Editorial Notice: Reviewed for underwriting accuracy using roofing occupational classification analysis, elevated-work severity modeling, commercial lines risk engineering, and multi-state workers’ compensation frameworks. | Published: June 2026 | Last reviewed: June 2026.

————————————————————————————————————–

Executive Summary

Navigating the complexities of roofing contractor insurance underwriting requires a deep understanding of how commercial insurance carriers calculate volatile construction hazards. Underwriters look past superficial company titles to evaluate working heights, material heating methods, subcontractor exposure, payroll classifications, and historical regulatory compliance.

When these operational metrics are translated into risk-selection frameworks, they dictate premium loads, policy exclusions, and claim reliability. This guide details the structural systems insurance companies use to judge roofing operations, providing contractors and risk managers with a blueprint to optimize account presentation and protect their coverage.

Why Roofing Contractors Face Higher Insurance Risk

Daily Physical/Environmental Realities

Roofing operators encounter intense physical and environmental friction. Daily exposure is defined by continuous steep-slope navigation, variable structural integrity of roof decks, and unmitigated climate conditions. These factors reduce physical grip, accelerate fatigue, and multiply mechanical error rates, turning routine movements into high-consequence safety risks within the broader Construction Workers Insurance ecosystem.

Injury and Illness Profile

Because of these environmental realities, the industry profile concentrates heavily on traumatic, permanent injuries rather than short-term illnesses. While lacerations, punctures from fastening tools, and acute musculoskeletal strains from handling heavy materials represent high-frequency claims, the trade is dominated by extreme severity risks. Falls from roof edges, scaffolding collapses, and catastrophic drops through unprotected skylights result in permanent orthopedic destruction, severe traumatic brain injuries (TBIs), or fatalities.

Why Roofing Injuries Create Long-Term Insurance Costs

When a roofing worker is injured, the claim experience is marked by severe friction. In disability insurance underwriting, insurers evaluate whether a claimant can realistically return to their exact trade. Because roofing requires perfect physical balance, mobility, and strength, even minor physical impairments can permanently prevent an employee from safely returning to steep-slope work.

This creates an extended financial tail on claims. Insurers realize that roofing firms have near-zero light-duty roles available on a job site, meaning injured workers often stay on total temporary disability or permanent partial disability benefits for maximum durations, driving up the ultimate cost of the file.

How Insurers Classify Roofing Contractors

Primary Regulatory Codes (NCCI, ISO, NAICS)

Underwriters standardize this real-world risk using specific regulatory codes. For workers’ compensation, payroll must be allocated according to NCCI Class Code 5551 (Roofing – All Kinds), which carries some of the highest base rates in construction. For general liability, underwriters use ISO Code 98686 to classify commercial and residential roofing operations. On a broader macroeconomic scale, these businesses are tracked under NAICS Code 238160 (Roofing Contractors).

[NAICS Code: 238160] ──► [ISO Code: 98686] ──► [NCCI Code: 5551] ──► [2018 SOC Detailed Code: 47-2181]

(Roofing Contractors) (General Liability) (Workers' Comp) (Federal Task Taxonomy)

Transitional Drift & Mismatch Risk

A major administrative breakpoint occurs through “transitional drift”—where an employee’s duties shift in the field, but their paperwork remains unchanged. In accordance with standard classification rules, risk evaluation is entirely exposure-based, meaning workers are classified by what they physically do, not by their official titles.

If a worker is hired as a low-risk “Siding Installer” or “Residential Carpenter” but is reassigned to patch a roof leak, they immediately drift into a higher-hazard classification system. These underlying alphanumeric sorting rules are detailed in our comprehensive guide on Occupational Class Ratings.

Audit and Payroll Exposure

At the annual premium audit, insurers verify operational reality by inspecting payroll ledgers, W-2 forms, 1099 certificates, and material invoices. Auditors enforce a rigid 50% Time-on-Tools Rule for supervisory roles. If an audit or site log reveals that an employee designated as a “Supervisory Foreman” spends more than 50% of their billable hours performing manual roof removal or material handling, the carrier rejects the supervisory classification and defaults their entire payroll exposure to the manual roofing tier — not a partial adjustment, but a full reclassification.

For business owners, this means a foreman whose wages were coded at a lower supervisory rate can trigger a retroactive premium bill covering their entire annual payroll at the highest roofing classification rate. That surprise audit invoice is one of the most common and most avoidable financial shocks in the trade.

How Roofing Insurance Underwriting Works

Base Rates

The underwriting process begins with the base rate, which is a fixed dollar amount charged per $100 of payroll or gross revenue. This base rate is determined by historical loss-cost data within a specific state or territory. Because roofing is actuarially categorized as a severe risk, its baseline pricing is heavily loaded before any individual company credits or safety factors are considered.

