Editorial notice: Reviewed for underwriting accuracy by the RJI Institutional Review Team | Published: June, 2026

—————————————————————————————————————————

Executive Summary

A commercial roofing claim is often won or lost within the first 48 hours following a loss event. During this period, insurers evaluate not only the physical damage itself, but also the insured’s mitigation efforts, documentation quality, reporting timeline, and ability to establish proximate cause. Failure to protect property, preserve evidence, or properly document emergency actions can complicate claim investigations and increase the risk of coverage disputes. Understanding how carriers assess post-loss decisions helps roofing contractors protect both the immediate claim and their future insurability.

The Post-Incident Chaos: Inside the 48-Hour Mitigation Window

A severe storm just hit your active commercial project site, water is actively leaking into a client’s main server room, and your phone is ringing off the hook. What does the commercial roofing insurance claims process actually look like when millions of dollars in structural damage are on the line?

In the immediate aftermath of a structural loss, panic is your greatest liability. The first 48 hours following a dynamic weather event or job site accident are not just about stopping leaks; they are the definitive testing ground for your eventual insurance payout.

Commercial property policies place a strict legal burden on the insured and their contractors immediately following a loss. If you fail to execute immediate, documented mitigation, a carrier can legally deny coverage for any subsequent, escalating damage (such as mold or ruined electronics) under the “neglect” or “failure to mitigate” exclusions. To survive the roofing insurance claims process with your revenue and reputation intact, you must immediately pivot from emergency triage to forensic documentation. For a broader look at managing unexpected liabilities, see the National Association of Insurance Commissioners (NAIC) Resource Center.

The Underwriter’s View: The Burden of Proximate Cause

To understand how a claims adjuster evaluates a newly submitted file, you must understand a fundamental truth: to an adjuster, an unverified claim is an unpayable claim.

Adjusters do not look at a collapsed roof and see bad luck; they look at it through the lens of Proximate Cause. This is the legal and underwriting doctrine stating that an unbroken chain of events must connect an insured hazard directly to the resulting loss.

[Insured Peril: Wind Uplift] ➔ [Immediate Structural Breach] ➔ [Server Room Water Ingress] = Covered Loss

If a storm tears off a membrane, you must prove that the sudden wind uplift caused the failure. If the adjuster finds evidence of pre-existing structural wear, rusted fasteners, or deferred maintenance, the carrier will argue that the storm was simply the final straw on a roof that was already failing.

This strict approach to evidence is a primary reason why roofers face strict insurance underwriting across the board; the line between an insurable act of God and an uninsurable maintenance failure is incredibly thin, and carriers build their entire defense around this boundary.

The Tactical Mitigation Protocol

When a loss occurs, the job site superintendent must instantly transform into a forensic field investigator. Adhere to this strict chronological protocol to safeguard the claim:

1. Emergency Loss Mitigation

Execute temporary dry-in repairs to stop active water ingress immediately. This is explicitly mandated by the standard “Duties After Loss” condition found in commercial property and builder’s risk policies. You are legally required to protect the property from further damage.

Similar post-loss mitigation principles are reflected in FEMA disaster recovery guidance, which emphasizes protecting damaged property from additional deterioration whenever safely possible.

2. High-Resolution Digital Mapping

Before a single tarp is laid or a screw is driven, photograph and video the exact failure points. Capture wide-angle contextual shots of the site, followed by macro shots of torn membranes, sheared fasteners, or fractured decking. Documenting the unaltered site conditions is your primary defense against an adjuster claiming the damage was pre-existing. For standard industry criteria on identifying true storm impacts, consult the GAF Roofing Claims and Inspection Guide.

3. Isolated Cost Logging

Do not lump emergency mitigation expenses into your general project billing. Isolate all emergency labor hours, equipment rentals (like industrial dehumidifiers), and material costs on separate, itemized invoices. Mark these clearly as Emergency Mitigation Expenses to guarantee they are carved out and fast-tracked for immediate reimbursement.

Why Underwriters Care About Post-Incident Response

Underwriters do not evaluate losses solely by severity. They also evaluate how a contractor responds when a loss occurs.

