Editorial notice: Reviewed for underwriting accuracy by the RJI Institutional Review Team | Published: May, 2026 | Updated: June, 2026.

—————————————————————————————————————————

Executive Summary

Disability insurers carefully evaluate severe fall injuries because workers in high-angle or elevated environments face a greater risk of permanent disability after falls from roofs, towers, scaffolding, bridges, and industrial structures. Severe falls can result in long-term income-replacement claims, extended medical treatment, and permanent work limitations that directly affect underwriting decisions, occupational classification, and disability insurance pricing.

What Is Fall Severity Modeling in Disability Insurance?

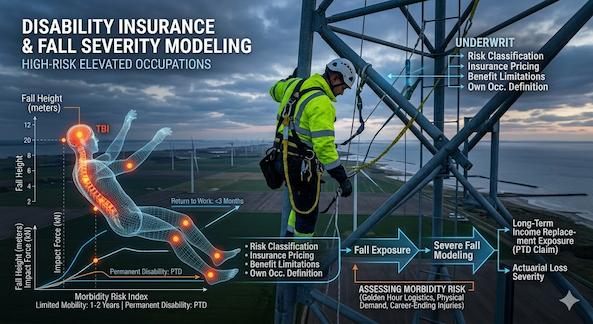

Fall severity modeling is the process disability insurers use to estimate how serious a fall-related injury could become and how that injury may affect a worker’s long-term ability to earn income (long-term disability risk).

Instead of only asking whether falls happen frequently, disability insurers also evaluate:

- how severe the injury could become and whether complications may create permanent work limitations

- how long recovery could take

- whether permanent impairment is possible

- whether the worker can return to the same occupation

- whether the worker could perform any physically demanding work afterward

- how much long-term income replacement exposure the insurer may face

For elevated occupations, insurers focus heavily on whether a severe fall could permanently prevent a worker from returning to physically demanding labor.

Fall Severity Modeling in Disability Insurance helps insurers estimate how severe fall-related injuries may affect long-term work ability, income replacement exposure, and disability claim risk for elevated workers.

A worker may physically survive a fall but still lose the climbing ability, mobility, balance, strength, coordination, or endurance required for their occupation. That long-term work-loss exposure is central to disability underwriting decisions.

This underwriting approach closely connects:

fall exposure → disability risk → long-term insurance cost

This disability severity analysis closely overlaps with the broader elevated-risk framework explained in Height Exposure Underwriting: How Insurers Evaluate Elevated Workers, where insurers evaluate working height, climbing frequency, rescue complexity, and occupational severity exposure.

Why Severe Falls Create Major Disability Insurance Risk

Why do disability insurers worry more about severe falls than minor injuries?

Disability insurers focus heavily on severe falls because elevated occupational accidents often create injuries that permanently affect a worker’s ability to perform physical labor.

Common severe fall-related disability concerns include:

• traumatic brain injuries

• spinal cord injuries

• paralysis

• mobility loss

• chronic balance problems

• chronic pain conditions

• neurological damage

• long-term musculoskeletal injuries

These injuries may permanently affect a worker’s ability to climb, lift, balance, carry equipment, or safely perform physically demanding labor.

A worker may survive a fall from a tower, scaffold, bridge, or industrial platform but still lose the physical ability needed for climbing, lifting, balancing, carrying equipment, or working at height safely.

That creates a major disability concern because disability insurance primarily protects income-producing work ability.

Insurers closely monitor long-term disability exposure associated with severe falls identified in NIOSH fall injury research.

For example:

- A roofer who loses balance coordination may no longer safely work on pitched roofs.

- A utility lineman with spinal damage may lose climbing ability permanently.

- A scaffold worker with chronic pain may become unable to perform heavy labor consistently.

Even when workers eventually recover partially, insurers evaluate whether they can realistically return to the same occupational demands.

The more physically demanding the occupation, the greater the long-term disability severity exposure becomes.

This is also why elevated occupations often appear in stricter occupational risk classifications discussed in Catastrophic Fall Risk in Occupational Insurance.

Why disability insurers model severe fall exposure carefully

Falls from elevation consistently rank among the most serious occupational injury categories because they often combine severe physical trauma with long recovery periods and permanent work limitations.

For disability insurers, this creates elevated long-term income replacement exposure, especially in occupations dependent on climbing ability, mobility, strength, and balance.

