Executive Summary

High-risk insurance policies contain more exclusions because hazardous occupations create greater injury severity, operational unpredictability, and catastrophic exposure potential. Insurers use exclusions to define sustainable coverage boundaries, control concentrated loss exposure, and maintain coverage availability within dangerous industries where claim volatility is significantly higher than standard occupational categories.

Introduction: When Coverage Exists, but Protection Feels Limited

Many high-risk workers are surprised to learn that even after being approved for insurance, coverage can feel narrower than expected. A policy may be active, premiums may be paid, yet certain situations are excluded in ways that feel restrictive or unfair.

This is especially common in dangerous work.

In this guide, we explain insurance exclusions for high-risk jobs, why they exist, and what they actually mean in real situations.

Construction workers, offshore crews, industrial operators, transport workers, and others in hazardous roles often encounter policies with more exclusions than their peers in low-risk jobs. These exclusions are frequently misunderstood because workers often interpret policy activation as universal protection rather than coverage limited by predefined exposure boundaries.

In reality, exclusions are a core structural feature of how insurance functions when work involves higher-than-average risk.

This guide explains why insurance policies for high-risk jobs contain more exclusions, what those exclusions actually mean, and how they fit into the broader risk job insurance explained.

What Insurance Exclusions for High-Risk Jobs Actually Are

An exclusion is a clearly defined boundary that specifies which risks the insurer did not agree to cover when the policy was issued. It exists to limit exposure to events that fall outside the insurer’s risk tolerance.

Exclusions do not remove coverage retroactively. They define coverage from the beginning.

This distinction matters because many disputes arise from the assumption that exclusions are added later or used to avoid paying claims. In reality, exclusions are part of the original agreement and are one of the ways insurers make coverage possible at all.

Understanding exclusions as boundaries rather than penalties helps explain why they are more common in high-risk work.

Why High-Risk Jobs Require More Exclusions

To understand why exclusions increase in dangerous work, it helps to look at how insurers respond when risk becomes harder to predict and more expensive to manage.

High-risk jobs introduce several challenges at once:

– Injuries occur more frequently

– Outcomes tend to be more severe

– Recovery periods are longer

– Costs are less predictable

Evidence block:

According to the International Labour Organization (ILO), hazardous industries consistently experience higher injury severity, fatality rates, and longer recovery periods than lower-risk occupations. Elevated claim volatility increases insurer exposure uncertainty, which is why high-risk insurance systems rely more heavily on exclusions, underwriting controls, and coverage boundaries than standard occupational insurance structures.

When both the likelihood and cost of claims increase, insurers must control exposure carefully. One way they do this is by excluding risks that are too volatile, too severe, or too difficult to price sustainably.

Insurers also use exclusions to reduce correlated-loss exposure, where multiple severe claims within the same occupational category can threaten portfolio stability across an insurance pool.

Without exclusions, premiums would rise sharply or coverage would become unavailable altogether.

Exclusion structures may also reflect reinsurance requirements, where insurers transferring catastrophic occupational exposure to larger risk-sharing entities must comply with externally imposed exposure restrictions.

Exclusions are therefore not a sign of hostility toward high-risk workers; they are a mechanism that allows insurance to exist in dangerous work environments.

Insurance systems are built to manage uncertainty. These exclusion structures operate within a broader insurance ecosystem involving workers’ compensation, disability insurance, occupational accident coverage, and liability systems explained in types of insurance for high-risk jobs.

When uncertainty increases, rules become more specific. These exclusions exist because dangerous work concentrates risk, requiring insurers to clearly define what they can and cannot absorb.

How Exclusions Are Decided During Underwriting

Exclusions are not created during claims. They are decided much earlier, during underwriting.

Underwriting is the stage where insurers assess:

-

What duties a worker performs

-

How often hazardous tasks occur

-

Where the work takes place

-

How injuries are likely to happen and resolve

Based on this assessment, insurers decide which risks they can accept and which must be excluded.

