Editorial notice: Reviewed for underwriting accuracy by the RJI Institutional Review Team | Published: June 2026 | Last reviewed: June 2026

————————————————————————————————————–

Executive Summary

OSHA fall protection standards set the minimum safety requirements for anyone working at height. For Workers, they define what protection your employer must legally provide. For business owners, they shape how insurers price your coverage, and whether they’ll insure you at all. Meeting the baseline keeps you compliant. How consistently you manage it determines your underwriting outcome.

What Are OSHA Fall Protection Standards?

Fall protection is the combination of equipment, engineered systems, and behavioral training designed to prevent workers from falling from elevated surfaces, or to reduce the physical trauma if a fall occurs. These rules are codified under federal law by the Occupational Safety and Health Administration (OSHA), and they apply uniformly across American industries.

Here’s why it matters beyond the legal requirement: a fall from height doesn’t produce an ordinary workplace injury. It produces catastrophic events, severe trauma, permanent disability, or death. That shift in injury profile moves the entire loss spectrum toward permanent total disabilities (PTD) and fatalities, which fundamentally alters how insurers price and underwrite elevated work.

Two concepts are essential to understanding what follows:

OSHA Compliance is a legal pass/fail threshold. A contractor either meets the statutory minimum or is in violation of federal regulations.

Insurance Underwriting evaluates something far broader: the aggregate financial exposure, the probability of systemic operational failure, and the ultimate severity of claims. Insurers don’t just ask “do you have a harness?” They assess whether your organization can implement safety systems consistently, across every project, every crew, and every subcontractor.

For a comprehensive breakdown of how carriers price structural elevation hazards across varying asset classes, see our technical reference guide on Height Exposure Underwriting.

When Does OSHA Require Fall Protection?

The height at which fall protection becomes legally mandatory depends on your industry classification:

| Industry | Required at | Federal Regulation |

|---|---|---|

| General Industry | 4 feet | 29 CFR Part 1910 Subpart D |

| Shipyards | 5 feet | 29 CFR Part 1915 Subpart I |

| Construction | 6 feet | 29 CFR Part 1926 Subpart M |

| Longshoring | 8 feet | 29 CFR Part 1918 Subpart I |

| Scaffolding | 10 feet | 29 CFR Part 1926.502 |

| Steel Erection (Connectors) | 15 feet | 29 CFR Part 1926.760 |

Once those trigger heights are crossed, employers must deploy one or more engineered or behavioral risk control systems:

- Guardrails — permanent or temporary structural barriers that prevent a worker from stepping off an unprotected edge

- Safety Nets — passive interception systems suspended beneath a work area to catch a falling worker and dissipate kinetic energy

- Personal Fall Arrest Systems (PFAS) — the harness, lanyard, and anchor assembly that stops a fall before ground impact

- Positioning Systems — harness rigs that hold a worker against a vertical surface (such as a utility pole) hands-free, preventing any free fall beyond two feet

- Travel Restraint Systems — active rigging that physically prevents a worker from reaching an unprotected edge in the first place

For a full breakdown of federal regulatory texts, consult the official OSHA Fall Protection Standards and the specific operational requirements detailed within the OSHA Construction Standards.

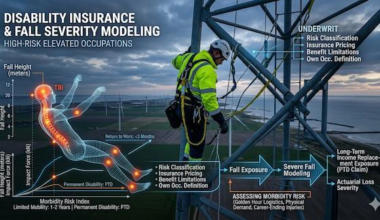

Why Height Exposure Creates Severe Insurance Risk

The higher the work, the larger the potential claim. Within commercial risk placement, working height radically alters mathematical loss modeling. The fundamental underwriting framework reflects a predictable pivot: as working height increases, insurer exposure shifts from frequency risk, many predictable, lower-cost claims, to severity risk, rare events that produce catastrophic, multi-million-dollar losses.

