Table of Contents Hide

- 1. Introduction

- 2. Offshore Work Is Fundamentally Different From Onshore Jobs

- 3. Why Traditional Life Insurance Often Fails Offshore Workers

- 4. Unique Risks Offshore Workers Face Daily

- 5. What Makes Offshore Workers’ Life Insurance “Specialized”

- 6. The Financial Impact on Families Without Proper Coverage

- 7. Employer-Provided Coverage Is Rarely Enough

- 8. How Specialized Life Insurance Protects Offshore Workers Better

- 9. Role of Accidental Death & Dismemberment (AD&D) Offshore

- 10. Cost vs Risk: Why “Cheaper” Insurance Can Be More Expensive

- 11. Who Needs Specialized Offshore Life Insurance the Most

- 12. Common Myths That Stop Offshore Workers From Getting Proper Coverage

- 13. How This Fits Into Offshore Workers’ Life Insurance Planning

- 14. Conclusion

1. Introduction

At 4:30 a.m., the helicopter blades start spinning on a dimly lit offshore helipad. The weather is unsettled, the sea below is restless, and the platform sits hours away from the nearest coastline. For the crew boarding that flight, this is a routine morning. Offshore work rarely feels dramatic when you’re living it day after day. Yet the reality is simple: offshore jobs operate in environments where risk is built into every shift.

Offshore oil and gas workers, commercial fishermen, marine engineers, divers, and vessel crews work far from immediate help, surrounded by heavy machinery, volatile conditions, and unforgiving weather. The job pays well for a reason. But when it comes to financial protection, many offshore workers assume a standard life insurance policy will suffice.

That assumption is where problems begin because offshore roles demand insurance coverage that reflects real-world offshore risk, not generic onshore job profiles.

Those risks are part of the broader insurance for oil and gas workers system, which explains how offshore and industrial jobs are treated across different insurance policies.

Offshore work is not just another occupation category on an insurance form. It carries unique risks that traditional life insurance often excludes, restricts, or prices aggressively. This is why offshore workers’ need specialized life insurance exists and why relying on a standard policy can leave dangerous gaps.

This article explains, in practical terms, why offshore workers need specialized life insurance, how offshore risks differ from onshore jobs, and what happens when coverage doesn’t match reality. For a full overview of how offshore life insurance is structured, see our life insurance for offshore workers guide.

2. Offshore Work Is Fundamentally Different From Onshore Jobs

Onshore jobs, even those labeled “industrial,” operate within reach of infrastructure. Roads, hospitals, fire services, and emergency responders are all within minutes. Offshore jobs operate in a completely different risk universe.

Remote and Isolated Locations

Offshore installations are often hundreds of miles from land. If something goes wrong, help doesn’t arrive quickly. Medical evacuations depend on weather, aircraft availability, and sea conditions. A minor incident onshore can become a life-threatening situation offshore simply because of distance.

Harsh and Unpredictable Weather

Wind, waves, storms, and sudden weather shifts are constant variables offshore. Even experienced crews can be caught off guard by rapidly escalating conditions that affect visibility, equipment stability, and transportation safety.

Heavy Machinery and Complex Operations

Offshore platforms and vessels operate in proximity to high-pressure systems, cranes, drilling equipment, winches, and rotating machinery. The margin for error is small, and mechanical failures can have serious consequences.

Limited Emergency Response

Onshore, emergency services scale quickly. Offshore, the crew is the first responder. Fire suppression, rescue, and medical care rely on onboard training and equipment until evacuation becomes possible.

Transportation Risks

Getting to and from offshore jobs involves helicopters, crew boats, supply vessels, and sometimes diving bells or submersibles. Transportation alone adds layers of exposure not found in typical onshore employment.

These differences matter deeply to insurers, and they are precisely why offshore workers are treated differently in underwriting.

3. Why Traditional Life Insurance Often Fails Offshore Workers

Many offshore workers buy life insurance early in their careers, often before fully understanding how their occupation affects coverage. Others purchase policies quickly, assuming “life insurance is life insurance.” Unfortunately, traditional policies frequently fall short. This gap in protection explains why offshore workers need specialized life insurance rather than relying on standard policies.

Occupational Exclusions

Standard life insurance policies often include exclusions for hazardous occupations. Offshore drilling, diving, and commercial fishing are commonly flagged. Claims related to these activities may be limited or denied outright.

These exclusions come from the same risk-classification framework explained in risk job insurance, which shows how insurers group dangerous occupations before applying any coverage.

High-Risk Classifications

Even when coverage is approved, offshore workers are often placed into high-risk categories. This can lead to:

-

Significantly higher premiums

-

Lower coverage limits

-

Stricter underwriting conditions

Some applicants are declined entirely once their offshore role is fully disclosed.

Policy Denial After Disclosure

A typical scenario: a worker buys a policy without clearly explaining offshore duties. Later, during a claim, the insurer reviews occupational details and disputes coverage. What looked like protection on paper becomes a legal argument during the worst possible time.