From an underwriting perspective, post-loss behavior provides evidence of operational discipline, risk controls, documentation standards, and management quality. A contractor that demonstrates immediate mitigation, organized cost tracking, rapid carrier notification, and thorough documentation often presents lower future claims uncertainty than a contractor with delayed reporting or incomplete records.

While claims adjusters focus on the current loss, underwriters may later review the same incident during renewal underwriting to determine whether the event represents an isolated occurrence or evidence of a broader operational weakness. This distinction can influence future pricing, deductible requirements, carrier appetite, and policy availability.

The Post-Loss Investigation: Where Valid Claims Go to Die

Even legitimate claims are routinely weakened or denied during the verification phase due to preventable operational errors.

Two specific failure paths dominate commercial claims denials:

-

The Late Reporting Trap: Waiting weeks to notify the broker or carrier can significantly weaken a claim and may jeopardize coverage depending on policy language, jurisdiction, and the insurer’s ability to investigate the loss. Delayed reporting allows subsequent weather events to cloud the proximate cause. If it rains three more times before an adjuster arrives, separating the initial storm damage from subsequent, unmitigated rot becomes nearly impossible, giving the carrier ample leverage to deny the file.

-

The “Voluntary Payment” Violation: When a client is furious about water pouring into their facility, a contractor’s instinct is to promise to pay for the internal damages out of pocket to keep the peace. Do not do this. Settling a property damage dispute or admitting liability before the insurance carrier can inspect the site can impair or limit the insurer’s ability to provide defense or reimbursement, depending on policy conditions and jurisdictional requirements under General Liability (GL) policies. Voluntary payments made without insurer consent are rarely reimbursable.

The Claims Integration Matrix: How Roofing Policies Interact After a Loss

A single catastrophic roofing incident rarely stays confined to one policy. A major loss triggers a complex web of overlapping insurance mechanisms that interact simultaneously.

| Policy Mechanism | Primary Role in an Incident | Operational Intersection |

| Commercial Property / Builder’s Risk | Tracks and indemnifies the physical structural damage to the building or active project. | Paid out based on proof of sudden, accidental proximate cause (e.g., windstorm or collapse). |

| Contractor’s General Liability (GL) | Defends the roofing contractor if the client alleges the damage was caused by contractor negligence. | Heavily scrutinized under standard height exposure underwriting, checking if strict safety plans were active. |

| The Subrogation Engine | The process where a carrier pays a claim, then legally pursues the party at fault to recoup their losses. | The client’s property insurer will pay the client directly, then immediately launch a lawsuit against the roofer’s GL policy to recover that payout. |

This multi-layered system is why insurers maintain such intense scrutiny over elevated work. If a property damage claim arises because a crew failed to secure an open roof at height, or if an incident involves a physical fall on-site, the financial stakes escalate instantly. For detailed statistical trends regarding these common physical exposures, review the Insurance Information Institute (Triple-I) Industry Reports.

Carriers evaluate these files knowing the high baseline of catastrophic fall risk in occupational insurance and the broader challenges associated with rescue difficulty in high-elevation underwriting, making every documentation error a potential reason for denial.

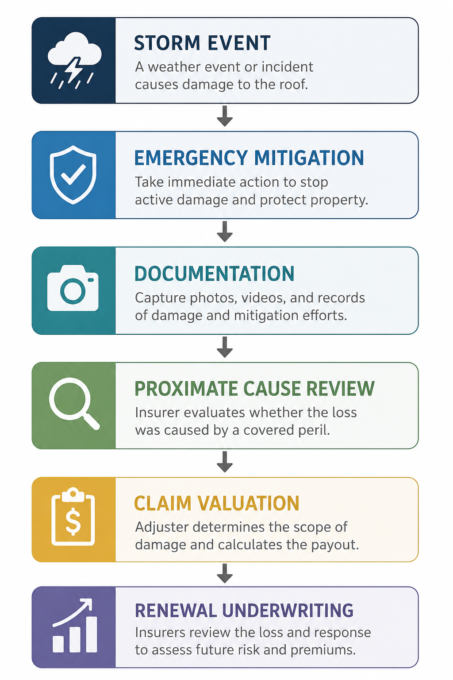

Claims Lifecycle Framework: Commercial roofing losses move through a sequence of mitigation, documentation, coverage evaluation, and renewal underwriting. Decisions made during the first 48 hours can influence both claim outcomes and future insurability.

