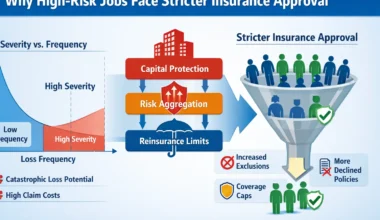

Risk job insurance is the underwriting system insurers use to evaluate, price, and restrict coverage. This system is anchored in the 2018 Standard Occupational Classification (SOC), a federal coding structure that translates daily job tasks into actuarial risk signals. By mapping a worker’s “Direct Match Title” to specific hazard tiers, insurers control high-severity claim exposure. Unlike standard insurance, it applies occupational classification rules, exclusion frameworks, and risk-based pricing models to control high-severity claim exposure.

Executive Summary

Data from International Labour Organization and Occupational Safety and Health Administration shows that hazardous industries produce higher injury severity and fatality rates. As a result, insurers apply stricter underwriting rules, occupational classifications, exclusions, and pricing adjustments when evaluating workers in high-risk jobs.

Where Risk Job Insurance Fits in the Insurance System

Risk job insurance is not a single policy. It is the central framework that connects how insurers:

- classify occupations

- determine eligibility

- adjust pricing and exclusions

- evaluate claims

To understand each component in detail:

- insurance eligibility for high-risk jobs

- occupation class ratings explained

- insurance claims scrutiny for high-risk jobs

These pages expand the individual systems that operate within risk job insurance.

This page serves as the foundational explanation of risk job insurance, with all other guides expanding individual components of this system.

Introduction: When Work Itself Changes the Insurance Rules

Every day, millions of people work in occupations where physical danger is not an occasional possibility but an inherent part of the job. Construction workers operate at height on scaffolding and unfinished structures. Offshore crews spend weeks at sea on drilling platforms surrounded by heavy machinery and volatile energy extraction equipment. Miners work underground in confined spaces with heavy equipment and geological instability. Industrial workers operate powerful machines capable of causing severe injury within seconds.

These environments create a very different risk landscape compared to office or service-sector work.

For most people, insurance appears straightforward. A policy is purchased, premiums are paid, and coverage is expected to protect against unexpected loss. However, for workers in hazardous occupations, insurance rarely behaves that simply.

Policies may cost more.

Coverage may include occupational exclusions.

Claims may be scrutinized more closely.

Certain risks may not be covered at all.

Many workers discover these differences only after an injury, illness, or denied claim reveals how occupational risk affects insurance rules.

Understanding these differences is the purpose of risk job insurance.

This concept explains how insurance systems evaluate dangerous work, classify occupational exposure, adjust underwriting decisions, and define the boundaries of coverage for workers whose jobs involve elevated physical risk.

This guide introduces the full risk job insurance system, including occupational classification, underwriting decisions, coverage exclusions, and claim outcomes for workers in hazardous occupations.

Why This Page Exists

Most insurance resources explain policies, pricing, or coverage types. However, they rarely explain the underlying system that determines how hazardous occupations are evaluated, restricted, and insured.

This page focuses on that system.

How Risk Job Insurance Actually Works (System Overview)

Risk job insurance operates through a structured five-stage system:

- Occupational Classification: This follows SOC Classification Principle #2, which states that occupations are classified based on work performed rather than job titles. This is why a “Lead” who performs manual labor is rated differently than a “Lead” in an office.

- Underwriting filters

- Risk classification assignment

- Policy modification

- Claim evaluation

Each stage controls a different part of risk exposure.

Quick Summary of the System

- Classification defines risk category

- Filters determine eligibility

- Pricing reflects risk level

- Exclusions define limits

- Claims confirm coverage

Why This System Matters

This five-stage structure explains why insurance behaves differently for workers in hazardous occupations.

Unlike standard insurance, where coverage is often assumed to apply broadly, risk job insurance defines coverage boundaries through classification, filtering, and exclusion mechanisms before a claim ever occurs.

Understanding this system allows workers to identify potential coverage gaps early and avoid relying on policies that may not respond as expected.