A ground-level contractor presents a risk model built on manageable, high-volume claims. A high-risk elevated contractor presents a binary model: long periods of zero losses interrupted by a single event that can exhaust primary policy limits entirely. Underwriters evaluate height exposure through five distinct severity multipliers:

Fatality Exposure: Falls remain the leading cause of death in construction. A fatal fall triggers immediate statutory death benefits, extensive legal defense costs, and serious operational disruption on the job.

Permanent Total Disability (PTD): Workers who survive extreme falls often face permanent brain or spinal injuries. The lifetime indemnity and medical escalation costs of a single PTD claim can easily reach $5,000,000 to $10,000,000: permanently altering the lives of everyone involved and anchoring loss runs for years.

Complex Rescue Costs: When a worker is suspended by a PFAS after a fall, the clock starts immediately. Specialized extraction, aerial lift equipment, and emergency services deployment all expand the ultimate claim expense, and suspension trauma can convert a successful mechanical arrest into a catastrophic medical loss if rescue takes too long.

Third-Party Liability: A falling worker or dropped tool doesn’t only endanger the crew. It poses an immediate hazard to pedestrians, nearby property, and public infrastructure, triggering massive General Liability (GL) claims alongside standard Workers’ Compensation, fracturing the liability chain across multiple policy lines.

Accumulation Risk: A single incident, a scaffold collapse or deck failure, can injure multiple workers simultaneously, triggering claims across several policies at once, instantly exhausting primary limits and exposing excess umbrellas. Catastrophic fall events may also affect reinsurance layers when multiple severe injuries arise from a single occurrence.

Carriers manage these catastrophic risk variables through stringent pricing mechanics, multi-layered reinsurance placements, and strict coverage limits detailed within our portal on Height Exposure Underwriting.

How Insurers Use OSHA Compliance During Underwriting

A common misconception among business owners is that maintaining basic compliance guarantees competitive insurance pricing. In reality, underwriters treat basic regulatory compliance as a baseline requirement, the floor, not a differentiator. Some standard-market carriers restrict elevated work exposures entirely, while surplus lines carriers may provide coverage with stricter controls, exclusions, or pricing adjustments.

During the account review process, commercial underwriters meticulously dissect an employer’s real-world safety data, focusing on:

Written Safety Programs: Is your fall protection plan a site-specific operational protocol, or a generic off-the-shelf document? Insurers can tell the difference.

Documented Rescue Procedures: Do you have a written plan to retrieve a suspended worker within minutes, or is your plan to call 911 and wait? The latter leaves your carrier exposed to severe medical escalation from suspension trauma.

Training and Certification Records: Are workers certified by verifiable third-party agencies, with credentials tracked alongside payroll? Or is training handled informally on the job?

Equipment Inspections: Are daily pre-use harness checks and annual competent-person inspections logged digitally, or managed by verbal confirmation alone?

OSHA Citation History: Underwriters frequently review publicly available OSHA citation histories, loss information, and safety records when evaluating an account. A clean record signals organizational control, while repeated or willful violations may indicate elevated operational risk.

Historical Incident Frequency: Loss runs stretching back 3 to 5 years are cross-referenced with payroll data to determine whether near-miss patterns reflect systemic behavioral failure.

While perfect compliance does not guarantee a lower rate, repeated violations or formal citations heavily influence an insured’s structural standing within Occupational Class Ratings, directly limiting carrier appetite, driving up base deductibles, and restricting overall eligibility.

What this means for contractors: Strong fall protection systems may improve carrier options, reduce pricing pressure, and support long-term insurability.

How Carriers Evaluate Fall Protection Programs

Insurance risk engineers translate physical workplace behaviors into underwriting scoring matrices. When reviewing an elevated contractor, carriers classify risk controls into distinct categories:

Positive Underwriting Indicators (Preferred Risk Quality)

Certified Competent Person Training: Every job site features a designated, highly trained supervisor capable of identifying fall hazards and authorized to halt work immediately.