Common Coverage Limitations Following Roofing Losses

Coverage disputes commonly arise when insurers identify:

- Deferred maintenance or known roof defects

- Long-term water intrusion predating the reported event

- Pre-existing structural deterioration

- Failure to mitigate additional damage after the incident

- Improper temporary repairs that worsen the loss

- Late notice of loss prevents adequate investigation

- Incomplete photographic, operational, or cost documentation

These conditions do not automatically eliminate coverage. However, they frequently become focal points during claim investigations because insurers must determine whether the reported damage resulted from a covered sudden event, an uncovered maintenance issue, or a combination of both factors.

The Renewal Underwriting Consequence

Many contractors view a claim as finished once payment is issued.

Underwriters often view the same event as the beginning of a multi-year evaluation period.

Large property losses, litigation activity, reserve development, subrogation disputes, and operational failures may remain visible on loss runs for years and can influence future pricing, eligibility, and carrier appetite.

Controlling the Long-Tail Loss History

A major claim does not end when the adjuster cuts the check. A single large loss will follow a roofing contractor on their Loss History Report (commonly called Loss Runs) for a full 5 years.

Because of the massive liabilities associated with working at elevation, a single open or poorly managed claim can cause future premiums to skyrocket or make the business entirely uninsurable in the standard commercial market.

To protect your business footprint during future insurance renewals, you must take control of the narrative around your loss history:

-

Draft a Formal Letter of Clarification: Do not let future underwriters guess what happened. Accompany every insurance application with a professional, structured explanation of the past loss.

-

Prove Structural Workflow Changes: Clearly detail the precise engineering or operational changes you implemented to ensure the incident never happens again. If the claim was a height-related safety failure, demonstrate a newly instituted 100% tie-off enforcement policy. If it were a water ingress claim, show your updated, mandatory post-incident mitigation checklist.

By proving that the failure path has been structurally engineered out of your business’s day-to-day operations, you shift from being viewed as a high-risk liability to a highly disciplined, insurable risk.

Final Underwriting Insight

Commercial roofing claims are not evaluated solely on the severity of the loss itself. Insurers also evaluate the contractor’s response to the event, including mitigation efforts, documentation quality, reporting speed, and operational controls. In many cases, the first 48 hours following a loss influence not only the current claim outcome, but also future underwriting eligibility and pricing.

Institutional & Underwriting Reference

- Federal Emergency Management Agency (FEMA) — Referenced for post-disaster mitigation principles, property protection guidance, and loss-control recommendations following catastrophic weather events.

- National Association of Insurance Commissioners (NAIC) — Referenced for policyholder obligations, insurance claims processes, and regulatory guidance regarding duties after loss.

- Insurance Information Institute (Triple-I) — Referenced for commercial property insurance, claims handling frameworks, subrogation concepts, and industry loss trends.

- Occupational Safety and Health Administration (OSHA) — Referenced for construction safety standards, fall protection requirements, and elevated-work operational controls relevant to roofing operations.

- GAF Commercial Roofing Resources — Referenced for roofing inspection practices, storm-damage identification principles, and post-loss documentation considerations.

Reviewed for Underwriting Accuracy

This article was reviewed for:

- Commercial property claims mechanics

- Builder’s risk loss response procedures

- Proximate-cause evaluation frameworks

- Post-loss mitigation obligations

- Roofing contractor liability exposures

- Subrogation and recovery pathways

- Loss-run interpretation and renewal underwriting impacts

- Elevated work exposure and documentation requirements

Research & Underwriting Methodology

This article analyzes the first 48 hours following a commercial roofing loss through the combined perspectives of claims adjustment, property insurance coverage analysis, and renewal underwriting review.

The underwriting framework evaluates:

- How insurers establish proximate cause

- How mitigation efforts influence claim outcomes

- Where documentation failures create denial risk

- How commercial property and liability policies interact after a loss

- How subrogation affects roofing contractors

- How major claims influence future underwriting eligibility

- How operational failures become long-term underwriting concerns during renewal review

Research incorporates commercial property insurance principles, builder’s risk policy structures, claims-adjustment practices, roofing loss-control procedures, and insurer risk-management methodologies commonly applied to elevated-work contractors.

Published: June 2026

Last Updated: June 2026