The Risk Compression Model (How Insurers Reduce Exposure)

Insurers manage hazardous occupations by compressing risk into controllable variables:

- Classification reduces complexity into categories

- Underwriting filters eliminate unacceptable exposure

- Pricing adjusts for expected loss severity

- Exclusions remove catastrophic risk scenarios

This process allows insurers to convert unpredictable occupational risk into structured, measurable exposure.

How Insurers Evaluate High-Risk Workers (Summary)

When assessing high-risk workers, insurers focus on:

- actual job duties (not just titles)

- exposure level (elevate work exposure, offshore, machinery)

- frequency of hazardous tasks

- health and lifestyle factors

These inputs determine classification, eligibility, and pricing decisions.

Full breakdown: how insurance underwriting works for high-risk jobs

The AI Underwriting Audit

In 2026, ‘Black Box’ underwriting is being replaced by transparent AI. If your application is flagged as ‘High Risk’ by an automated system, ask for the Explainability Report. Under 2026 governance frameworks, insurers must be able to prove that their AI didn’t utilize biased or outdated data to surcharge your premium.

Occupational Risk in Hazardous Industries

Hazardous industries consistently produce higher injury severity and fatality rates than standard occupations.

According to Occupational Safety and Health Administration, construction and extraction occupations consistently rank among the highest for fatal workplace injuries, a key factor influencing how insurers design occupational classifications and underwriting thresholds.

From an insurance perspective, higher injury severity increases:

- claim probability

- payout size

- long-term liability

This is why insurers treat these occupations differently from low-risk roles.

Key Components of Risk Job Insurance

| Component | What it controls |

|---|---|

| Occupational classification | Risk grouping |

| Underwriting filters | Eligibility |

| Risk class | Pricing |

| Policy exclusions | Coverage limits |

| Claims evaluation | Payout decisions |

Why Coverage Is Restricted or Modified

For high-risk workers, policies are often adjusted through:

- higher premiums

- occupational exclusions

- restricted benefits

- policy riders

These modifications define what risks are covered — and what are not.

The 2026 Regulatory Impact on Eligibility

As of May 2026, underwriting is no longer just about the worker; it is about the employer’s regulatory footprint. Two specific factors now influence individual eligibility:

-

The 80°F Heat Threshold: Following the expiration of OSHA’s National Emphasis Program, underwriters are requiring proof of written Heat Illness Prevention Plans for outdoor occupations. Lack of a plan can trigger a “substandard” rating for disability policies.

-

Violence Prevention Infrastructure: For healthcare and social service workers, the momentum of H.R. 2531 has forced insurers to scrutinize employer “incident logs.” If an employer cannot show a documented violence prevention committee, the risk is often flagged as “Non-Renewable.”

Evidence: Injury Severity and Insurance Impact

| Industry | Relative Injury Risk | Insurance Impact |

|---|---|---|

| Construction | High | Higher premiums, exclusions |

| Offshore Energy | Very High | Strict underwriting filters |

| Mining | High | Substandard classifications |

| Transportation | Moderate–High | Severity-based pricing |

Can You Get Insurance If You Have a High-Risk Job?

Yes, but coverage depends on how insurers evaluate occupational exposure through underwriting filters and classification systems. Some workers may qualify for standard policies with restrictions, while others may require specialized coverage or face exclusions based on job duties.

Why Do Insurance Claims Get Denied for High-Risk Jobs?

Claims are often denied due to undisclosed job duties, policy exclusions, or changes in occupational risk after policy issuance. These factors create claim breakpoints that insurers use to determine whether coverage applies.

How Insurers Classify High-Risk Occupations

Building on the occupational risk categories above, insurers apply classification systems to group jobs based on expected injury frequency and severity.

These systems are designed to estimate both the likelihood of injury and the potential severity of claims.

These classification systems help insurers estimate how likely injuries are to occur and how severe those injuries may be.

Pro-Tip: The ’80/20 Rule’ for Job Titles

Underwriters often default to the highest-risk category if a job description is vague. If you are a “Working Foreman” or “Site Lead,” explicitly document the percentage of time spent on administrative vs. manual duties.