Engineered & Certified Anchor Systems: Instead of relying on improvised tie-off spots, the firm utilizes permanently engineered, structurally validated anchorage points certified by a licensed structural engineer.

Documented, Site-Specific Rescue Plans: Every job site has an active rescue kit containing specialized extension poles, trauma straps, and pre-rigged mechanical advantage blocks so crews can act quickly.

Third-Party Independent Safety Audits: The contractor voluntarily pays an external safety firm to conduct unannounced, bi-weekly site inspections, providing digital reports directly to management.

Adverse Underwriting Indicators (Substandard Risk Quality)

Frequent or Open OSHA Citations: Unresolved or repeated citations for lack of fall protection indicate a systemic breakdown of supervisor oversight on active projects.

Informal or Oral Safety Practices: Safety policies rely heavily on “common sense” rather than written, signed, and enforced daily pre-shift safety checklists.

Absent Rescue Procedures: The operational plan for a suspended worker is simply to dial 911, exposing the carrier to severe medical complications from extended suspension.

Subcontractor Safety Deficiencies: The primary contractor fails to collect verifiable certificates of insurance (COIs) or fails to enforce their own fall safety mandates down to tiered trade partners.

When multiple adverse indicators appear simultaneously, carriers may increase premiums, restrict coverage, impose structural exclusions, or decline the account entirely. The longer and more difficult a rescue becomes, the larger the potential claim, an operational reality analyzed under Rescue Difficulty Underwriting and reflected within Occupational Class Ratings.

Failure Paths That Increase Claim Exposure

When an elevated safety system breaks down, the resulting failure path moves rapidly from a physical incident to a complex, multi-layered insurance crisis. These system-level breakdowns predictably amplify financial exposure:

Anchor Point Failure

A worker wears a premium harness and connects their deceleration lanyard correctly, but the structural anchor point fails under the sudden application of dynamic kinetic force.

Insurance Implication: This structural failure instantly converts a controlled suspension event into a catastrophic, full-impact fatality or permanent disability claim. It expands the litigation profile to include third-party product liability or structural design litigation, fracturing the liability chain between the equipment manufacturer, the project engineer, and the contractor.

Rescue Delays

A worker falls from an elevated platform, and their PFAS deploys perfectly, successfully halting their free fall. However, the contractor has no active, on-site rescue mechanism. The worker remains suspended for forty-five minutes.

Insurance Implication: Rescue delays increase medical complications, disability exposure, and claim severity. Through the lens of Rescue Difficulty Underwriting, a successful mechanical arrest is rendered a catastrophic medical claim solely due to operational timing failures and subsequent orthostatic intolerance.

Subcontractor Non-Compliance

A general contractor mandates 100% fall protection tie-off on a multi-story mixed-use project. A secondary framing subcontractor ignores the mandate, allowing an un-tied worker to traverse an unprotected edge. The worker falls through an open elevator shaft.

Insurance Implication: This triggers immediate, multi-line litigation. The injured worker sues the general contractor under an “Action Over” lawsuit, alleging failure to maintain a safe workplace. Because the subcontractor’s policy likely contains hidden independent contractor exclusions or narrow height limitations, a massive legal dispute erupts over contractual risk transfer, indemnification clauses, and primary versus excess policy responses.

Missing Documentation

A worker is injured on a temporary scaffolding platform. The carrier requests historical training records, daily inspection checklists, and signed pre-shift huddle documentation for that work week. The contractor cannot produce them.

Insurance Implication: In court, a lack of documentation is legally equated to a lack of execution. The absence of a verifiable digital paper trail strips defense attorneys of their ability to mitigate punitive damage claims, dramatically escalating final loss severity, maximizing plaintiff settlement leverage, and guaranteeing severe premium surcharges or non-renewals at the upcoming policy expiration. If it isn’t written down and dated, it may as well not have happened.

