Editorial notice: Reviewed for underwriting accuracy by the RJI Institutional Review Team | Published: May, 2026 | Last reviewed: June, 2026

—————————————————————————————————————————

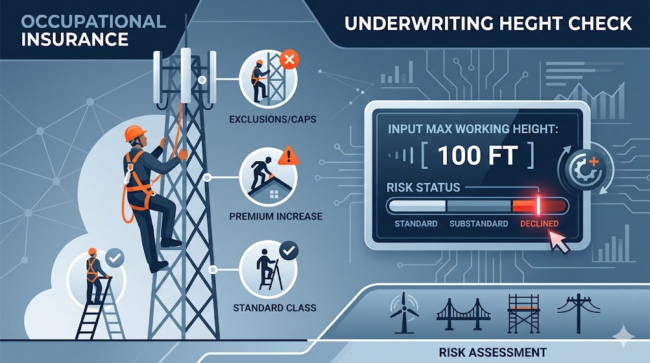

Height Restrictions in Occupational Insurance Policies affect many workers involved in roofing, tower climbing, bridge work, scaffolding, offshore maintenance, and other elevated occupations. Insurers often apply working-height limitations, occupational exclusions, benefit caps, or stricter underwriting rules because severe falls can create expensive disability, liability, and fatality claims.

Executive Summary

Many insurance policies place restrictions on elevated work because severe falls from roofs, towers, scaffolding, bridges, offshore platforms, and industrial structures can create expensive disability, liability, and fatality claims. As working height increases, the insurer’s exposure shifts from “Frequency Risk” (many small claims) to “Severity Risk” (one catastrophic claim). This shift is what triggers policy exclusions and premium hikes.

What Are Height Restrictions in Occupational Insurance Policies?

Height restrictions are underwriting rules insurers use to limit or control coverage for people who work above certain elevations. These restrictions are designed to manage severe injury exposure linked to elevated occupations.

Standard Industry Thresholds: The “Line in the Sand”

Underwriters generally look at height through two globally recognized benchmarks:

- The 2-Meter / 6-Foot Rule: This is the universal baseline. Anything below this is typically covered under standard, non-elevated insurance terms. Once you cross this line, you are officially “working at height.”

- The 10-Meter / 30-Foot Rule: This is where standard public liability and disability policies pivot. Exceeding 10 meters triggers specialized risk assessments, mandatory safety plan verifications, and premium surcharges.

In practical terms, a policy may:

- refuse coverage above certain working heights

- exclude tower climbing entirely

- limit disability benefits for elevated occupations

- restrict offshore elevated work

- cap coverage for high-elevation contractors

- apply stricter underwriting classifications

Insurers commonly use these restrictions for occupations involving:

- communication towers

- wind turbines

- bridges

- scaffolding

- structural steel work

- offshore platforms

- industrial maintenance structures

For example, a disability insurer may insure a warehouse maintenance worker who occasionally uses ladders but decline or heavily restrict a full-time tower climber working hundreds of feet above ground.

The underwriting logic is simple:

Greater elevation exposure usually means greater catastrophic injury exposure.

That connection often drives:

height exposure → insurer concern → policy restriction

This underwriting framework closely relates to Height Exposure Underwriting: How Insurers Evaluate Elevated Workers, where insurers analyze maximum elevation, exposure frequency, rescue conditions, and catastrophic injury severity before determining eligibility and pricing structures.

Why Do Insurers Impose Height Restrictions?

Insurers focus heavily on severity risk, not just accident frequency.

A fall from a short ladder may result in a minor injury. A fall from a communication tower, bridge structure, offshore platform, or wind turbine may result in permanent disability or fatal injuries.

Federal injury surveillance data from National Institute for Occupational Safety and Health (NIOSH) fall prevention research consistently shows that falls remain one of the leading causes of severe occupational injuries in elevated trades.

That severity difference changes underwriting decisions dramatically.

This is directly connected to Catastrophic Fall Risk in Occupational Insurance, where insurers evaluate how severe elevated falls can trigger permanent disability exposure, long-term income replacement costs, fatality claims, and major employer liability losses.

Insurers commonly evaluate:

- catastrophic fall potential

- permanent disability exposure

- fatality risk

- rescue difficulty

- long-term medical costs

- lifetime income replacement exposure

- employer liability severity

- rehabilitation costs

As working height increases, insurers often view catastrophic exposure as becoming more severe, more expensive, and harder to predict accurately.

For example:

| Elevated Exposure | Typical Underwriting Concern |

|---|---|

| Low ladder work | Moderate injury exposure |

| Multi-story roofing | Severe fall claims |

| Tower climbing | Catastrophic disability exposure |

| Offshore elevated work | Rescue complexity + fatality exposure |

| Bridge ironwork | High-severity structural fall risk |

This is why insurers frequently separate elevated occupations into different underwriting classes rather than treating all “construction” or “maintenance” work the same.

Types of Height Restrictions Insurers Use

Insurers use several different restriction models when underwriting elevated occupations.

Maximum Working Height Limits

Some policies only allow coverage below specific elevations.

Examples include:

- no work above 15 feet

- restrictions above 30 feet

- exclusions for work above 50 feet

- automatic referral requirements for tower work

Once a worker exceeds those thresholds, underwriting limits often become stricter, premiums may increase substantially, or coverage may be denied entirely.

Common Height Thresholds Insurers Evaluate

While underwriting rules vary between carriers, several working-height thresholds commonly trigger stricter underwriting review:

| Height Threshold | Typical Underwriting Impact |

|---|---|

| Above 6 feet / 2 meters | Basic elevated-work classification begins |

| Above 15 feet | Increased occupational review |

| Above 30 feet / 10 meters | Higher-risk underwriting classification |

| Above 50 feet / 15 meters | Major premium increases or exclusions |

| Tower and extreme-elevation work | Possible decline or specialized underwriting |

Underwriting Note: The 50-foot (15-meter) threshold directly mirrors the explicit occupational exclusions frequently found in international high-risk and critical illness policies.

These thresholds are not universal rules, but many insurers use similar elevation benchmarks when evaluating catastrophic fall exposure.

Tower-Climbing Exclusions

Tower climbing is one of the most heavily restricted elevated-risk occupations in insurance underwriting because catastrophic fall exposure and rescue difficulty can create severe long-term claims costs.

Many insurers view:

- communication towers

- cellular towers

- broadcast towers

- transmission structures

as severe fall-risk occupations due to:

- extreme height exposure

- difficult rescue conditions

- fatality severity

- spinal injury risk

Some policies completely exclude tower-related injuries.

Scaffold-Work Restrictions

Scaffold exposure creates concern because workers often:

- move continuously at elevation

- carry equipment

- work in unstable weather conditions

- operate around incomplete structures

Underwriters may limit disability coverage or raise premiums substantially for full-time scaffold workers.

Offshore Elevated-Work Restrictions

Offshore elevated work combines multiple underwriting concerns, including rescue difficulty, delayed extraction capability, environmental hazards, and catastrophic injury exposure:

- elevation exposure

- environmental hazards

- remote rescue difficulty

- delayed emergency response

This concern overlaps heavily with Rescue Difficulty in High-Elevation Underwriting, where insurers evaluate how delayed extraction capability, remote access limitations, and difficult emergency recovery conditions can increase catastrophic claim severity.

Because of this, offshore elevated workers often face:

- restricted carrier availability

- benefit caps

- occupational exclusions

- longer waiting periods

Occupational Reclassification

A worker initially classified as “maintenance” may be reclassified into a higher-risk category after underwriters discover elevated duties.

This process is closely tied to Occupational Hazard Classification in Insurance, where insurers group occupations according to injury severity potential, operational hazards, rescue difficulty, and long-term claims exposure.

This type of occupational mismatch is sometimes referred to as classification drift, where the reported job title no longer reflects the worker’s actual exposure severity.

For example:

| Reported Occupation | Actual Duties | Possible Underwriting Result |

|---|---|---|

| Electrician | Utility pole climbing | Higher-risk classification |

| Maintenance worker | Tower climbing | Restricted coverage |

| Painter | Industrial tower painting | Premium increase |

| Technician | Wind turbine repair | Disability limitations |

Underwriters frequently discover that real-world operational exposure differs significantly from the occupational description originally provided during application review.

Benefit Limitations and Policy Caps

Some insurers reduce maximum available benefits for elevated workers because catastrophic claims can become extremely expensive.

Restrictions may include:

- lower disability benefit limits

- capped accidental death payouts

- shorter benefit periods

- stricter elimination periods

- reduced policy maximums

Restricted Coverage for Side Work

Many elevated workers perform subcontract or side jobs that insurers never initially evaluated.

Examples include:

- weekend roofing work

- side tower maintenance

- subcontract scaffold work

- offshore contract assignments

Undisclosed side work can create serious claim disputes later.

Structural exclusion model: Insurers often isolate high-uncertainty elevated exposures they believe cannot be priced accurately without stricter underwriting verification.

How Height-Based Underwriting Decisions Usually Work

Insurers often evaluate elevated occupations using a layered severity review process:

- Occupational classification → What type of elevated work is performed?

- Maximum working height → How high does the worker regularly operate?

- Frequency of exposure → Is elevated work occasional or daily?

- Rescue complexity → How difficult would emergency recovery be after a fall?

- Historical claims severity → Has this occupation produced catastrophic disability or fatality claims historically?

Once severity exposure crosses internal underwriting thresholds, insurers may:

- increase premiums

- reduce available benefits

- apply exclusion riders

- require additional underwriting review

- decline coverage entirely

Some insurers maintain very limited underwriting appetite for extremely elevated-risk occupations because catastrophic fall severity can exceed the pricing tolerance of standard occupational insurance models.

From the insurer’s perspective, elevated work becomes difficult to price once severe injury exposure combines with rescue complexity, unpredictable fall conditions, and long-term disability probability.

Which Occupations Are Commonly Affected by Height Restrictions?

Roofers

Roofing combines frequent elevation exposure with high fall frequency. Insurers often apply premium increases, exclusions, or disability limitations.

This underwriting concern closely relates to Why Roofers Face Strict Insurance Underwriting, where insurers evaluate repetitive elevation exposure, catastrophic fall frequency, ladder dependency, weather-related hazard exposure, and long-term disability severity associated with roofing occupations.

Tower Climbers

Tower climbing is frequently considered one of the highest-severity occupational classes because of extreme elevation and difficult rescue conditions.

This underwriting profile closely aligns with Tower Climbers Insurance, where insurers evaluate extreme height exposure, rescue complexity, catastrophic fall severity, transmission-structure access, and long-term disability risk associated with communications infrastructure work.

Bridge Workers

Bridge ironworkers and structural bridge crews face severe underwriting scrutiny because falls over water, traffic, or steel structures can create catastrophic injuries.

This elevated-risk profile closely relates to Bridge Workers Insurance, where insurers analyze structural fall exposure, over-water operations, traffic-adjacent hazards, rescue difficulty, and high-severity injury potential associated with bridge construction and maintenance work.

Structural Ironworkers

Insurers evaluate:

- exposed steel work

- incomplete structures

- multi-story elevation

- harness dependence

These factors can trigger higher-risk occupational classifications.

These underwriting considerations closely relate to Structural Ironworkers Insurance, where insurers evaluate exposed steel erection, multi-story elevation exposure, incomplete structural environments, fall-arrest dependency, and catastrophic injury severity when determining occupational classification, pricing, and coverage eligibility.

Wind Turbine Technicians

Wind turbine work combines:

- extreme heights

- confined access

- remote rescue conditions

- severe weather exposure

This often leads to restricted disability coverage availability.

These underwriting concerns are examined in greater detail in Wind Turbine Technicians Insurance, where insurers evaluate turbine height exposure, confined-access systems, remote rescue limitations, severe weather conditions, and catastrophic injury severity.

Utility Linemen

Utility line work creates elevated injury exposure involving poles, energized systems, and difficult rescue scenarios.

Scaffold Workers

Scaffold workers may experience stricter underwriting because of unstable platforms and continuous elevated movement.

Offshore Maintenance Workers

Offshore elevated maintenance work combines:

- remote access

- rescue delays

- severe weather

- structural elevation exposure

This frequently produces stricter policy limitations.

How Height Restrictions Affect Different Types of Insurance

Disability Insurance

Disability insurers focus heavily on whether a worker could permanently lose the ability to perform elevated duties.

Disability carriers frequently use height restrictions in occupational insurance policies when evaluating long-term catastrophic injury exposure for elevated workers.

Severe falls may create:

- spinal injuries

- mobility limitations

- traumatic brain injuries

- long-term work-loss exposure

This is why elevated workers often face:

- lower benefit caps

- occupation exclusions

- stricter underwriting reviews

Related reading: Disability Insurance for High-Risk Workers

Workers’ Compensation

Workers’ compensation policies generally cannot exclude covered workplace injuries, but insurers still evaluate:

- employer safety history

- OSHA violations

- elevated incident frequency

- claims severity trends

Poor elevated-risk management can increase employer premiums significantly.

Occupational Accident Insurance

Occupational accident policies sometimes contain strict language regarding:

- elevated duties

- subcontract work

- offshore assignments

- hazardous classifications

Coverage disputes may occur if duties were inaccurately disclosed.

Life Insurance

Life insurers may:

- increase premiums

- reduce available coverage

- classify applicants differently

Depending on how often they work at elevation.

Accidental Death & Dismemberment Coverage

AD&D carriers closely examine catastrophic fall exposure because high-elevation deaths and severe injuries can trigger large payouts.

Employer Liability Coverage

Employers performing elevated work may face higher liability premiums due to:

- catastrophic injury potential

- severe legal exposure

- rescue complexity

- long-term settlement costs

These pricing increases are closely related to Why Elevated Workers Pay More for Insurance, which explains how catastrophic exposure probability, disability severity, rescue complexity, and elevated underwriting limits influence premium calculations.

In some industries, standard liability coverage may not fully extend to high-elevation operations. Employers performing tower work, structural steel installation, industrial rope access, or high-rise maintenance sometimes require specialized elevated-risk endorsements or contractor-specific liability coverage.

Standard Policies vs Specialized Elevated-Risk Policies

Workers involved in tower climbing, industrial rope access, structural steel work, or offshore elevated operations often require specialty coverage structures designed specifically for elevated-risk occupations and catastrophic exposure management.

| Coverage Type | Typical Height Treatment |

|---|---|

| Standard business liability policy | Often includes height limitations |

| Standard disability insurance | May restrict elevated occupations |

| Specialized contractor liability policy | Designed for high-elevation exposure |

| Elevated-risk occupational accident coverage | Broader catastrophic fall consideration |

| Tower and industrial specialty policies | Underwritten specifically for severe height exposure |

Why Undisclosed Elevated Work Creates Claim Problems

This is one of the biggest failure paths in occupational insurance underwriting.

Severe fall claims frequently trigger detailed occupational investigations because insurers want to verify:

- actual job duties

- elevation exposure

- subcontract activities

- offshore assignments

- side work involvement

Common disclosure problems include:

| Disclosure Issue | Potential Claim Problem |

|---|---|

| “Maintenance worker” instead of tower climber | Misclassification investigation |

| Undisclosed roofing side work | Coverage dispute |

| Hidden offshore duties | Occupational exclusion review |

| Unreported subcontract climbing work | Claim denial risk |

| Inaccurate working-height description | Policy rescission review |

Decision breakpoint in occupational underwriting often occurs when elevated exposure combines with undisclosed duties, conflicting application information, or severe-risk classifications that exceed simplified underwriting limits.

Insurers investigate these claims closely because catastrophic falls create high financial exposure.

Claims scrutiny usually increases dramatically once injuries involve permanent disability, fatal falls, spinal trauma, or undisclosed elevated subcontract work.

Related reading: Common Reasons Claims Are Denied for Risk Jobs

Real-World Underwriting Examples

| Occupation | Primary Height Risk | Common Restriction |

| Residential Roofer | Frequency of falls | Premium loading (higher cost) |

| Tower Climber | Catastrophic fatality/disability | Total exclusion or benefit caps |

| Wind Turbine Tech | Rescue complexity / Remote location | Limited disability benefit periods |

| Bridge Ironworker | High-impact structural fall | Stricter underwriting “referrals.” |

Underwriting severity model: occupations involving extreme elevation, rescue difficulty, and permanent disability exposure typically receive the strictest policy restrictions.

Why Do Disability Insurers Use Height Restrictions?

Disability underwriting focuses heavily on long-term income replacement exposure.

Severe spinal trauma and permanent mobility impairment are major underwriting concerns because elevated falls can permanently remove workers from physically demanding occupations, according to spinal cord injury information.

A severely elevated work injury may permanently prevent a worker from returning to:

- roofing

- tower climbing

- structural steel work

- utility climbing

- offshore maintenance

That creates major financial exposure for disability insurers.

This exposure overlaps directly with Permanent Disability Risk from Elevated Work, where insurers evaluate how spinal trauma, mobility loss, traumatic brain injuries, and permanent occupational impairment can create long-term disability payment exposure following severe elevated falls.

Related reading: Fall Severity Modeling in Disability Insurance

Disability carriers evaluate:

- probability of permanent impairment

- inability to return to elevated work

- spinal injury exposure

- rehabilitation duration

- long-term monthly benefit costs

Height restrictions become stricter when insurers believe a fall could permanently remove a worker from their occupation.

This decision framework aligns closely with broader occupational underwriting systems that classify workers according to catastrophic claim severity exposure.

How Do OSHA Violations Affect Height Restrictions in Insurance?

Insurers also evaluate how safely elevated work is performed.

Insurers often review OSHA fall protection standards because repeated violations can signal elevated future claim severity exposure.

Underwriters commonly review:

- OSHA fall violations

- prior elevated incidents

- rescue preparedness

- safety certifications

- employer claims history

- fall-protection compliance

- documented safety programs

Related reading: OSHA Fall Violations and Insurance Costs

A company with repeated fall violations may face:

- higher premiums

- stricter underwriting

- coverage restrictions

- reduced carrier options

Meanwhile, employers with strong safety records and verified fall-protection systems may reduce underwriting concerns.

The Safety Catch: Conditional Payout Risk

Even when a policy is active, severe fall claims may trigger detailed investigations into whether legally required fall-protection systems were being properly used at the time of the incident.

Insurers and claims investigators often review:

- harness usage

- guardrail systems

- anchor-point compliance

- rescue procedures

- documented safety enforcement

- OSHA fall-protection violations

If investigators determine that mandatory safety procedures were knowingly ignored, insurers may dispute portions of the claim, enforce policy exclusions, increase employer liability scrutiny, or reassess future coverage eligibility depending on the policy structure and jurisdiction involved.

From an underwriting perspective, safety compliance is not viewed as a simple regulatory formality. It is treated as part of the operational risk controls supporting the policy itself.

How Workers and Employers Can Reduce Height Restriction Problems

Workers and employers can reduce underwriting problems by improving disclosure accuracy and maintaining strong safety documentation.

Insurers often make underwriting decisions based on incomplete occupational descriptions. Creating a detailed exposure profile helps reduce classification disputes later.

The Disclosure Checklist

Before signing a policy, ensure you have documented:

[ ] Max Ceiling: Your absolute maximum working height in feet.

[ ] Frequency: What % of the week is spent above 15ft/30ft/50ft?

[ ] Safety Gear: Specific brands/types of fall arrest systems used.

[ ] Rescue Plan: Existence of a documented “High-Angle Rescue” protocol.

These steps help insurers:

- classify exposure more accurately

- reduce uncertainty

- prevent claim disputes

- evaluate eligibility fairly

Honest disclosure is especially important because catastrophic fall claims often trigger deeper occupational investigations.

Common Failure Paths in Height-Restricted Insurance Policies

Coverage problems commonly occur when:

- Elevated duties are inaccurately disclosed

- subcontract climbing work is omitted

- offshore elevated assignments are hidden

- actual working heights exceed disclosed thresholds

- OSHA fall violations reveal unsafe operational history

- catastrophic claims trigger occupational reclassification reviews

These situations often increase the likelihood of:

- claim disputes

- exclusion enforcement

- benefit limitations

- policy rescission investigations

- stricter future underwriting

Frequently Asked Questions

At what exact height do insurance restrictions typically begin?

While it varies by carrier, many insurers trigger stricter underwriting or automatic occupational referrals starting at around 15 feet. Major policy exclusions, premium increases, or coverage limitations often appear once work regularly exceeds 50 to 100 feet, especially for tower climbing, bridge work, and structural ironwork.

Can I get disability insurance if I am a full-time tower climber?

Yes, but coverage is often restricted. Disability insurers may apply lower monthly benefit caps, stricter underwriting classifications, or exclusion riders that limit coverage for work-related fall injuries. Some policies may still cover non-work accidents while excluding elevated occupational injuries.