Hidden Clauses Many Workers Overlook

Standard policies are not written with offshore realities in mind. Clauses related to location, travel, and hazardous activity may quietly restrict coverage in offshore environments.

This is not a flaw in insurance, it’s a mismatch. Traditional policies are built for predictable, onshore risk profiles.

4. Unique Risks Offshore Workers Face Daily

Offshore risks are not abstract. They are part of daily operations, and insurers who specialize in this field understand how often small hazards compound into serious incidents. Understanding why offshore workers need specialized life insurance starts with recognizing how insurers view offshore risk.

Mechanical and Equipment Risks

Cranes lifting heavy loads, rotating drill strings, tensioned cables, and pressurized systems are constantly in motion. Equipment failure or human error can result in crushing injuries, entanglement, or falls.

Environmental and Weather Risks

High winds can destabilize equipment. Waves can slam vessels against structures. Lightning strikes, storms, and rogue waves create constant exposure even during routine tasks.

Transportation Risks

Helicopter transfers and crew boat operations are among the most statistically significant offshore risks. Mechanical failure, visibility issues, or sudden weather shifts can escalate quickly.

Diving-Specific Risks

Offshore divers face decompression illness, equipment malfunction, entanglement, and underwater visibility hazards. These risks are highly specialized and often excluded from standard policies.

Explosion and Fire Risks

Hydrocarbons, gas pockets, and electrical systems create fire and explosion hazards unique to offshore energy operations. When incidents occur, they escalate rapidly due to confined spaces.

Fatigue and Long-Shift Risks

Extended rotations, night shifts, and physically demanding work increase fatigue-related errors. Offshore accidents often stem from exhaustion rather than recklessness.

Each of these risks underscores the need for offshore workers to have coverage explicitly tailored to their environment.

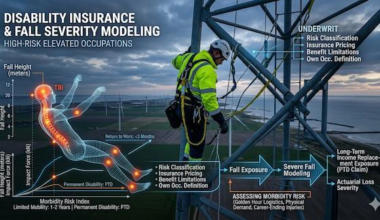

5. What Makes Offshore Workers’ Life Insurance “Specialized”

Specialized Offshore Workers Life Insurance is not just standard coverage with a higher price tag. It is structured from the ground up to reflect offshore realities.

Risk-Rated Underwriting

Underwriting considers the actual offshore role, not just a job title. Divers, drillers, technicians, and marine crew are assessed differently, ensuring coverage aligns with exposure.

Offshore-Specific Coverage Clauses

Policies are written to explicitly include offshore duties, locations, and transportation methods, reducing ambiguity at claim time.

AD&D Enhancements

Many specialized policies integrate or easily add accidental death and dismemberment benefits, recognizing the higher likelihood of serious injury offshore.

Job-Specific Eligibility Criteria

Rather than blanket exclusions, eligibility is tailored. This allows many offshore workers who have been declined elsewhere to secure meaningful coverage.

The specialization isn’t about fear, it’s about accuracy.

6. The Financial Impact on Families Without Proper Coverage

When an offshore worker is underinsured, the consequences extend far beyond immediate loss.

Sudden Income Loss

Offshore roles often support entire households. Without adequate life insurance for offshore workers, families may struggle to replace lost income.

Debt Exposure

Mortgages, education costs, personal loans, and business obligations don’t disappear. Inadequate coverage can leave families carrying long-term debt.

Funeral and Emergency Costs

Offshore-related fatalities can involve international transport, specialized recovery, and higher logistical expenses.

Long-Term Stability

Life insurance isn’t about short-term relief. It’s about ensuring dependents have financial breathing room to make decisions without panic.

Proper coverage is a stabilizing force during instability.

7. Employer-Provided Coverage Is Rarely Enough

Many offshore workers rely heavily on employer-provided insurance, assuming it’s sufficient. In reality, it often falls short. This limitation is another reason why offshore workers need specialized life insurance that remains active regardless of employer or contract. Employer benefits alone rarely address why offshore-specific coverage matters for long-term family protection.

Coverage Limits

Employer policies typically offer limited death benefits, often based on salary multiples that don’t reflect offshore risk exposure.

Lack of Portability

When contracts end or jobs change, coverage often disappears. Offshore careers are fluid, and insurance gaps are common.

Contract-Based Employment

Many offshore workers operate on rotational or project-based contracts. Employer coverage may not extend between assignments.

This is why the distinction between employer-provided vs individual offshore insurance matters. Individual policies travel with the worker, not the job.

8. How Specialized Life Insurance Protects Offshore Workers Better

Specialized policies address the gaps left by standard coverage.

Broader Death Benefit Triggers

Coverage extends to offshore-specific incidents, including transportation accidents and worksite emergencies.