Rating Modifiers (EMR/Mod)

The primary mechanism used to adjust the base rate is the Experience Modification Rate (EMR), or “Mod.” The EMR acts as a direct mathematical reflection of a contractor’s safety record compared to the industry average (which is set at 1.0).

-

An EMR of 0.85 means the contractor has a better-than-average safety record, earning a 15% discount on workers’ compensation premiums.

-

An EMR of 1.35 signals a decaying safety framework, applying a 35% penalty surge directly to the baseline pricing.

Eligibility Filters

To protect their portfolios, insurance companies establish hard eligibility filters that screen out high-risk processes. Standard, well-known insurance markets operate under strict guidelines that prohibit them from writing policies for roofing contractors who perform work above a specific story threshold or who use specific high-hazard materials. While 3 stories or 36 feet is a commonly cited threshold, these limits vary materially by carrier, state, and material system. Some admitted markets draw the line at 2 stories, others apply height restrictions only to flat or torch-down work.

Contractors operating near any height boundary should not assume they fall within standard market appetite. The mechanics of how carriers evaluate vertical exposure and set these thresholds are broken down in Height Restriction Underwriting. Verify the specific threshold in your program guidelines before accepting a contract, not after signing one.

Breaching these filters triggers an immediate underwriting decision breakpoint, forcing the file out of standard lines.

Underwriter Red Flags

When reviewing an application, analysts look for specific red flags that indicate unpriced hazard exposure:

-

Undeclared Hot-Process / Open-Flame Operations: Applications claiming 100% cold-applied or shingle work, but financial records showing bulk purchases of torch-down membranes or hot asphalt kettles.

-

Gaps in Continuous Coverage: Historical periods where the business operated without active insurance policies, signaling financial instability or hidden losses.

-

Rapid Multi-State Expansion: Moving into new state jurisdictions without establishing localized safety management or verified supervisor controls.

What Factors Increase Roofing Insurance Costs?

Size and Scale

The premium and risk structure varies significantly based on the scale of the operation. Small, residential “Chuck-in-a-truck” firms face intense scrutiny regarding owner-operator exposure; if the owner is injured on the wood deck, the business loses its primary revenue driver and management layer simultaneously, spiking the risk of an extended disability claim. Conversely, large commercial roofing enterprises are evaluated on corporate risk management frameworks, subcontractor safety verification, and formal safety director roles.

Severity Amplifiers

Underwriters look at real-world operational variables that amplify the severity of a potential claim. The vertical scale of a project is the single most critical variable carriers evaluate, a process detailed in Height Exposure Underwriting. Other severity amplifiers include:

-

Extreme Pitch and Slope: Steep-slope roofs dramatically accelerate fall velocity and complicate standard personal fall arrest setups.

-

Multi-Employer Site Friction: Operating on a single site alongside crane operators, structural steel workers, and masonry crews increases the likelihood of cross-liability accidents.

-

High-Angle Evacuation Hurdles: Working on high-rise commercial skeletons where standard emergency services cannot easily extract an injured worker, requiring specialized high-angle rescue teams.

Safety Controls

Carriers heavily favor contractors who back up their applications with documented, verifiable safety controls. This includes keeping flawless records of formal OSHA 10-hour or 30-hour cards, logging daily equipment and harness inspections, and utilizing engineered anchorage points rather than temporary job-built structural ties.

Historical OSHA citation patterns can materially influence underwriting decisions, premium calculations, and carrier appetite. OSHA Fall Violations and Insurance Costs explains how repeated safety violations affect pricing, renewals, and long-term insurability.

Seasonal Variability

The roofing sector is subject to intense seasonal volatility. During peak summer construction surges, payrolls expand rapidly with temporary or uncertified laborers, increasing frequency risk. Actuarially, this surge compresses the underwriter’s margin, prompting deep reviews of a contractor’s formal onboarding and safety training protocols for short-term workers.

Accumulation Risk

Insurers must manage “accumulation risk”, the concentration of multiple insured risks in a single geographic zone. If a carrier insures twenty roofing contractors in a single coastal city, a major severe weather event or hurricane could trigger simultaneous claims across all twenty policies, creating concentrated loss exposure within the insurer’s regional portfolio. Underwriters use strict territorial caps to limit their exposure to this aggregated risk.