Can OSHA Violations Affect Insurance Claims?

A critical operational boundary exists between statutory administrative penalties and policy enforcement: an administrative OSHA violation does not automatically void a commercial insurance claim.

Workers’ Compensation operates strictly as a no-fault system in the United States. If an employee bypasses an engineered guardrail and falls from a roof, the statutory workers’ compensation policy is still legally required to respond, paying all necessary medical care and indemnity wage replacement benefits.

However, a serious, willful, or repeated OSHA violation deeply alters the macro-insurance architecture through several financial mechanisms:

- Experience Modification Rate (EMR) Inflation: Severe fall losses flow directly into the employer’s NCCI actuarial formula, driving the EMR above the critical 1.0 threshold for up to three consecutive years and dramatically raising manual premiums.

- Non-Renewal Decisions: Carriers are under no legal obligation to continue insuring a business. A severe fall combined with serious OSHA citations frequently triggers an immediate notice of non-renewal at policy expiration.

- Eligibility Exclusion: The contractor is displaced from the competitive admitted insurance market and forced into the non-admitted surplus lines arena or state-backed assigned risk pools, where premiums are often double or triple for half the coverage.

- Employer Liability Caps: In certain states, if an employer exhibits gross negligence or intentional malice by ignoring an explicit OSHA mandate, the exclusive remedy shield of workers’ compensation can be pierced, allowing the employee or their estate to sue directly for uncapped civil damages.

Structural Exclusions in High-Risk Fall Exposure Coverage

To protect their capital reserves from unpriceable hazards, carriers frequently introduce restrictive policy endorsements into commercial liability and workers’ compensation policies. Exclusions do not eliminate risk; they allocate risk away from the insurer when exposures cannot be priced accurately. In elevated work environments, underwriters rely heavily on the following five structural exclusions:

Work Above Specified Heights: Many standard-lines policies contain an explicit absolute height limitation, excluding all operations performed above three stories or 30 feet. Any loss occurring above this operational ceiling may fall outside policy coverage or trigger coverage disputes.

Unreported Subcontractors: Policies may explicitly exclude any third-party liability claims arising from the actions of tiered subcontractors unless those subcontractors have been formally disclosed, vetted, and approved by the carrier prior to project kickoff.

Intentional Safety Violations: If an insured receives a formal “willful” citation from regulatory authorities, specific defense and indemnity components within the Employer’s Liability section may be excluded due to intentional disregard of mandatory safety systems.

Excluded Rope Access Operations: Because industrial climbing demands a distinct risk profile, generic construction policies frequently incorporate explicit exclusions for any work utilizing specialized rope access, bosun’s chairs, or structural rappelling frameworks.

Unscheduled Locations: In high-risk sectors, coverage may be strictly restricted to specific job sites designated in the policy declarations. Working at an unscheduled location shifts the entire financial liability back onto the operating contractor.

Occupations Most Affected by Fall Protection Underwriting

Different industrial classifications present unique height exposure vectors and specialized rescue challenges, demanding precise underwriting evaluation:

Tower Climber Insurance

Workers climbing telecommunications structures routinely operate at heights between 100 and 1,000+ feet. At these heights, an uncontrolled fall may result in catastrophic injury or fatality if primary protection systems fail. Underwriters writing Tower Climber Insurance evaluate the strict use of dual-carabiner 100% tie-off compliance, weather tracking protocols, and specialized remote vertical rescue systems that crews must deploy in the field.

Roofer Insurance

Commercial and residential roofers experience the highest gross volume of fall injuries of any trade group, driven by sloped surfaces, fragile decking, and high worker turnover. Roofer Insurance is classified as a highly restricted risk category. Carriers heavily scrutinize structural height limitations within the policy form, the presence of perimeter guardrail systems, and meticulous daily payroll split tracking to avoid audit penalties.