Offshore Accident Coverage

Accidents occurring during offshore duties are clearly included, reducing claim disputes.

On-Duty and Off-Duty Protection

Many policies cover workers during rotations, transfers, and rest periods linked to offshore deployment.

Optional Riders

Common enhancements include:

-

Accidental death & dismemberment

-

Disability income riders

-

Medical evacuation support

Together, these features form comprehensive offshore job risk protection.

9. Role of Accidental Death & Dismemberment (AD&D) Offshore

Offshore environments have a higher probability of severe injury, not just fatal incidents. This is where accidental death & dismemberment for offshore workers plays a critical role. The role of AD&D further reinforces why offshore workers need specialized life insurance, especially in environments where severe injury is more likely than instant fatality.

Why AD&D Is Critical Offshore

Serious injuries can permanently affect earning ability. AD&D provides lump-sum payouts for qualifying injuries, not just death.

Common Qualifying Offshore Incidents

-

Machinery-related amputations

-

Falls from height

-

Diving accidents

-

Transportation-related trauma

How It Complements Life Insurance

AD&D does not replace life insurance, it strengthens it by addressing financial needs related to injuries.

10. Cost vs Risk: Why “Cheaper” Insurance Can Be More Expensive

Offshore workers are often cost-conscious, especially early in their careers. But cheaper policies can create expensive problems later. When claims are denied, the financial consequences highlight the case for offshore-specific life insurance despite higher premiums. This is often the point where workers truly understand why offshore workers need specialized life insurance instead of cheaper alternatives.

False Savings of Basic Policies

Low premiums often reflect exclusions and limitations that surface only at claim time.

Risk of Denied Claims

A denied claim costs more than years of higher premiums ever would.

Justifying the Cost

The cost of offshore workers’ life insurance reflects a realistic risk assessment. Proper coverage is not overpriced, it’s appropriately priced.

The real question isn’t cost. It’s whether the policy will pay when needed.

11. Who Needs Specialized Offshore Life Insurance the Most

While all offshore workers face elevated risk, exposure varies by role. Each of these professions illustrates why offshore workers need specialized life insurance tailored to actual job exposure.

Oil & Gas Workers

Exposure to hydrocarbons, pressure systems, and complex operations.

Offshore Drillers

High mechanical risk, rotating equipment, and long shifts.

Commercial Fishermen

Weather exposure, vessel instability, and manual handling risks.

Offshore Divers

Unique physiological and equipment-related hazards.

Marine Engineers

Maintenance of critical systems under operational pressure.

Offshore Construction Workers

Heavy lifting, height exposure, and dynamic work environments.

Seafarers and Vessel Crew

Extended time at sea, transportation risks, and isolation.

According to the IMO, maritime occupational hazards are significantly amplified by fatigue, isolation, and weather exposure.

Each group benefits from coverage for offshore employees designed for their specific exposure.

12. Common Myths That Stop Offshore Workers From Getting Proper Coverage

“My Employer Covers Everything”

Employer policies are limited, temporary, and not tailored to individual needs.

“Offshore Accidents Are Rare”

They are less frequent than daily hazards but far more severe when they occur.

“Specialized Insurance Is Unaffordable”

In reality, many policies are competitively priced once risk is accurately assessed.

These myths delay protection, not risk.

13. How This Fits Into Offshore Workers’ Life Insurance Planning

Understanding why specialized coverage matters is the foundation for more intelligent decisions. This connects directly to:

-

Choosing the right policy type

-

Comparing offshore-specific coverage options

-

Evaluating real costs versus perceived savings

-

Preparing families for claim readiness

Understanding risk is only one step in Offshore Workers Life Insurance planning, which also involves comparing policy structures and coverage limits.

Education leads to better protection, not just better policies.

Life insurance is only one part of how offshore risk is insured. Workers’ compensation, disability, and liability coverage are explained in our full insurance for oil and gas workers guide.

14. Conclusion

Offshore work will always carry risk. No amount of training or experience eliminates the realities of distance, machinery, weather, and transportation. What offshore workers can control is how well their families are protected if something goes wrong. Ultimately, this is why offshore workers need specialized life insurance, not as a luxury, but as a practical necessity.

Standard life insurance was never designed for offshore environments. Specialized Offshore Workers Life Insurance exists because offshore work is different and pretending otherwise creates unnecessary vulnerability. Once the risks are clearly understood, offshore workers’ specialized life insurance becomes self-evident.

Choosing the right coverage isn’t about fear. It’s about preparation, responsibility, and understanding the fundamental nature of offshore life. When insurance matches the job, protection becomes reliable and that peace of mind is something every offshore worker deserves.

Celestine Nwulu

Celestine Nwulu is a publisher and researcher focused on high-risk insurance, commercial coverage, and occupational risk industries. His work translates complex underwriting concepts, insurance requirements, claims risks, and coverage structures into practical guidance for workers, contractors, and business owners operating in hazardous industries.