Why Disability Insurers Focus on Work Ability

What are disability insurers actually protecting?

Disability insurance is primarily designed to protect against income loss caused by injury or illness.

Because of this, disability underwriters focus heavily on whether an injured worker can continue earning income after a severe fall.

Insurers evaluate whether the worker can:

- return to their exact occupation

- return to physically demanding labor

- perform modified duties

- switch to another occupation

- maintain comparable income after injury

Long-term disability claim research from actuarial and disability insurance organizations consistently shows that permanent work limitations create some of the largest income replacement exposures for disability insurers.

Temporary injury vs permanent occupational disability

Disability insurers separate temporary injuries from permanent occupational disability.

| Temporary Injury | Permanent Occupational Disability |

|---|---|

| Short recovery period | Long-term or permanent impairment |

| Worker eventually returns to normal duties | Worker cannot safely return to prior occupation |

| Limited income interruption | Extended income replacement exposure |

| Lower long-term claim severity | Higher long-term income replacement exposure |

This issue is directly connected to permanent disability risk from elevated work, where insurers evaluate whether severe injuries may permanently eliminate a worker’s ability to perform physically demanding occupations.

A worker with spinal instability, chronic neurological pain, or permanent balance problems may never safely return to climbing-heavy occupations again.

That distinction directly affects disability underwriting decisions.

How Insurers Evaluate Severe Fall Exposure

What factors increase disability severity exposure?

Disability insurers use multiple underwriting factors to estimate how severe a fall-related disability claim could become.

Maximum working height

Workers operating at extreme heights generally create higher disability severity exposure because falls from greater heights increase the probability of catastrophic injury.

Disability underwriters also monitor fatal occupational fall statistics to understand long-term occupational injury severity trends affecting elevated workers.

Frequency of climbing

Occasional ladder work creates different underwriting exposure than daily climbing performed for entire shifts.

Repetitive elevated exposure increases cumulative injury probability.

Roof vs tower vs scaffold work

Not all elevated work is classified equally.

| Elevated Work Type | Disability Severity Concern |

|---|---|

| Residential roofing | Repetitive fall exposure |

| Tower climbing | Extreme-height catastrophic injury exposure |

| Scaffold work | Multi-directional fall exposure |

| Bridge work | Complex rescue and severe trauma risk |

Offshore elevated work

Offshore elevated work creates additional disability concern because injured workers may experience delayed rescue and slower emergency medical access.

Disability insurers evaluate whether delayed treatment could increase the likelihood of permanent impairment, long-term recovery problems, or permanent work limitations after a severe fall.

Rescue difficulty

Disability insurers evaluate how quickly injured workers can receive medical treatment after severe falls. Delayed rescue can increase long-term impairment severity.

This underwriting concern is explored further in Rescue Difficulty in High-Elevation Underwriting, where insurers evaluate delayed emergency response exposure in offshore, tower, bridge, and remote elevated occupations.

Physical Job Demands

Highly physical jobs create larger disability exposure because workers depend heavily on mobility, strength, coordination, endurance, and climbing ability.

Underwriting interpretation:

Disability insurers often view physically intensive occupations as higher severity risks because workers depend heavily on full-body function to maintain income-producing work capacity.

Repetitive elevated exposure

Daily elevated work increases cumulative injury exposure over time, especially in physically demanding occupations.

Prior injuries and medical history

Previous back injuries, spinal problems, mobility limitations, neurological conditions, or prior fall injuries may increase underwriting restrictions.

Age

Older workers may face increased disability severity concern because recovery periods may become longer and permanent impairment probability may rise.

Occupations With High Disability Severity Exposure

Roofers

Roofers often work on sloped surfaces with repetitive climbing exposure. Severe falls may permanently affect balance, mobility, and heavy labor ability.

Roofing occupations often receive stricter underwriting review because repetitive elevated exposure creates ongoing severe-fall disability concern.

Tower Climbers

Tower climbers face extreme-height exposure where severe injuries may permanently eliminate climbing capacity and physically demanding work ability.

Tower climbing occupations are frequently categorized as elevated-severity exposure classes because of extreme working heights, rescue complexity, and catastrophic fall potential.

These same severity concerns help explain why workers seeking tower climbers insurance often face stricter underwriting standards, where even a single fall may create permanent work limitations and long-term income replacement exposure.