In 2026, many carriers utilize an 80/20 threshold based on SOC Coding Guideline #5. This guideline specifies that workers in Major Groups 33-0000 through 53-0000 (Construction, Extraction, and Transport) are only classified as “Supervisors” if they spend 80% or more of their time on supervisory activities. If you spend 21% of your time “on the tools,” an insurer may legally reclassify you into a higher-hazard manual tier.

Common high-risk occupations include:

Construction workers

Offshore oil and gas workers

Miners

Heavy equipment operators

Commercial fishermen

Transportation workers

Industrial maintenance technicians

Marine engineers

These occupations share several characteristics that influence insurance risk:

-

frequent exposure to hazardous environments

-

heavy equipment operation

-

high-energy physical work

-

potential for catastrophic accidents

Occupational classification affects several aspects of insurance coverage, including:

-

whether coverage is offered

-

premium pricing

-

policy exclusions

-

underwriting class assignment

-

claim investigation procedures

In many cases, two workers with similar job titles may be treated differently depending on their actual job duties and exposure level.

For example, a construction project manager working primarily in an office may face fewer insurance restrictions than a worker installing structural steel at height, where height exposure significantly increases severity-based risk classification.

Structural Exclusions in Risk Job Insurance

Insurance policies frequently include structural exclusions designed to limit exposure to specific high-risk activities.

These exclusions are especially common in policies issued to workers in high-exposure roles.

Common exclusions include:

Hazardous occupation exclusions

Aviation exclusions

Offshore activity restrictions

Explosives or demolition exclusions

Subsea or deep-water activity limitations

Technical Insight: Many exclusions are triggered by “Residual Categories” (SOC codes ending in “9”, such as 47-5099, Extraction Workers, All Other). According to SOC Coding Guideline #4, these codes are used for tasks not distinctly described in the standard structure. From an underwriting perspective, these “All Other” roles represent “Unquantified Risk.” Consequently, insurers often apply broad Structural Exclusions or “Substandard” ratings to these codes because the specific safety data for the role is missing.

For example, an aviation exclusion may prevent a life insurance policy from covering death resulting from helicopter transportation unless a special rider is added.

Similarly, offshore activity exclusions may restrict coverage for workers performing duties on drilling platforms or marine vessels.

These exclusions are typically embedded within policy terms and may not be obvious to policyholders until a claim occurs.

Understanding these exclusions before purchasing insurance is essential for workers whose occupations involve elevated physical risk.

Why Insurance Claims Fail for High-Risk Workers

Claims typically fail due to:

- undisclosed job duties

- occupational exclusions

- job changes after policy approval

- coverage gaps between employment

Full breakdown: insurance claims scrutiny for high-risk jobs

Claim Breakpoints in High-Risk Insurance

Insurance claims involving hazardous occupations are often subject to additional scrutiny.

Because severe injuries and fatalities can result in large financial payouts, insurers carefully review the details surrounding claims related to dangerous work.

Claim Breakpoint Analysis

| Claim Variable | Underwriting Scrutiny Level | The 2026 “Breakpoint” |

| Duty Consistency | Extreme | Does the injury report align with the “Statement of Required Duties” defined in the 2018 SOC Definitions for that specific code? |

| Safety Compliance | High | Was the worker following a documented Job Hazard Analysis (JHA) at the time of loss? |

| Post-Accident Protocol | Medium–High | Was a DOT-compliant drug test administered within the required window? |

| Certification Status | Critical | Was the worker’s OSHA 30 or NFPA 1582 certification expired on the date of incident? |

For example, if a worker changes jobs after purchasing a policy and fails to update their insurer, the new occupation may fall outside the policy’s coverage rules.

These issues can create disputes during claim investigations and sometimes lead to denied claims.

Understanding how claims are evaluated helps workers avoid misunderstandings that may arise later.

