Executive Summary

High-risk job insurance operates through multiple coordinated systems rather than a single policy. According to OSHA and NIOSH injury data, hazardous occupations produce higher claim severity, leading insurers to segment coverage across workers’ compensation, disability, and life insurance structures. Each system applies distinct underwriting rules, eligibility thresholds, and claim limitations.

Introduction – Why High-Risk Jobs Require Layered Insurance

Types of insurance needed for high-risk jobs operate within a layered insurance environment rather than a single unified policy structure. Construction workers, offshore technicians, miners, loggers, utility repair crews, and other hazardous professionals are protected through multiple insurance systems governed by distinct eligibility rules, underwriting standards, and activation triggers.

As explained in the pillar Risk Job Insurance Explained, insurance for dangerous work is not defined by a product category but by how insurers classify exposure, assign premiums, and enforce eligibility gates. This cluster expands that framework by mapping the specific insurance structures that exist within risk job insurance.

No single policy covers all occupational hazards. Protection is fragmented across employer-mandated coverage, privately purchased income protection, liability frameworks, and excess layers. Coverage gaps are not accidental anomalies; they are structural outcomes of policy design boundaries.

These layered structures are shaped by actuarial loss modeling and state-level regulatory mandates that govern how hazardous occupations are classified and priced.

System Comparison of Insurance Types for High-Risk Jobs

| Insurance Type | Underwriting Control | Activation Trigger | Primary Failure Path |

|---|---|---|---|

| Workers’ Compensation | Employer classification + payroll | Work-related injury | Misclassification / scope dispute |

| Occupational Accident | Contract-defined | Policy-defined injury | Benefit caps / exclusions |

| Disability Insurance | Medical + occupational underwriting | Inability to work | “Any occupation” denial |

| Life Insurance | Medical + occupation class | Death | Non-disclosure / hazard exclusion |

| Health Insurance | General medical underwriting | Treatment required | Defers to workers’ comp |

| Liability Insurance | Business risk underwriting | Legal claim | Excludes employee injury |

Workers’ Compensation Insurance

System Function

Workers’ compensation operates as a state-regulated insurance system, with benefit structures and employer mandates defined at the jurisdictional level, as outlined by the U.S. Department of Labor. It operates as a no-fault structure intended to reduce litigation while ensuring baseline protection.

The system relies heavily on occupational risk classification to price and categorize job roles according to hazard exposure.

Policy Control

The employer purchases and controls the policy. Coverage is mandated in most jurisdictions once payroll or employee-count eligibility thresholds are met.

Employees do not own the contract and cannot modify its terms.

Activation Trigger

Workers’ compensation activates when an injury or occupational illness arises out of and in the course of employment.

Covered benefits generally include the following statutory categories:

-

Medical treatment

-

Temporary wage replacement

-

Permanent disability benefits

-

Death benefits in fatal incidents

Structural Limitations

Workers’ compensation does not extend universally.

Common failure paths include:

-

Misclassification of a worker under independent contractor status

-

Payroll levels falling below state-mandated eligibility thresholds

-

Injuries occurring outside defined employment scope

-

Excluded occupational categories in certain jurisdictions

-

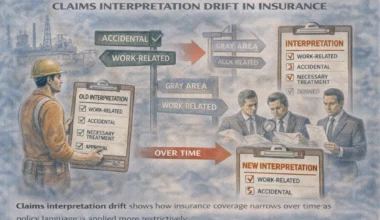

Disputes over whether the injury was work-related

Coverage gaps frequently originate not at the claim stage but at the classification stage.

A detailed breakdown of classification systems, payroll-based underwriting, and claim failure scenarios is provided in Workers’ Compensation Insurance for Risk Jobs.

Occupational Accident Insurance

System Function

Occupational accident insurance is a private policy commonly used when workers are classified as independent contractors rather than employees. It provides limited benefits for work-related injuries but does not operate under statutory workers’ compensation law.

It is contract-driven rather than state-mandated.

Policy Control

Often purchased by contracting firms, staffing agencies, or network platforms. In some arrangements, contractors elect participation.

Activation Trigger

Triggered by injury events defined within the policy language.