Structural Ironworkers

Ironworkers frequently operate at significant heights while handling heavy materials, creating elevated catastrophic injury exposure.

Because structural steel work combines height exposure, heavy lifting requirements, and physically demanding labor, structural ironworkers insurance often involves stricter disability underwriting review due to the potential for permanent occupational impairment after severe falls.

Bridge Workers

Bridge work combines elevated fall exposure, difficult rescue conditions, and physically intensive labor requirements.

Many of the factors that influence bridge workers insurance underwriting involve elevated fall exposure, rescue complexity, and the possibility that severe injuries may permanently affect long-term work capacity.

Wind Turbine Technicians

Wind turbine technicians operate in confined elevated spaces where falls may create major spinal or neurological injury exposure.

The combination of extreme working heights, repetitive climbing, and remote work environments helps explain why wind turbine technicians insurance often receives stricter disability underwriting consideration than lower-risk occupations.

Utility Linemen

Utility linemen depend heavily on climbing ability, coordination, and upper-body function. Severe falls may permanently affect occupational performance.

Offshore Elevated Workers

Offshore workers face elevated structures, weather exposure, delayed rescue access, and physically demanding conditions that increase disability severity concern.

Scaffold Erectors

Scaffold erectors experience repetitive elevated exposure while handling heavy materials and unstable positioning.

These occupations often receive stricter underwriting review because severe falls may permanently affect work capacity rather than causing only temporary injuries.

How Fall Severity Modeling in Disability Insurance Affects Coverage

How do severe fall risks affect actual disability coverage?

Disability severity modeling directly affects how insurers price, structure, and approve coverage for elevated workers.

Many disability insurers rely on occupational classification systems similar to those used by the National Council on Compensation Insurance (NCCI) when evaluating elevated occupational risk categories and long-term claim exposure.

Possible insurance consequences include:

Workers with greater severe-fall exposure often pay higher disability insurance premiums because insurers anticipate higher long-term claim costs.

These pricing adjustments are part of the broader underwriting structure explained in Why Elevated Workers Pay More for Insurance, where insurers evaluate injury severity exposure, occupational classification, and long-term claim probability.

Occupational class downgrades

Some elevated occupations are placed into riskier occupational classes that reduce eligibility or increase pricing.

Exclusions

Insurers may exclude certain elevated duties or hazardous occupational activities from coverage.

Limited benefit periods

Some policies shorten the maximum benefit duration available for higher-risk occupations.

Stricter medical underwriting

Workers with prior injuries or elevated exposure may face additional medical reviews, records requests, or functional evaluations.

Reduced monthly benefits

Insurers sometimes limit income replacement amounts for occupations with elevated disability severity exposure.

Denied applications

Applications may be declined when combined fall exposure and disability severity risk exceed underwriting limits.

Applications become more difficult when elevated exposure combines with prior spinal injuries, inconsistent occupational disclosures, or physically intensive full-time labor dependency.

Longer waiting periods

Higher-risk occupations may receive longer elimination periods before benefits begin.

Policy restrictions

Some disability policies contain occupational limitations tied to hazardous elevated work.

Every underwriting decision ultimately connects back to one core question:

Could a severe fall permanently prevent this worker from earning income?

When does severe fall exposure trigger stricter disability underwriting?

Disability underwriting restrictions often increase when multiple elevated-risk factors combine together, such as:

- extreme working heights

- repetitive climbing exposure

- offshore elevated work

- prior spinal injuries

- physically demanding labor dependency

- inconsistent safety history

Some insurers apply formal working-height thresholds and occupational restrictions when elevated exposure exceeds internal underwriting limits. These underwriting limits are closely connected to height restrictions used in some occupational insurance policies for elevated workers.

At certain underwriting thresholds, insurers may:

• reduce available monthly benefits

• increase waiting periods

• apply occupational exclusions

• require additional medical records

• move the worker into a higher-risk occupational class

• decline coverage entirely

Why Severe Disability Claims Receive Heavy Investigation

Why are severe disability claims investigated so closely?

Severe disability claims often involve large long-term payouts. Because of this, insurers investigate occupational disclosures very carefully when elevated workers file claims.

