Executive Summary

Life insurance for high-risk workers is governed by occupational classification systems and underwriting adjustments rather than standard pricing models. According to International Labour Organization (ILO) data, hazardous occupations carry higher fatality risk, leading insurers to apply premium loadings, exclusions, and eligibility restrictions. Coverage outcomes depend on job duties, disclosure accuracy, and policy design.

Evidence Base

This article draws from:

– International Labour Organization (ILO) occupational fatality and workplace risk data

– National Institute for Occupational Safety and Health (NIOSH) research on hazardous work exposure

– National Association of Insurance Commissioners (NAIC) underwriting and insurance market guidance

– Industry underwriting practices related to occupational classification, mortality assessment, exclusions, and premium loadings

These sources help explain why life insurance for hazardous occupations often involves stricter underwriting, occupational exclusions, higher premiums, and reduced eligibility limits compared to standard-risk applicants.

Introduction: Why Life Insurance Works Differently in Dangerous Jobs

Life insurance is often presented as straightforward financial protection: premiums are paid over time, and beneficiaries receive a payout if the insured person dies during the policy period.

For workers in hazardous occupations, however, life insurance underwriting is rarely straightforward. Construction workers, offshore personnel, miners, industrial operators, transport workers, and others in dangerous environments are often evaluated under separate occupational risk frameworks that affect pricing, exclusions, eligibility, and claim structure.

These differences are not accidental, and they are not based on job titles alone. They exist because life insurance is built around long-term risk, and dangerous work changes how that risk is evaluated.

This guide explains how life insurance works for high-risk workers, why coverage rules differ, and what job-related factors insurers focus on. It is part of our broader explanation of insurance rules for high-risk jobs, and is written for workers with little or no insurance background.

What Life Insurance Is Designed to Do

At its core, life insurance is designed to protect people who depend on your income.

If you die during the policy period, the insurer pays a lump sum to your beneficiaries. That money is typically used to replace lost income, cover debts, or support family members.

To make this system work, insurers estimate:

-

How long a person is likely to live

-

How likely a payout is during the policy period

-

How large that payout might be

Age, health, and lifestyle all matter. But for high-risk workers, occupation plays a much larger role than many people expect.

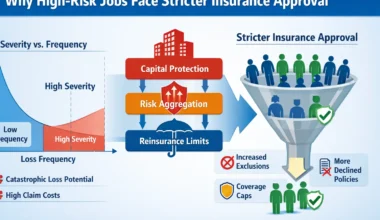

Why High-Risk Jobs Change Life Insurance Rules

Data from the International Labour Organization (ILO) shows that hazardous occupations experience higher fatality and injury rates, which helps explain why life insurance rules change for high-risk work.

Life insurance pricing and eligibility are based on probability over time.

When a job increases the likelihood of fatal accidents or long-term health damage, insurers must account for that additional risk. This does not mean high-risk workers cannot get life insurance. It means the rules used for average-risk work no longer apply cleanly.

This assessment is not moral or judgmental. It is actuarial, based on historical injury rates, fatality data, occupational exposure patterns, and claims experience.

High-risk jobs often involve:

-

Greater exposure to fatal accidents

-

Remote or unpredictable environments

-

Heavy machinery or hazardous materials

-

Long shifts and physical strain

-

Travel risks, including offshore or cross-border work

From an insurer’s perspective, these factors increase uncertainty. As uncertainty increases, insurers adjust how coverage is offered.

Dangerous work changes insurance behavior because higher risk requires special rules. These underwriting adjustments are part of the broader insurance framework explained in Types of Insurance for High-Risk Jobs, where different forms of occupational coverage respond to workplace risk in different ways.

Job Duties Matter More Than Job Titles

One of the most common misunderstandings around life insurance is assuming that job titles determine eligibility.

In reality, insurers focus on what you actually do, not what your role is called.

Two people may both be labeled “technicians” or “supervisors,” but if one regularly works at height, handles heavy equipment, or operates in remote locations, their risk profile is very different.

When applying for life insurance, insurers typically examine:

-

Daily work activities

-

Frequency of hazardous tasks

-

Work environment (onshore, offshore, industrial, remote)

-

Use of machinery or tools

-

Travel requirements related to work

This is why life insurance outcomes can differ widely even among workers with similar titles.