Ironworker Insurance

Structural steel erectors assemble the primary skeletal frames of skyscrapers, bridges, and industrial structures, often operating on narrow beams before floors are constructed. Underwriters for Ironworker Insurance closely review the utilization of horizontal lifelines, nets, and advanced crane-suspended personnel platforms, matching exposures against stringent catastrophe-modeling tools.

Wind Turbine Technician Insurance

Technicians operate inside and on top of nacelles located 200 to 400 feet above the ground, managing heavy mechanical components in confined, high-wind environments. Wind Turbine Technician Insurance requires specialized evaluation of internal climb-assist ladders, specialized exit-harness rigging, and hyper-detailed emergency evacuation plans designed for remote geographic locations.

Rope Access Technician Insurance

Utilizing advanced industrial climbing techniques, these specialists descend or ascend the exterior facades of skyscrapers, dams, and industrial structures via high-tensile static lines. Rope Access Technician Insurance assesses adherence to strict international frameworks (e.g., SPRAT/IRATA), looking for dual-line redundancy and extensive logged field hours.

Scaffold Worker Insurance

Erecting and dismantling temporary modular platforms creates dynamic, shifting elevation hazards before protective guardrails can be safely secured. Scaffold Worker Insurance focuses heavily on the competent person designation, structural capacity modeling to prevent tipping failures, and the clear separation of third-party general liability exposures from pedestrian foot traffic below.

Key Takeaways

- OSHA compliance is the legal minimum, not a pricing advantage. Meeting the standard keeps you out of trouble. Exceeding it is what keeps your coverage accessible and your premiums manageable.

- Insurers evaluate systems, not just equipment. The question isn’t whether you own a harness; it’s whether your entire operation uses one, every time, with documentation to prove it.

- Rescue capability matters as much as fall prevention. A contractor with a flawless harness program but no active rescue plan remains a severe, high-risk insurance exposure.

- Subcontractors are your exposure. If they don’t meet your safety standards, you may bear the legal and financial consequences.

- Documentation is your legal defense. If it isn’t written, signed, and dated, it may as well not have happened.

Final Underwriting Insight

Fall protection standards do not eliminate risk. They provide insurers with evidence that elevated exposures are being managed systematically. In high-risk occupations, underwriting often evaluates not whether falls are possible, but whether severe outcomes can be controlled when falls occur.

—————————————————————————————————————————

Institutional & Underwriting References

To verify data accuracy, legal thresholds, and structural risk models, this text links directly to the governing institutional bodies:

Occupational Safety and Health Administration (OSHA): The federal regulatory authority defining the statutory parameters of workplace safety engineering. Explore the comprehensive regulatory frameworks at OSHA Fall Protection Regulations.

National Institute for Occupational Safety and Health (NIOSH): The premier federal research body isolating empirical epidemiological trends in workplace trauma. Review their latest safety research at NIOSH Fall Injury Research.

National Council on Compensation Insurance (NCCI): The nation’s primary actuarial and statistical clearinghouse that translates loss data into modern experience modifications.

To evaluate macro-level industry fatality data and structural incident patterns, consult the official OSHA Fatal Falls Data.

Reviewed for Underwriting Accuracy

This document has been thoroughly evaluated against core insurance operations criteria:

- Height Exposure Severity Modeling: Validating the mathematical pivot from frequency to severity risk curves across elevated exposures

- Occupational Classification Analysis: Ensuring accurate alignment with NCCI, NAICS, and specialty surplus lines trade codes

- Rescue Complexity Evaluation: Reviewing medical, physiological, and technical extraction limits associated with suspension trauma

- Fall Protection Risk Controls: Assessing the direct underwriting impact of engineered versus passive and behavioral safety systems

- Claim Severity Pathways: Mapping the precise structural trajectory from a physical incident through the multi-line legal settlement process

- Liability Allocation Analysis: Isolating the contractual risk transfer, indemnity, and exclusion dynamics of multi-layered contracting.