Common claim investigation concerns include:

- undisclosed elevated duties

- omitted offshore work

- material misrepresentation of duties

- hidden prior injuries

- undisclosed physically demanding side jobs

- part-time tower work not reported

- subcontract elevated work omitted from applications

For example:

A worker who applies as a “maintenance technician” but regularly performs tower climbing may create major underwriting discrepancies during claim review.

Similarly, a worker who hides previous spinal injuries may face serious claim complications if permanent disability develops after a fall.

Disability insurers investigate whether:

- the occupation was described accurately

- hazardous duties were fully disclosed

- prior injuries affected underwriting eligibility

- work intensity matched the original application

Accurate occupational disclosure reduces future claim disputes and improves policy reliability.

This issue is closely related to failure-path systems discussed in Common Reasons Claims Are Denied for Risk Jobs.

Real-World Disability Underwriting Examples

Roofer vs Warehouse Worker

A roofer regularly exposed to elevated surfaces creates much greater severe-fall disability exposure than a warehouse worker operating mainly at ground level.

The roofer may face:

- higher premiums

- stricter occupational classification

- reduced policy options

Tower Climber vs Office Electrician

A tower climber working hundreds of feet above ground faces significantly greater catastrophic disability exposure than an office-based electrician performing low-height service work.

Even if both workers share electrical skills, disability severity exposure differs dramatically.

Offshore Ironworker vs Residential Painter

An offshore ironworker faces elevated structures, delayed rescue access, heavy labor exposure, and harsh environmental conditions.

A residential painter may still face ladder exposure but generally creates lower catastrophic disability severity exposure.

Wind Turbine Technician vs Equipment Inspector

A wind turbine technician performs repetitive high-elevation climbing in confined environments.

An equipment inspector performing mostly ground-level assessments usually creates lower permanent disability exposure.

Scaffold Erector vs Administrative Construction Coordinator

A scaffold erector performs repetitive elevated labor with physical positioning demands.

An administrative coordinator working primarily in office environments creates much lower severe-fall disability concern.

“Own Occupation” vs “Any Occupation” Disability Definitions

Why do disability definitions matter so much for elevated workers?

Disability policy definitions heavily affect how claims are evaluated after severe fall injuries.

Own Occupation Disability

“Own occupation” coverage generally means the worker is considered disabled if they cannot perform the duties of their specific occupation.

Example:

A tower climber who permanently loses climbing ability may still qualify for benefits even if they could theoretically perform desk work.

Note: Some insurers offer ‘Modified Own Occupation,’ which pays benefits if you cannot work your specific job but chooses to offset payments if you earn income elsewhere.

Any Occupation Disability

“Any occupation” definitions are stricter.

Under this structure, insurers evaluate whether the worker can perform almost any reasonable occupation based on training, education, or experience.

Example:

A roofer unable to return to roofing work may still be denied ongoing benefits if the insurer determines office-based work remains possible.

For high-risk elevated workers, ‘Any Occupation’ policies often create a coverage gap where a worker is too injured to climb but not injured enough to qualify for benefits under sedentary work standards.

For elevated workers, this distinction matters heavily because their occupations depend on:

- climbing ability

- mobility

- balance

- coordination

- strength

- endurance

- physical positioning

A severe fall may permanently eliminate those abilities even when the worker remains capable of limited sedentary work.

Understanding disability definitions before purchasing coverage is extremely important for hazardous occupations.

OSHA, Safety History & Disability Underwriting

How do insurers interpret safety history?

While individual disability insurance (IDI) is underwritten based on the person, Group Disability underwriters and Workers’ Compensation carriers heavily weigh an employer’s Experience Modification Rate (EMR) and OSHA 300 logs.

Underwriters may review:

- OSHA fall violations

- prior incident history

- employer safety culture

- fall-protection compliance

- repetitive injury patterns

- safety certifications

- training documentation

Strong safety records may improve underwriting confidence because insurers view structured safety practices as indicators of lower catastrophic injury exposure.

Disability insurers may review employer compliance with OSHA fall protection standards when evaluating elevated occupational exposure.

Repeated violations or recurring incidents may increase underwriting restrictions. Repeated OSHA fall violations may also affect broader occupational insurance costs by increasing insurer concern about severe injury exposure and future claim probability.

However, disability insurers are not simply evaluating workplace safety itself.

They are evaluating how safety exposure may increase the probability of severe long-term disability claims.