Occupational Classification in Life Insurance

Life insurers convert job duties into risk classes that directly affect pricing and eligibility.

Typical classification adjustments include:

- Standard class → office-based or low-risk roles

- Moderate risk → field work with limited hazard exposure

- High risk → construction, offshore, mining, heavy equipment operation

Insurers may apply:

- Flat extra fees (additional cost per $1,000 of coverage)

- Table ratings (percentage increase in base premium)

- Occupational exclusions for specific activities

Classification determines whether coverage is issued, priced higher, or restricted.

In practice, occupational classification systems function as actuarial control mechanisms that allow insurers to segment mortality exposure across different categories of hazardous work.

This classification framework connects directly to occupational class rating systems, where insurers translate workplace exposure into pricing, eligibility, and underwriting decisions. We explain this process further in Occupational Class Ratings: How Insurers Price High-Risk Jobs.

How Life Insurance Applications Are Evaluated for High-Risk Work

Life insurance underwriting for high-risk workers is usually more detailed.

In addition to medical information, insurers may ask:

-

Detailed descriptions of job duties

-

Time spent on hazardous tasks

-

Work location and environment

-

Safety protocols followed

-

History of work-related injuries

This information helps insurers estimate how occupational risk interacts with age and health over time.

The process may feel intrusive or slow, but it is driven by risk assessment rather than judgment about the worker.

Once occupational risk is factored in, these differences often appear in specific, predictable ways.

Underwriting Filters for High-Risk Occupations

Life insurance underwriting for hazardous jobs combines medical and occupational risk assessment.

Key filters include:

- Medical condition and history

- Age and lifestyle factors

- Occupational hazard exposure

- Work environment (remote, offshore, industrial)

- Frequency of dangerous tasks

High-risk workers are evaluated not only on health but on how often they are exposed to potentially fatal events.

Underwriting Decision Thresholds

How Occupational Exposure Changes Underwriting Outcomes

| Occupational Exposure Factor | Typical Underwriting Impact |

|---|---|

| Routine work at height | Higher premium classification or exclusion risk |

| Offshore or remote deployment | Additional scrutiny due to evacuation and emergency-response limitations |

| Heavy machinery operation | Increased occupational risk classification |

| Frequent hazardous environment exposure | Greater likelihood of premium loadings |

| Cross-border or international assignments | Geographic limitations or coverage restrictions |

| Combined medical and occupational risk | Possible movement into stricter underwriting categories |

| High coverage requests in hazardous occupations | Reduced eligibility limits or additional underwriting review |

Occupational underwriting decisions are rarely based on a single factor alone. Insurers typically evaluate combined exposure patterns, claim probability, emergency access, and long-term mortality assumptions together.

Common Ways Life Insurance Differs for High-Risk Workers

High-risk workers often encounter one or more of the following differences:

Higher premiums

Coverage may cost more because the probability of payout is higher.

Occupational exclusions

Some policies exclude death caused by specific job-related activities.

Coverage limits

The maximum payout may be lower than expected.

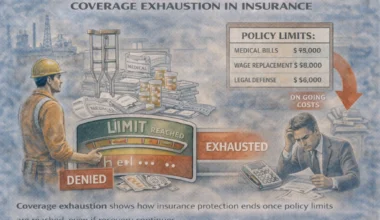

Coverage restrictions are also heavily influenced by internal policy limits, which insurers use to control financial exposure in hazardous occupations. We explain this system in Policy Limits in High-Risk Insurance: Why They Exist and How Insurers Set Them.

Restricted policy types

Certain forms of life insurance may be unavailable for specific jobs.

Additional documentation

Applications and claims may require more verification.

These differences vary by insurer and job type, but they reflect how occupational risk is managed.

Coverage outcomes are also shaped by how insurers structure eligibility tiers, exclusions, and underwriting conditions for hazardous work environments. We explain this framework further in How Insurers Structure Coverage for Hazardous Occupations.

Offshore and Remote Work Considerations

Workers in offshore, maritime, or remote environments often face additional scrutiny.