Decision breakpoint (exclusion-setting):

Exclusions in hazardous occupation insurance often increase when underwriting identifies exposure patterns associated with catastrophic loss potential, operational instability, or inconsistent risk predictability.

Common exclusion triggers include:

– Offshore or underground operations

– High-severity equipment exposure

– Remote or isolated worksites

– Non-routine operational tasks

– Frequent contractor transitions

– Multi-jurisdictional work environments

– Undeclared hazardous secondary duties

As exposure volatility increases, insurers may narrow coverage boundaries to prevent concentrated loss exposure within high-risk occupational categories.

This broader process of balancing exclusions, limits, underwriting controls, and exposure segmentation is part of how insurers structure coverage for hazardous occupations.

These decisions are made before a policy is issued and are reflected in the policy’s written terms.

This is why exclusions often feel technical or specific. They are tied directly to exposure patterns identified during underwriting, not to individual claim behavior.

We explain this process step-by-step in our guide on insurance eligibility for high-risk jobs

Common Types of Exclusions in High-Risk Work

Exclusions in high-risk jobs tend to fall into predictable categories. While wording varies, the underlying logic is consistent.

Duty-specific exclusions: These limit coverage for particular tasks that significantly increase risk.

Environment-based exclusions: These apply to work performed in especially unpredictable or remote settings.

Task-triggered exclusions: Coverage may be excluded when specific high-risk actions are involved, regardless of job title.

Time-based exclusions: Some exclusions apply during certain phases of work, such as transit or non-routine operations.

Condition-related exclusions: Pre-existing injuries or conditions may be excluded when combined with hazardous duties.

These categories exist to separate manageable risk from unmanageable exposure.

Why Job Duties Matter More Than Job Titles for Exclusions

Exclusions are driven by exposure, not labels. Many workers misunderstand insurance exclusions for high-risk jobs, assuming they are tricks or hidden clauses. In reality, they define the boundaries insurers can safely cover.

Two workers with the same job title can have very different exclusion profiles if their daily duties differ.

Insurers use occupational classification systems to separate workers into different underwriting categories based on exposure severity, operational environment, and frequency of hazardous activity. These classifications directly influence which exclusions become necessary within a policy structure.

One may perform hands-on hazardous tasks regularly, while another with the same title may work primarily in a supervisory or monitoring role.

This is why exclusions are tied to what a worker actually does, not what their role is called. Temporary duties, undocumented task changes, or informal role expansions are common sources of confusion at claim time.

Clear understanding of how duties affect exclusions helps explain why outcomes can differ even among workers who appear to do the same job.

This is why exclusions follow exposure rather than job titles, reflecting the reality that job duties matter more than job titles when insurance risk is assessed.

How Exclusions Affect Claims (Where Confusion Happens)

Exclusions become most visible when a claim is filed.

At claim time, insurers examine whether the event falls inside or outside the boundaries defined in the policy. When an injury or loss aligns with an exclusion, the claim may be denied even though the policy is active.

This outcome often feels personal, but it reflects enforcement of agreed boundaries rather than a new decision.

Many high-risk claim disputes arise not because coverage was absent, but because exclusions were misunderstood. Recognizing this difference helps reduce frustration and misinterpretation when claims are reviewed closely.

When a claim falls near an exclusion boundary, it often triggers closer review, and claims near these boundaries are reviewed more carefully because the policy must be applied exactly as written.

We explore what happens at the very edge of coverage, when exclusions, limits, and definitions can no longer respond, in our guide on when insurance coverage truly ends for high-risk workers.

Where Exclusions Commonly Break Coverage

Coverage disputes involving exclusions frequently emerge at structural boundary points where actual work exposure differs from the occupational profile originally evaluated during underwriting.

Common breakdown scenarios include:

– Temporary expansion into hazardous duties

– Undeclared operational changes

– Informal role transitions

– Work performed outside declared geographic regions

– Contractor activity outside approved classifications

– Non-routine tasks performed during emergencies or shutdown operations

In many cases, the policy itself remains active, but the event falls outside the exposure boundaries the insurer originally agreed to cover.