Common Claim Failure Triggers

Insurance claims for workers in hazardous occupations most commonly fail when one or more of the following conditions occur:

- Hazardous job duties were not fully disclosed during application

- Policy exclusions apply to the activity involved in the incident

- Job roles or responsibilities changed after policy issuance without notification

- Coverage gaps exist due to employment or contract changes

These failure triggers represent the most frequent breakpoints in high-risk insurance claims and highlight why accurate disclosure and policy understanding are critical before relying on coverage.

Real-World Scenario: The Certification Gap

In early 2026, a structural welder in an offshore energy role suffered a debilitating back injury. Although his policy was active, the claim was scrutinized because his NFPA 1582 medical fitness certification had expired 10 days prior to the accident.

The Outcome: The insurer moved to deny the disability claim, citing a “Lawful Employment” clause, arguing that the worker was technically ineligible for that specific hazardous duty on the day of the injury. This highlights the “Secondary Eligibility” crisis of 2026: it is not enough to be insured; you must be “currently qualified” according to industry safety standards for the policy to respond.

The “Hybrid-Industrial” Risk Gap

The ‘Remote Risk’ Paradox: If you operate heavy machinery or drones from a remote office, your classification is currently in flux. Insurers may try to charge you a ‘Field Rate’ even if you are in an office. Ensure your policy explicitly defines your ‘Point of Exposure’ to avoid paying construction-level premiums for desk-based operations.

How High-Risk Work Interacts With Different Types of Insurance

Occupational risk affects multiple types of insurance coverage.

Workers in hazardous occupations are often affected by several different coverage systems, which we explain in detail in our guide on types of insurance needed for high-risk jobs.

Each coverage type responds differently to hazardous work.

Common insurance systems affecting high-risk workers include:

Life insurance

Disability insurance

Workers’ compensation

Personal accident insurance

Employer group insurance

Workers’ compensation systems typically cover work-related injuries and illnesses.

Personal disability insurance may provide income replacement when injuries prevent workers from performing their job duties.

Life insurance provides financial protection to families in the event of death.

However, each of these systems may include limitations related to hazardous occupations.

For example, employer group coverage may end when employment stops, while personal policies may include occupational exclusions that affect claim eligibility.

Understanding how these systems interact helps workers build a more complete protection strategy.

The Insurance Stack for High-Risk Workers

Insurance protection for dangerous occupations usually functions as a layered system.

This system can be understood as an insurance stack.

Worker

↓

Employer safety systems

↓

Workers’ compensation coverage

↓

Personal disability insurance

↓

Life insurance protection

↓

Liability and legal protection

Each layer addresses a different type of risk exposure.

Employer safety systems attempt to prevent accidents.

Workers’ compensation covers injuries that occur during employment.

Disability insurance protects income if a worker cannot continue working.

Life insurance protects families against financial loss after death.

Understanding this layered system helps explain why multiple types of insurance may be necessary for workers in hazardous occupations.

Mental Health Parity in Hazardous Roles

“A significant 2026 update to the Mental Health Parity and Addiction Equity Act (MHPAEA) now requires insurers to provide ‘meaningful benefits’ for mental health conditions resulting from high-stress hazardous environments. When reviewing your ‘Insurance Stack,’ ensure your disability policy does not have a ‘Mental/Nervous’ limitation, a common exclusion that is being challenged by new 2026 regulations.”

Why Many Workers Discover Insurance Limits Too Late

Insurance misunderstandings rarely occur because workers are careless.

Instead, they often arise because:

policy language is complex

occupational exclusions are difficult to interpret

employer coverage appears sufficient

job duties change over time

policies are only examined carefully when claims occur

As a result, many workers assume they are fully protected until an accident, illness, or job change reveals gaps in coverage.

These surprises can be avoided when workers understand how insurance rules apply specifically to hazardous occupations.

Failure-Path Checklist for High-Risk Workers

Before relying on any insurance policy, confirm:

- Your job duties are fully and accurately disclosed

- No occupational exclusions apply to your role

- Your policy reflects your current job responsibilities

- Coverage remains active between contracts or employment changes

- Any offshore, aviation, or hazardous activities are explicitly covered

Recognizing these potential failure paths helps workers ask the right questions before relying on insurance coverage.