Life insurance for offshore work may involve:

-

Exclusions related to transport accidents

-

Restrictions based on distance from medical care

-

Higher premiums due to evacuation and rescue risks

These rules exist because fatal incidents in remote settings are more difficult to prevent or respond to quickly.

Understanding this helps explain why offshore life insurance is often treated separately from standard coverage.

Real-World Examples Across High-Risk Jobs

Construction Worker at Height

Offshore Oil and Gas Worker

Mining and Underground Work

Commercial Transport and Industrial Work

Employer-Provided Life Insurance vs Personal Policies

Many high-risk workers receive some life insurance through their employer. While helpful, employer coverage has limitations.

Employer-provided life insurance:

-

Is usually tied to employment

-

Often has lower coverage amounts

-

May not fully reflect job-specific risk

-

Ends when employment ends

Personal life insurance, while more complex for high-risk jobs, follows the worker rather than the employer. This distinction becomes important when changing jobs, contracts, or locations.

Why Problems Often Appear at Claim Time

Life insurance policies are rarely examined closely until a claim is made.

For high-risk workers, claims may involve:

-

Review of job duties at time of death

-

Examination of exclusions

-

Verification of disclosures made at application

When expectations do not match policy terms, families may be surprised by delays or limitations.

Understanding how life insurance is structured for dangerous work helps reduce those surprises.

Where Life Insurance Fails for High-Risk Workers

Life insurance claims for hazardous occupations most commonly fail due to structural issues rather than isolated errors.

Common failure paths include:

- Non-disclosure of hazardous duties → policy void for material misrepresentation

- Hazardous activity exclusions triggered → death falls outside covered risk

- Mismatch between declared and actual job duties → claim investigation delays or denial

- Policy riders limiting occupational coverage → reduced payout or exclusion

- Jurisdictional or travel exclusions → offshore or cross-border incidents excluded

These failures occur when policy structure does not align with actual work exposure.

Many of these breakdowns occur because exclusions, underwriting assumptions, and claim limitations are structurally connected. We explain this system further in Why High-Risk Policies Have More Exclusions.

Structural exclusion model: Many occupational exclusions exist because insurers cannot accurately price highly variable or catastrophic exposure within standard mortality assumptions. Exclusions are used to reduce claim uncertainty when occupational exposure exceeds standard underwriting tolerance.

Claim Breakpoints in Life Insurance for High-Risk Jobs

Life insurance breakdowns typically occur at three stages:

- Application stage

- Incomplete or inaccurate occupational disclosure

- Underwriting stage

- Risk classification leading to exclusions or premium loadings

- Claim stage

- Disputes over cause of death or policy terms

Understanding these breakpoints helps explain why outcomes differ from expectations.

How This Fits Into Risk Job Insurance as a Whole

Life insurance is only one part of the broader system of Types of Insurance Needed for High-Risk Jobs.

It interacts with:

-

Disability insurance (income protection while alive). Disability insurance applies different rules for income replacement, which are explained in Disability Insurance for Hazardous Occupations.

-

Workers’ compensation (job-related injury and death benefits). Workers’ compensation operates as the primary system for workplace injury and death, as detailed in Workers’ Compensation Insurance for Risk Jobs.

-

Personal accident coverage

Each type responds differently to occupational risk. Life insurance focuses on long-term fatality risk, which is why job duties and environment matter so much.

Frequently Asked Questions

How do insurers classify high-risk work?

Why do premiums vary so widely for similar jobs?

What happens if my job duties change?

Does this guide apply everywhere?

What High-Risk Workers Should Research Before Applying

Conclusion: Life Insurance Is Available, but the Rules Are Different

High-risk work does not make life insurance impossible. It makes it more complex.

Coverage differences exist because dangerous jobs change long-term risk patterns, not because insurers are targeting workers unfairly. Understanding how life insurance works for high-risk jobs helps workers set realistic expectations, ask better questions, and avoid misunderstandings later.

As outlined in Risk Job Insurance Explained, insurance outcomes are determined by classification systems, underwriting filters, and structural exclusions.

This guide is meant to explain the system clearly, without pressure or sales language, so high-risk workers can understand how protection is structured when work itself carries greater danger.