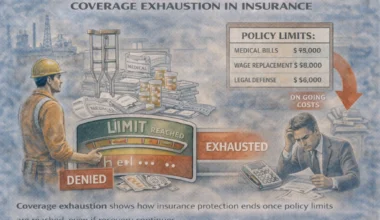

Why Exclusions Do Not Mean Coverage Is Useless

It is natural to assume that more exclusions mean weaker coverage. In practice, exclusions often make coverage possible.

Without exclusions, insurers would need to:

-

Raise premiums substantially

-

Reduce benefit amounts

-

Decline coverage altogether

Exclusions allow insurers to offer coverage at prices that remain viable while still protecting against defined risks. These structural trade-offs become more visible when combined with policy payout ceilings, which we explain in policy limits in high-risk insurance. They are part of a trade-off between availability, affordability, and scope.

For high-risk workers, understanding this trade-off helps explain why coverage exists with limits rather than not existing at all.

Because no single policy is designed to absorb every kind of risk, many workers need layered protection, which we break down in Why High-Risk Workers Often Need More Than One Insurance Policy.

How Exclusions Fit Into Risk Job Insurance as a System

Exclusions are one component of a larger system.

Within risk job insurance, coverage is shaped by:

– Eligibility, which determines whether coverage can exist

– Underwriting, which defines acceptable risk

– Pricing, which reflects exposure

– Exclusions, which limit volatility

– Claims, which enforce these rules in practice

At claim stage, exclusions function as enforceable structural boundaries rather than flexible guidelines. Once a claim falls outside the exposure categories defined during underwriting, coverage may no longer apply even when the policy itself remains active.

Exclusions operate alongside eligibility, underwriting, pricing, and claims as part of the broader risk job insurance system that governs coverage for dangerous work.

These boundaries also help explain why employer coverage is often limited on its own, which we explore in Why Employer Insurance Often Isn’t Enough for High-Risk Workers.

Exclusions work alongside limits and definitions to keep insurance aligned with real-world risk.

Beyond these boundaries lies the point where insurance can no longer continue at all, which we explain in When Risk Becomes Un-insurable for High-Risk Workers (And Why Insurance Can’t Follow You Further).

Frequently Asked Questions

Why do high-risk insurance policies contain more exclusions than standard insurance?

Because hazardous occupations create greater uncertainty around injury severity, catastrophic exposure, operational variability, and claim predictability. Insurers respond by narrowing coverage boundaries to maintain financial sustainability within high-volatility occupational categories.

Can exclusions change after job duties change?

Yes. Significant changes in operational exposure, hazardous task frequency, geographic work environment, or contractor status may trigger underwriting reassessment and alter exclusion structures at renewal or policy modification stage.

Why do workers with similar jobs receive different exclusions?

Because insurers evaluate actual exposure patterns rather than job titles alone. Two workers with similar titles may perform different tasks, operate in different environments, or face different levels of catastrophic exposure.

Conclusion: Exclusions Define Boundaries, Not Intent

Insurance policies for high-risk jobs contain more exclusions because dangerous work changes how risk must be managed.

In high-risk jobs, exclusions often show up as:

-

exclusions for offshore or remote duties

-

exclusions tied to specific machinery or tasks

-

exclusions during transport or non-routine operations

-

exclusions triggered by undisclosed job changes

Exclusions are not judgments about workers. They define where coverage begins and ends, so insurance can remain available in jobs where risk is concentrated.

In structural terms, exclusions function as exposure-management mechanisms that allow insurers to define sustainable coverage boundaries within occupations characterized by elevated injury severity and unpredictable operational risk.

Final underwriting insight:

Exclusions are not designed primarily around the possibility of denying claims. They are designed around defining sustainable exposure boundaries within occupational categories capable of generating unpredictable or catastrophic losses.

For high-risk workers, understanding what exclusions mean reduces surprise, prevents confusion at claim time, and clarifies how insurance actually functions when work itself carries greater danger.