elevated Work that may create long-duration disability-payment exposure.

How the insurance market reacts structurally

Because tower climber claims regularly trigger catastrophically severe claims, standard commercial lines carriers generally have limited underwriting appetite for this sector. Reinsurance companies, the global entities that backstop primary insurers, impose strict reinsurance treaty limitations that restrict primary carriers from concentrating high-risk occupational exposures on their balance sheets.

Consequently, standard insurance market capacity contracts dramatically. Many admitted carriers reduce participation in severe tower-climbing classifications, pushing contractors toward non-admitted surplus lines markets, specialty high-hazard programs, and customized underwriting structures designed for catastrophic occupational exposures.

How business improve insurability

To push back against market contraction and secure access to stable, competitively priced insurance, tower construction companies must establish clear, verifiable risk-mitigation systems that directly lower the underwriter’s severity models:

-

Verifiable Training Architecture: Maintain a real-time, digitized audit trail documenting that the active field workforce maintains current certifications from institutions like the National Wireless Safety Alliance (NWSA) alongside current Competent Climber and rescue-training certifications, recognized by the National Association of Tower Erectors (NATE).

-

Regulatory Compliance Documentation: Provide clean historical audit tracks free of citations. Demonstrating strict adherence to OSHA Fall Protection Standards for High-Risk Work helps reduce the compliance failures that often contribute to OSHA Fall Violations and Insurance Costs, signaling stronger operational risk controls to insurance carriers.

-

Site-Specific Emergency Infrastructure: Submit detailed written Emergency Action Plans (EAPs) with every insurance submission to address elevated rescue-response severity concerns. Documenting functional high-angle rescue capabilities, on-site rescue equipment, and trained extraction procedures helps reduce modeled disability severity and improves access to more favorable underwriting markets.

Institutional & Underwriting References

Occupational Safety and Health Administration (OSHA) — Telecommunications Tower Safety

Used to evaluate elevated-work fatality exposure, fall-protection compliance failures, rescue-response limitations, and catastrophic injury patterns associated with tower-climbing operations.

Occupational Safety and Health Administration (OSHA) — Fall Protection Standards

Referenced for underwriting evaluation of fall-protection systems, rescue-planning requirements, employer safety compliance, and elevated-work operational controls.

National Institute for Occupational Safety and Health (NIOSH) — Falls in the Workplace

Used to assess fall-related injury severity, suspension-trauma exposure, rescue-delay consequences, and occupational fatality trends involving elevated work environments.

Bureau of Labor Statistics (BLS) — Standard Occupational Classification (SOC) System

Referenced for occupational classification verification involving telecommunications tower climbers, line installers, elevated infrastructure workers, and underwriting segmentation frameworks.

National Association of Tower Erectors (NATE)

Referenced for tower-industry operational standards, climbing safety frameworks, rescue competency expectations, and elevated-work risk-management guidance.

National Wireless Safety Alliance (NWSA)

Used to evaluate workforce certification systems, climbing competency verification, rescue-training standards, and operational qualification controls relevant to tower-climbing underwriting.

Reviewed for Underwriting Accuracy

This article was reviewed for underwriting accuracy involving:

- tower-climbing occupational classification systems

- catastrophic fall-severity exposure

- rescue-response severity modeling

- suspension-trauma underwriting concerns

- disability-duration exposure analysis

- height-restriction underwriting logic

- reinsurance-capacity limitations

- specialty-market underwriting structures

- workers’ compensation severity exposure

- operational-risk verification systems

- contractor-chain liability exposure

- underwriting eligibility improvement factors