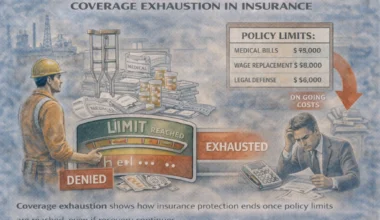

Common Reasons Roofing Insurance Claims Are Denied

Claim Failures

The primary failure path occurs during the claims process following an undisclosed operation. If a residential contractor takes a high-margin commercial contract requiring an open-flame torch-down system without notifying their broker, any resulting fire or injury triggers an immediate, intense forensic investigation.

Coverage Gaps

A massive gap occurs when contractors do not match their actual field work with their policy definitions. The underwriting logic surrounding these vertical boundaries is broken down in Catastrophic Fall Risk in Occupational Insurance. If a policy contains an absolute exclusion for commercial projects or a restriction on working heights above 36 feet, performing work at 40 feet instantly invalidates the coverage mechanism for that project.

Coverage Reliability Failures

If an underwriter discovers that a roofing firm deliberately hid its true operational hazards, such as misclassifying roofers as low-hazard siding installers on application questionnaires, the carrier has the legal authority to execute a retroactive policy rescission within the contestability window.

The practical consequence is more severe than most contractors realize. Rescission does not simply void coverage for the incident project. It voids the entire policy as though it never existed, leaving every project completed during that policy period uninsured simultaneously.

A single forensic audit can therefore expose the business to uninsured liability on dozens of completed jobs at once. In high-severity cases, the resulting out-of-pocket defense costs and damage awards across multiple open claims frequently force corporate liquidation.

Many of these breakdowns follow recurring patterns seen across hazardous occupations, which are examined in Common Reasons Claims Are Denied for Risk Jobs.

Claim Breakpoints

The ultimate breakpoint occurs when a claim is officially denied due to material misrepresentation. In high-severity cases, a denied third-party bodily injury or structural property claim forces the roofing contractor to pay defense costs and damages out of pocket, frequently leading to corporate liquidation or bankruptcy.

[Undisclosed Hazard Exposure] ──► [Catastrophic Site Incident] ──► [Forensic Audit] ──► [Policy Rescission Decision] ──► [Claim Denial / Uninsured Liability]

What Insurance Policies Do Roofing Contractors Need?

Workers’ Compensation Interpretation

From a workers’ compensation standpoint, the insurer’s exposure is entirely focused on the human element, statutory medical coverage, lost wage replacement, and long-tail permanent disability. Because workers’ compensation is a “no-fault” statutory line, the carrier must pay for employee injuries sustained on the job, even if the worker violated a company safety policy. To mitigate this absolute exposure, underwriters enforce aggressive pricing loads via NCCI Code 5551.

General Liability & Completed Operations

General liability underwriters evaluate risk through a completely different lens: property damage and third-party bodily injury. These boundaries are structured as strict contractual caps, analyzed under height restrictions. For roofers, this exposure is split into two critical hazards:

Operations Risk:

An open asphalt kettle tipping over and causing an active fire, or rainwater penetrating an exposed roof deck during a tear-off, causing massive interior structural damage to a client’s building. This specific exposure is managed through General Liability Roofing Insurance policies.

Completed Operations Risk

Completed operations is the single highest long-tail general liability exposure for commercial roofing contractors, and it is consistently the most misunderstood coverage in the trade. Unlike operations risk, which covers active job-site incidents, completed operations liability attaches after the work is finished and the contractor has left the site. A roof that fails two or three years post-installation due to a hidden membrane defect, improper flashing, or inadequate drainage design can collapse, flood a building interior, or injure a third party. Such claims are often evaluated under the completed operations portion of the commercial general liability policy, subject to policy terms, exclusions, and endorsements.

Occurrence vs. Claims-Made Forms

The policy form type is the threshold decision in completed operations coverage. An occurrence policy generally responds to bodily injury or property damage that takes place during the policy period, regardless of when the claim is filed. If a roof installed in 2023 fails in 2026 and causes a collapse, an occurrence policy active during the period of damage may respond, even if that policy has since been cancelled or the carrier has exited the market. This is the preferred form for roofing operations because of the multi-year lag between installation and structural failure.

A claims-made policy only responds if both the triggering incident and the formal claim filing occur while the policy is active. A contractor who switches carriers, lets a policy lapse, or retires without purchasing tail coverage can find every project completed under the old policy suddenly uninsured. Claims-made forms are cheaper upfront; carriers sometimes push them for that reason, but for commercial roofing, the long latency between project completion and detectable failure makes this form a structural coverage risk that contractors need to evaluate carefully before binding.

Extended Reporting Periods (Tail Coverage)

Contractors on claims-made forms who change carriers, downsize, or exit the business must purchase an Extended Reporting Period (ERP), commonly called a “tail.” The tail extends the window during which a claim can be filed and still trigger the old policy’s coverage. Without it, every completed project from the claims-made policy period becomes uninsured the moment the policy lapses.