Why Risk Job Insurance Is Treated Differently from Standard Insurance

Standard insurance models are designed for low-frequency, predictable risk environments where severe injury or fatality is relatively uncommon. In these cases, insurers can spread risk across large populations with similar exposure profiles.

High-exposure roles operate under a different risk structure.

Workers in industries such as construction, offshore energy, mining, and heavy equipment operation are exposed to conditions where both the probability and severity of loss are significantly higher. Data from International Labour Organization and Occupational Safety and Health Administration shows that hazardous industries consistently produce higher injury severity and fatality rates, which directly drives underwriting restrictions, classification models, and claim evaluation standards used by insurers.

Because of this, insurers cannot apply standard underwriting assumptions.

Instead, they must control risk through:

- Occupational classification systems

- Underwriting filters that limit eligibility

- Pricing adjustments tied to risk exposure

- Policy exclusions targeting high-severity activities

- Enhanced claim review processes

This structural difference is why risk job insurance exists as a distinct underwriting framework rather than a variation of standard insurance.

How Risk Job Insurance Connects to Other Guides

This page serves as the central pillar of the Risk Job Insurance system.

Each component of this system is explained in detail in the following guides:

- insurance eligibility for high-risk jobs — how insurers decide whether coverage is approved

- occupation class ratings explained — how jobs are grouped and priced

- insurance claims scrutiny for high-risk jobs — how claims are reviewed and denied

- Workers exposed to elevated environments may also face additional underwriting restrictions under height exposure underwriting models, particularly when fall severity exposure exceeds carrier thresholds.

Together, these pages form a complete framework for understanding how insurance works in hazardous occupations.

Key Takeaways

- Risk job insurance is a system, not a single policy

- Occupational classification determines how insurers evaluate risk

- Underwriting filters control eligibility for high-risk workers

- Policy exclusions define coverage limits before claims occur

- Claim failures often result from nondisclosure or risk changes

Final Summary

Risk job insurance is the system that governs how hazardous work is evaluated, insured, and paid during claims. It defines eligibility, pricing, exclusions, and claim outcomes for workers exposed to elevated occupational risk.

Unlike standard insurance, which assumes relatively stable risk conditions, hazardous work introduces high-severity exposure that forces insurers to rely on classification systems, underwriting filters, exclusions, and strict claim evaluation processes.

Understanding how this system operates allows workers to identify coverage limitations, avoid common failure paths, and make informed decisions before relying on any insurance policy tied to dangerous work environments.

Pro-Tip: Verify Your Direct Match Before applying for coverage, consult the 2018 SOC Direct Match Title File. This document contains thousands of specific titles used by underwriters to “crosswalk” your self-reported job name into a 6-digit risk code. Finding your Direct Match before you apply prevents the common “Misclassification Breakpoint” where a claim is denied because your title didn’t match the insurer’s internal risk map.

Frequently Asked Questions

Can I get life insurance if I work offshore?

Yes, but approval depends on underwriting risk classification, employer safety protocols, and your offshore role. High-risk workers often face exclusions, higher premiums, or specialized policies. See our offshore insurance eligibility guide for exact approval criteria and failure triggers.

Why was my disability claim denied for a hazardous job?

Most denials occur due to misclassification, undeclared job duties, policy exclusions, or failure to meet medical proof requirements. Hazardous occupations are heavily scrutinized during claims. Review our claims scrutiny guide for exact denial triggers and how to avoid them.

How does OSHA 2026 impact my insurance premiums?

OSHA 2026 regulations increase compliance requirements, which insurers use to adjust risk scoring. Employers with poor compliance records or higher incident rates may see increased premiums, while compliant operations may benefit from reduced costs. See the regulatory impact section above for underwriting implications.

Written by: Risk Job Insurance Editorial Team

Updated: May 2026

Grounding Sources: NCCI 2026 State of the Line Report; OSHA Heat Injury Rulemaking (2026); ILO Global Manual on Hazardous Occupations.