How Elevated Workers May Improve Disability Insurability

What can elevated workers do to improve disability underwriting outcomes?

Accurately disclose occupational duties

Workers should clearly explain:

- climbing frequency

- maximum working heights

- offshore duties

- tower exposure

- scaffold work

- physically demanding responsibilities

Incomplete descriptions can create future claim disputes.

Maintain certifications

Current safety certifications may improve underwriting confidence and demonstrate structured risk management.

Manage prior injuries responsibly

Workers should properly document treatment history, recovery progress, and medical follow-up for prior injuries.

Maintain strong safety records

Consistent safety compliance may help reduce underwriting concern about repetitive severe injury exposure.

Understand disability policy definitions

Workers should carefully review whether policies use “own occupation” or “any occupation” definitions.

Honestly disclose offshore or tower work

Hidden elevated duties often create major underwriting and claim problems later.

Accurate disclosure improves underwriting accuracy and reduces future claim complications.

Frequently Asked Questions

1. If I can still work a desk job after a severe fall, will disability insurance still pay benefits?

This depends largely on whether your policy uses an “Own Occupation” or “Any Occupation” disability definition. Under an “Own Occupation” policy, you may still qualify for benefits if you can no longer safely perform your specific job duties, such as climbing towers, working on roofs, or performing elevated labor — even if you are physically capable of office work. Under an “Any Occupation” policy, benefits may be denied if the insurer determines you can still perform sedentary or lower-risk work.

2. Why does working at greater heights increase disability insurance premiums?

Disability insurers use fall severity modeling to estimate how serious a fall-related injury could become. Falls from greater heights are statistically more likely to cause spinal injuries, traumatic brain injuries, paralysis, or permanent mobility loss. Because these injuries may prevent a worker from returning to physically demanding occupations permanently, insurers often view higher working heights as greater long-term income replacement exposure.

3. Will a previous back injury automatically prevent me from getting disability insurance?

Not always, but prior back injuries usually trigger stricter disability underwriting review. Insurers may request medical records, evaluate recovery history, or apply exclusions related to pre-existing spinal or musculoskeletal conditions. In some cases, coverage may still be approved, but with higher premiums, modified benefits, or condition-specific restrictions.

4. How does rescue difficulty affect disability underwriting for elevated workers?

Disability insurers evaluate how quickly injured workers can receive emergency medical treatment after a severe fall. Offshore platforms, remote industrial sites, wind turbines, and tower locations may involve delayed rescue access or slower emergency response times. Insurers may view delayed treatment as increasing the risk of permanent impairment, extended recovery periods, or long-term work limitations, which can lead to stricter underwriting decisions.

5. What happens if I fail to disclose occasional tower climbing or offshore elevated work?

Failing to disclose hazardous occupational duties may be treated as a material misrepresentation during underwriting. If a severe injury occurs while performing undisclosed elevated work, the insurer may investigate whether the original application accurately described your occupational exposure. In serious cases, undisclosed tower work, offshore duties, or subcontract elevated labor may lead to claim denial or policy rescission.

Final underwriting insight:

Disability insurers evaluate elevated occupations carefully because severe falls may create permanent work limitations that generate long-term income replacement claims far beyond the initial injury itself.

Key Takeaways

- Disability insurers focus heavily on severe fall injuries because even one catastrophic fall may permanently affect a worker’s ability to earn income.

- Severe falls may permanently affect climbing ability, mobility, balance, strength, and physically demanding work capacity.

- Disability underwriting focuses heavily on long-term income replacement exposure.

- Elevated occupations often receive stricter underwriting classifications and policy limitations.

- Prior injuries, offshore exposure, repetitive climbing, and physically demanding work increase underwriting concern.

- Fall Severity Modeling in Disability Insurance is used to estimate whether severe falls may permanently prevent elevated workers from returning to physically demanding occupations.

- Severe disability claims receive close investigation when occupational disclosures appear incomplete or inaccurate.

- “Own occupation” and “any occupation” disability definitions can dramatically affect claim outcomes for elevated workers.

- Accurate occupational disclosure helps reduce future underwriting disputes and claim complications.

Fall Severity Modeling in Disability Insurance plays a major role in how disability insurers classify elevated occupations, evaluate long-term claim severity, and determine underwriting restrictions.

—————————————————————————————————————————

Workers researching severe-fall disability exposure may also benefit from understanding: