Executive Summary

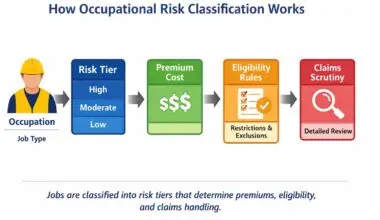

Why job title determines insurance approval is rooted in how insurers classify occupational risk, which directly affects eligibility, pricing, and claim outcomes. Insurers use it to classify risk exposure, determine eligibility, set pricing, and apply exclusions. Occupational risk classification frameworks, similar to those used in workplace safety systems such as OSHA, translate job roles into measurable exposure categories that directly influence underwriting decisions. Insurers use job titles as a primary risk classification input, meaning approval decisions, pricing structures, and claim evaluations are directly influenced by how an occupation is categorized within underwriting systems.

Key underwriting definition:

Job title determines insurance approval because it serves as a primary input in occupational risk classification systems, which insurers use to evaluate eligibility, pricing, and claim exposure.

What Does “Job Title” Mean in Insurance Underwriting?

In insurance underwriting, a job title is not just a label, it is a risk classification signal.

Insurers distinguish between:

- Declared job title → What you write on the application

- Actual job duties → What you actually do daily

This distinction matters because underwriting systems rely on standardized occupational classification databases, where each job title is mapped to a predefined risk level.

For example:

- “Engineer” → could be low-risk (office-based)

- “Field Engineer” → moderate to high risk

- “Offshore Engineer” → high or extreme risk

The same title can lead to different outcomes depending on how it is interpreted and verified.

How Insurers Classify Job Titles Into Risk Categories

Insurers convert job titles into risk classes, not descriptions.

Core Classification Layers:

1. Physical Hazard Exposure

- Working at heights

- Heavy machinery

- Explosives or high-impact tools

2. Environmental Risk

- Offshore conditions

- Extreme temperatures

- Chemical exposure

3. Operational Risk

- Transportation (aviation, maritime)

- Confined spaces

- High-pressure systems

This classification approach mirrors occupational risk segmentation used in labor statistics reporting, where job categories are grouped based on exposure levels, injury rates, and operational hazards.

This explains why job title determines insurance approval, as classification directly feeds into underwriting decision models.

Risk Tier Mapping

| Risk Tier | Example Jobs | Underwriting Impact |

|---|---|---|

| Low | Office administrator | Standard approval |

| Moderate | Warehouse supervisor | Slight premium increase |

| High | Construction worker | Coverage limits + exclusions |

| Extreme | Offshore diver | Possible decline |

Once mapped, your job title becomes a fixed input in underwriting logic.

How Job Title Drives the Underwriting System

Insurance underwriting follows a structured decision system:

Step-by-Step Process

- Job title submitted

- Mapped to classification database

- Cross-referenced with:

- Industry

- Duties

- Work environment

- Risk score assigned

- Eligibility band determined

- Decision triggered:

- Approve

- Modify

- Decline

This classification-driven decision process follows the broader framework outlined in How Insurance Underwriting Works for High-Risk Jobs, where insurers combine occupational data, verification systems, and financial exposure models to determine approval outcomes.

Key Insight

Underwriters do not evaluate your job manually; they rely on predefined classification logic.

How Insurers Verify Job Titles During Underwriting

After a job title is submitted and classified, insurers perform verification checks to confirm that the declared occupation accurately reflects actual work duties. This step reduces misclassification risk and prevents incorrect underwriting decisions.

Verification Methods Used by Insurers

1. Employer Verification

Insurers may confirm job roles directly with employers to validate responsibilities, work environment, and exposure levels.

2. Third-Party Data Sources

External databases and background verification systems are used to cross-check employment details and occupational history.

3. Industry Classification Cross-Checks

Job titles are compared against standardized occupational classification systems to ensure consistency with known risk categories.

4. Fraud Detection Triggers

Applications flagged for inconsistencies—such as vague job titles or mismatched duties—may undergo additional scrutiny or escalation.

Why Verification Matters

Verification ensures that underwriting decisions are based on actual occupational risk, not just declared information. When discrepancies are identified, insurers may:

- Adjust risk classification

- Apply stricter underwriting conditions

- Request additional documentation

- Decline coverage

Critical Insight

Job title verification is a key reason why job title determines insurance approval, as underwriting outcomes depend not only on classification, but on the accuracy and consistency of occupational data.

Underwriting Filters Triggered by Job Title

Once classified, your job title activates specific underwriting filters:

1. Coverage Limits

- High-risk jobs → lower maximum coverage

- Extreme-risk jobs → capped or restricted policies

2. Policy Type Restrictions

- Standard policies may be unavailable

- Shift toward:

- Simplified issue

- Guaranteed issue

3. Rider Eligibility

- Disability riders may be denied

- Accidental riders may be restricted

- Risk class directly increases pricing

- Higher uncertainty = higher premiums

These restrictions align with formal eligibility thresholds explained in Eligibility Requirements for High-Risk Job Insurance, where occupation type directly determines qualification boundaries and acceptable risk levels.

Decision Breakpoints: When Approval Changes

This is where underwriting becomes critical.

Approval shifts when risk crosses thresholds such as:

- High-risk job + high coverage request

- Hazard exposure exceeding insurer tolerance

- Job title inconsistent with declared duties

- Data mismatch across verification systems

When these thresholds are exceeded, insurers often transition applicants into full underwriting pathways that include medical verification, as detailed in Medical Exams for High-Risk Job Insurance.

Combined risk trigger point:

Approval typically shifts when multiple risk variables intersect, such as:

– High-risk job classification + high coverage request

– Verified hazardous duties + inconsistent application disclosure

– Elevated occupational risk + simplified underwriting limits

At this point, insurers either:

– Escalate to full underwriting, or

– Restrict or decline coverage

Decision Outcomes

| Condition | Outcome |

|---|---|

| Within risk threshold | Standard approval |

| Near threshold | Modified approval |

| Exceeds threshold | Decline or alternative policy |

Critical Insight

Approval is not binary; it shifts based on combined risk factors, with job title as a primary driver.

Underwriting Translation: What This Means for You

The underwriting system creates real-world differences:

Example 1:

- “Software Engineer” → Approved quickly, lower premium

- “Oil Rig Engineer” → Restricted approval, higher premium

Example 2:

- “Supervisor” vs “Site Supervisor”

→ Same title category, different exposure → different outcomes

In practice, underwriting decisions frequently diverge for applicants with similar qualifications but different job titles, as insurers prioritize exposure risk over professional designation.

Why This Happens

- Insurers price risk exposure, not job prestige

- Titles act as shortcuts to risk prediction

Cost Drivers and Tradeoffs

This pricing structure reflects the broader underwriting framework used across high-risk job insurance, where occupational classification directly influences financial risk modeling.

Your job title directly affects:

- Higher risk → higher cost

- Greater uncertainty → additional loading

Reinsurance and industry risk reports from Swiss Re Institute consistently show that higher occupational risk profiles lead to increased pricing, tighter coverage limits, and stricter underwriting controls across life and disability products.

2. Coverage Availability

- Limited options for high-risk occupations

- Reduced flexibility in policy structure

3. Tradeoff Structure

| Advantage | Tradeoff |

|---|---|

| Faster approval | Lower reliability |

| Easier access | Higher cost |

| Simplified underwriting | More exclusions |

These tradeoffs become more pronounced in simplified underwriting structures, as explained in Non-Medical Insurance for High-Risk Jobs: Tradeoffs Explained, where reduced screening increases both accessibility and claim uncertainty.

Key Insight

Job title influences not just approval but the quality and reliability of coverage.

Structural Exclusions Based on Job Title

Insurers use exclusions to manage unquantifiable risks.

Common Exclusion Types:

- Activity-based exclusions (e.g., offshore operations)

- Environment-specific exclusions (e.g., underwater work)

- Hazard-specific exclusions (e.g., explosives handling)

These exclusions are applied based on the same occupational classification and verification system used during underwriting, ensuring that unquantifiable risks are isolated at both policy and claim stages.

Structural Model

Exclusions isolate risks that cannot be accurately priced without deeper verification.

Failure Path Analysis: What Breaks Approval or Claims

Major Failure Points:

- Misclassified job title

- Undisclosed hazardous duties

- Generic or vague job descriptions

- Mismatch between application and verification data

- Change in job role after policy issuance

High-Risk Scenario

- Declared: “Technician”

- Actual: Offshore maintenance worker

This creates a classification mismatch, increasing claim denial risk.

Claim Breakpoints: Where Job Title Causes Denial

Claims are not based on what you declared; they are based on verified reality.

At Claim Stage, Insurers:

- Reassess your job role

- Verify duties at time of incident

- Compare with original application

Claim Denial Triggers:

- Undisclosed occupational hazards

- Misrepresentation of job duties

- Activity outside declared role

This is another reason why job title determines insurance approval outcomes, especially when claims are reassessed against actual job duties.

Critical Insight

Job title errors often do not surface at approval; they surface at claim stage.

Evidence Block: Why Job Titles Matter Systemically

Occupational risk classification systems used across safety and insurance industries consistently show:

- Higher-risk occupations → higher incident probability

- Increased uncertainty → stricter underwriting controls

- Simplified underwriting → higher premiums + lower limits

Occupational injury and exposure data tracked by agencies such as the National Institute for Occupational Safety and Health (NIOSH) consistently show that higher-risk job categories carry significantly elevated incident probabilities, which directly informs insurance risk classification models.

Industry Pattern

- High-risk job titles are:

- More expensive to insure

- More restricted in coverage

- More likely to face claim scrutiny

These patterns directly influence underwriting models, where higher-risk occupations are systematically assigned stricter approval conditions, higher premiums, and more coverage limitations.

Real-World Scenarios

Scenario 1: Offshore Worker vs Office Engineer

- Same qualification

- Different job titles

→ Offshore worker faces higher premiums and exclusions

Scenario 2: Construction Supervisor vs Laborer

- Supervisor → moderate risk

- Laborer → high risk

→ Different approval outcomes

Scenario 3: Pilot vs Aviation Technician

- Pilot → extreme risk classification

- Technician → moderate risk

→ Major differences in coverage availability

Job title is the entry point into the entire underwriting system.

These underwriting outcomes form part of the broader system explained in Risk Job Insurance, where occupational risk classification, underwriting filters, and claim validation mechanisms operate together.

Frequently Asked Questions About Job Title and Insurance Approval

Does your job title affect insurance approval?

Yes. Your job title is a primary input in underwriting and directly affects insurance approval. Insurers use it to classify occupational risk, which determines eligibility, coverage limits, premium pricing, and policy restrictions. Higher-risk job titles typically result in stricter approval conditions or modified coverage.

Why do insurers classify jobs into risk categories?

Insurers classify jobs into risk categories to standardize how occupational hazards are evaluated. Different jobs carry different levels of physical, environmental, and operational risk, and classification systems allow insurers to assign risk scores, predict claim probability, and apply consistent underwriting rules across applicants.

Can a wrong job title cause claim denial?

Yes. An incorrect or misleading job title can lead to claim denial, especially if the actual job duties differ from what was declared during application. At claim stage, insurers verify occupational details, and any mismatch between declared and actual work can be treated as misrepresentation.

What jobs are considered high risk for insurance?

High-risk jobs typically include occupations with elevated exposure to physical danger or hazardous environments. Examples include construction workers, offshore oil and gas workers, pilots, miners, and heavy equipment operators. These roles often face higher premiums, stricter underwriting, and more exclusions.

Core underwriting principle:

Job title is not evaluated for what it represents socially, but for the level of measurable risk exposure it introduces into the insurance system.

Key Takeaways

- Job title is a core underwriting input, not just a description

- It determines:

- Approval

- Pricing

- Coverage limits

- Exclusions

- Misclassification creates major claim risk

- High-risk job titles face structural limitations

- Verification at claim stage can override initial approval

System-level insight:

Insurance approval is not determined by job title alone, but by how that title maps to measurable risk exposure within underwriting classification systems.

Final Underwriting Insight

Job titles do not simply describe what you do; they define how insurers classify, price, and accept risk. In high-risk insurance, your job title shapes the entire lifecycle of your policy, from approval conditions to claim outcomes.