ERP pricing typically runs 100–200% of the expiring annual premium for a five-year tail, paid as a one-time lump sum. This cost surprises most contractors who assumed that cancelling a policy ended all exposure. It does not. Cancellation closes the coverage window but leaves the underlying liability intact. In most states, construction defect statutes of repose run six to ten years from project completion, meaning the liability window outlasts the policy by years unless tail coverage is in place.

The “Your Work” Exclusion

Standard commercial general liability policies contain a “your work” exclusion (ISO CG 00 01, Exclusion L) that eliminates coverage for property damage to the completed work itself. This is one of the most consequential and least-explained exclusions in roofing GL policies.

In practice, if a roof membrane fails due to faulty installation, the GL policy will typically cover resulting damage, water intrusion destroying interior finishes, electrical systems, stored inventory, but will exclude the cost of repairing or replacing the defective roof itself. The line between the defective work product and the consequential damage it causes determines what gets paid. For a contractor facing a $400,000 claim, that distinction might mean $320,000 is covered, and $80,000 is not, or it might mean the entire claim is disputed until the allocation is litigated.

Contractors should also verify how the subcontractor exception within this exclusion is structured on their specific policy. ISO’s standard form can restore coverage for damage caused by a subcontractor’s work, but only when the endorsement language is correctly structured and the subcontractor’s operations are properly scheduled. Carriers routinely issue policies where this exception is narrowed or deleted, leaving the general contractor exposed for damage originating from subcontracted work. Confirm this language with your broker or coverage counsel before any commercial project involving subcontracted roofing labor.

Specialty Lines (Inland Marine, Commercial Auto)

Roofing operations require independent evaluation across secondary specialty lines:

-

Inland Marine (Equipment/Cargo): Covers expensive tools, asphalt kettles, generators, and safety rigging while in transit or stored on-site. Underwriters look at security storage protocols and theft history.

-

Commercial Auto: Evaluates the risk of heavy supply trucks, dump trucks, and trailers transporting heavy materials. Carriers closely screen the Motor Vehicle Records (MVRs) of all drivers, since a single commercial auto collision involving a multi-ton roofing truck represents a severe liability exposure.

Why Roofing Insurance Is Becoming Harder to Get

Capacity & Availability Constraints

Because roofing carries such a high severity risk, insurance “capacity”, the amount of premium volume standard carriers are willing to write for this trade, is extremely constrained. During a hard insurance market cycle, standard, well-known admitted carriers aggressively pull back their appetite, completely shutting down their roofing programs and refusing to write new accounts.

Regulatory & Litigation Surges / Market Cycle Sensitivity

The roofing sector is highly sensitive to litigation surges and changes in local safety laws. In regions with strict structural liability rules or aggressive tort environments, third-party lawsuits against contractors spike sharply following site accidents, completely upending the standard Commercial Roofing Insurance Claims Process. When litigation costs rise, insurance carriers respond by increasing baseline premiums across the entire roofing pool, tightening exclusions, and reducing the availability of standard general liability coverage.

Carrier Appetite Trends

Current market trends show standard insurance providers limiting their footprint strictly to low-rise, non-hazardous residential work. Any contractor utilizing hot processes, torch-down systems, or operating on commercial skeletons is routed directly away from standard lines and into the specialized non-admitted surplus lines market, where policies are custom-built with high mandatory deductibles and tailored coverage limitations.

Contractors placed in surplus lines must understand a structural difference that is rarely explained clearly: non-admitted carriers are not backed by state guaranty funds. When an admitted carrier becomes insolvent, the state guaranty fund steps in to pay outstanding claims up to statutory limits. That backstop does not exist for surplus lines carriers. Because surplus lines policies generally are not protected by state guaranty funds, contractor recovery options may be limited if a non-admitted carrier becomes insolvent. Contractors should evaluate the carrier’s financial strength and discuss these risks with their broker before binding coverage.

How Roofing Contractors Can Improve Insurance Eligibility

Immediate Mitigation Wins

Contractors can secure immediate eligibility improvements and better pricing terms by implementing quick, transparent operational changes:

-

Isolate Task Documentation: Maintain clean daily logs separating ornamental or gutter work from active roofing, preventing the automatic downward reclassification of lower-risk workers.

-

Enforce Subcontractor Controls: Mandate that any hired subcontractor provide a valid Certificate of Insurance (COI) matching or exceeding your own general liability limits, with an explicit “Hold Harmless” indemnity agreement attached.