Does my policy cover side work like weekend roofing?

Usually not unless the work was fully disclosed during underwriting. Most occupational insurance policies are based on your primary reported duties. Undisclosed roofing, scaffold work, subcontract climbing, or elevated side jobs are common causes of claim disputes, denied claims, and policy rescission investigations.

Will an OSHA violation automatically cancel my insurance?

A single OSHA violation rarely causes immediate cancellation, but it can lead to higher renewal premiums, stricter underwriting reviews, or reduced carrier availability. Insurers often view repeated fall-protection violations as indicators of elevated future catastrophic claim exposure.

Is there a standard height limit on a standard Public Liability policy?

Yes. A typical standard business or public liability policy frequently includes a built-in height restriction of either 10 meters (approximately 30 feet) or 15 meters (approximately 50 feet). Working beyond these limits often requires a specialized elevated-risk endorsement, contractor extension, or separate high-risk liability policy.

Final underwriting insight:

Height restrictions do not exist simply because elevated work is dangerous. They exist because elevated-risk occupations create catastrophic exposure scenarios that are difficult for insurers to price once rescue difficulty, permanent disability probability, and occupational severity combine.

Key Takeaways

- Insurers use height restrictions because severely elevated falls can create catastrophic disability and liability claims.

- Higher elevation exposure usually leads to stricter underwriting and policy limitations.

- Tower climbing, offshore elevated work, and structural steel work often receive the toughest restrictions.

- Disability insurers closely evaluate whether a worker could permanently lose the ability to perform elevated duties.

- Undisclosed side work, subcontract climbing, or inaccurate job descriptions can create major claim disputes.

- OSHA violations, poor safety history, and rescue difficulties can increase underwriting concern.

- Height restrictions vary significantly between occupations, depending on the potential for catastrophic injury severity.

- Accurate occupational disclosure helps reduce underwriting problems and future coverage disputes.

- Height restrictions in occupational insurance policies are designed to control catastrophic fall-risk exposure.

Institutional & Underwriting Reference

This article was developed using publicly available occupational safety guidance, underwriting classification frameworks, elevated-risk liability standards, catastrophic injury modeling principles, and high-risk occupational insurance practices commonly referenced across the insurance and construction-risk industries.

Institutional & Regulatory References

- Occupational Safety and Health Administration (OSHA) Fall Protection Standards — Federal fall-protection requirements used by insurers to evaluate elevated-work operational controls and claims exposure.

- National Institute for Occupational Safety and Health (NIOSH) Fall Prevention Research — Occupational fall-injury research is frequently referenced when evaluating catastrophic injury severity and elevated-work exposure trends.

- Legal & General Occupational Underwriting Limits — Example occupational underwriting framework illustrating how insurers evaluate height exposure, hazardous duties, and occupational classification severity.

- International Labour Organization (ILO) Occupational Safety Guidance — International workplace safety guidance relevant to elevated-work operations and fall-risk management systems.

- Health and Safety Executive (HSE) Working at Height Guidance — Regulatory guidance commonly referenced in elevated-work operational risk evaluation and contractor safety review frameworks.

Reviewed for Underwriting Accuracy By

RJI Institutional Review Team

This article was reviewed for underwriting accuracy involving:

- elevated-risk occupational classification analysis

- catastrophic fall severity modeling

- rescue-complexity evaluation

- disability-income exposure assessment

- occupational disclosure failure-path analysis

- underwriting threshold interpretation

- specialty elevated-risk policy structures

- high-risk contractor liability exposure

- operational risk-control evaluation

Research & Underwriting Methodology

This article applies an underwriting-translation framework designed to explain how insurers structurally evaluate elevated occupations involving catastrophic fall exposure.

The analysis incorporates:

- occupational classification systems

- catastrophic injury severity modeling

- underwriting threshold escalation logic

- elevated-risk policy restrictions

- rescue-difficulty exposure analysis

- disability-income replacement risk

- specialty contractor liability structures

- OSHA and fall-protection compliance interpretation

- operational underwriting controls

- occupational misclassification and claim-failure pathways

The article also translates institutional underwriting concepts into worker-understandable operational consequences while maintaining carrier-oriented severity logic and policy-structure realism.

Published: May 2026

Last reviewed: June, 2026.