Structural Data Compliance

Achieve long-term compliance by aligning all internal payroll and operational records with standard institutional databases. Ensure your internal job cost data matches NCCI Code 5551 definitions, and audit your job titles against the federal 2018 SOC taxonomy before submitting your files to an underwriter. Providing an organized, database-compliant file signals a structured risk culture to the carrier’s automated screening software.

System-Compliant Account Presentation

When presenting an account to an underwriter, package your application as a professional, defensive submission. Do not simply fill out a generic questionnaire. Include a typed, formal safety manual modeled after the OSHA Roofing Safety Framework, provide a five-year verified EMR history report, include a written high-angle rescue protocol, and detail your sub-contractor pre-screening process.

A comprehensive, system-compliant presentation proves to the underwriter that you understand your hazards, separating your business from low-tier operations and unlocking access to competitive pricing and preferred carrier tiers.

—————————————————————————————————————————

Institutional & Underwriting References

Occupational Safety and Health Administration (OSHA)

Roofing Fall Protection Standards (29 CFR 1926 Subpart M) — Referenced for fall-protection requirements, warning line systems, personal fall arrest standards, ladder safety, and regulatory compliance factors that influence roofing underwriting and claim investigations.

National Council on Compensation Insurance (NCCI)

Workers’ Compensation Classification Inspection & Class Code System — Referenced for NCCI Code 5551 payroll allocation, workers’ compensation rating structures, Experience Modification Rate (EMR) calculations, audit procedures, and multi-state roofing classifications.

U.S. Bureau of Labor Statistics (BLS)

Census of Fatal Occupational Injuries (CFOI) and Injury & Illness Statistics — Used to evaluate roofing fatality trends, injury frequency, claim severity patterns, and broader occupational risk characteristics across construction trades.

U.S. Bureau of Labor Statistics — Standard Occupational Classification (SOC) System

2018 Standard Occupational Classification (SOC) System — Referenced for occupational classification validation, task-based risk identification, roofing trade categorization under SOC 47-2181, and underwriting exposure verification.

National Institute for Occupational Safety and Health (NIOSH)

Construction Falls Prevention Research and FACE Program — Referenced for catastrophic fall exposure analysis, injury mechanisms, rescue challenges, and long-term disability implications associated with elevated work environments.

Insurance Services Office (ISO)

Commercial General Liability Classification System — Referenced for general liability classification structures, roofing operations coding, completed operations exposure, and third-party property damage risk evaluation.

U.S. Census Bureau

North American Industry Classification System (NAICS) — Referenced for industry-level business classification under NAICS 238160 (Roofing Contractors), supporting market segmentation and underwriting categorization.

Reviewed for Underwriting Accuracy

This article was reviewed for underwriting accuracy using:

- Roofing occupational classification analysis (SOC 47-2181, NCCI Code 5551, ISO classifications, and NAICS 238160)

- Elevated-work severity modeling and catastrophic fall exposure assessment

- Commercial lines risk engineering principles for roofing operations

- Workers’ compensation rating structures and Experience Modification Rate (EMR) frameworks

- General liability underwriting for completed operations and third-party property damage exposures

- Subcontractor risk transfer analysis, Certificates of Insurance (COIs), and hold harmless agreements

- Payroll classification audits and occupational misclassification scenarios

- Carrier eligibility filters, surplus lines placement, and market appetite restrictions

- Roofing contractor risk selection and carrier appetite analysis across admitted and surplus lines markets

Research & Underwriting Methodology

This article applies an occupational underwriting framework that translates real-world roofing operations into insurance-system classifications, pricing models, and coverage outcomes. The analysis integrates regulatory standards, occupational classification systems, and commercial underwriting practices commonly used across construction-related insurance markets.

Research and underwriting analysis for this article incorporates:

- Occupational classification frameworks, including the 2018 Standard Occupational Classification (SOC) system, NCCI workers’ compensation classifications, ISO liability classifications, and NAICS industry codes

- Regulatory guidance from OSHA roofing safety standards and fall-protection requirements

- Occupational injury and fatality datasets from the Bureau of Labor Statistics (BLS) and NIOSH research programs

- Workers’ compensation rating principles, including payroll allocation, experience modification, and audit procedures

- Commercial general liability underwriting, completed operations exposures, and third-party property damage analysis

- Roofing contractor eligibility filters, including height restrictions, open-flame operations, and subcontractor risk transfer mechanisms

- Market-capacity dynamics affecting admitted carriers and surplus lines placement for elevated-risk construction operations

The objective of this methodology is to translate institutional underwriting systems into practical operational consequences that roofing contractors can use to improve eligibility, strengthen risk presentation, and maintain coverage reliability.