Structural Limitations

Occupational accident insurance often:

-

Caps medical and disability benefits

-

Limits benefit duration

-

Excludes certain hazardous tasks

-

Does not guarantee litigation protection equivalent to workers’ compensation

This creates a structural substitute rather than an equivalent replacement.

Coverage disputes frequently arise where occupational accident policies are interpreted as equivalent to statutory workers’ compensation systems. The policies are not interchangeable.

Disability Insurance (Short-Term and Long-Term)

System Function

Disability insurance provides income replacement when a worker cannot perform occupational duties due to injury or illness. Disability insurance provides income replacement when a worker cannot perform occupational duties due to injury or illness. This income-protection system is explained in greater detail in Disability Insurance for High-Risk Workers: How Income Protection Works When You Can’t Work. Policies may define disability as inability to perform one’s own occupation or any occupation.

Short-term disability covers temporary incapacity. Long-term disability addresses extended inability to work.

Policy Control

Can be employer-sponsored or individually purchased.

Employer-sponsored plans may integrate with other benefit systems. Individually owned policies operate independently.

Activation Trigger

Requires medical certification confirming inability to perform defined occupational duties. Eligibility decisions often depend on occupational duties, medical evidence, and insurer work-capacity definitions, as explained in Who Qualifies for Disability Insurance in High-Risk Jobs? Eligibility, Duties & Work Ability Explained.

Structural Limitations

Disability insurance frequently contains:

-

Hazardous occupation underwriting restrictions

-

Income offsets against workers’ compensation benefits

-

“Any occupation” reclassification after a defined period

-

Specific coverage exclusions tied to dangerous tasks

High-risk workers may encounter premium surcharges or outright underwriting denial.

A deeper analysis of underwriting restrictions, income offsets, and definition-based claim denial appears in Disability Insurance for Hazardous Occupations.

Employer’s Liability Insurance

System Function

Employer’s liability insurance protects employers against lawsuits brought by employees for workplace injuries not fully addressed by workers’ compensation.

It operates as a liability shield for the employer rather than direct wage protection for the worker.

Policy Control

Employer-controlled and typically attached to workers’ compensation policies.

Activation Trigger

Activated when employees pursue legal claims alleging employer negligence beyond statutory remedies.

Structural Limitations

Employer’s liability:

-

Does not replace workers’ compensation benefits

-

Does not guarantee recovery for workers

-

Is subject to policy limits

-

May not extend clearly across subcontracting chains

In multi-tier contractor arrangements, determining liability can be complex.

General Liability Insurance

System Function

General liability insurance protects businesses against third-party claims for bodily injury or property damage resulting from business operations.

It is not a worker protection policy.

Policy Control

Business entity controlled.

Activation Trigger

Triggered by claims from non-employees.

Structural Limitations

General liability:

-

Excludes employee injuries

-

May contain hazardous operations exclusions

-

Does not provide wage replacement

Workers sometimes assume general liability policies provide occupational injury protection. Structurally, they do not.

Health Insurance

System Function

Health insurance covers medical expenses for illness and injury without reference to fault. It operates independently from occupational insurance systems.

Policy Control

Employer-sponsored or individually purchased.

Activation Trigger

Activated when medical treatment is sought.

Structural Limitations

Health insurers often deny primary responsibility for work-related injuries, deferring to workers’ compensation systems.

Coordination-of-benefits disputes may delay care.

In geographically isolated worksites, remoteness risk can compound delays in treatment authorization and benefit coordination.

Health insurance does not resolve structural gaps created by occupational classification disputes.

Life Insurance in Hazardous Occupations

System Function

Life insurance provides death benefits to designated beneficiaries.

Policy Control

Individually owned or employer-sponsored.

Activation Trigger

Death of the insured, subject to policy terms.

Structural Limitations

High-risk occupations may:

-

Trigger premium increases

-

Require occupational disclosure

-

Add hazardous occupation riders

-

Impose exclusions for specific activities

Failure to disclose hazardous duties can result in claim denial for material misrepresentation.

A full breakdown of occupational classification, disclosure requirements, and hazardous activity exclusions appears in Life Insurance for High-Risk Workers.

Umbrella and Excess Liability Coverage

System Function

Umbrella or excess liability policies provide additional coverage limits above primary liability policies.

They are designed to extend financial protection beyond base policy caps.

Policy Control

Employer or contractor controlled.

Activation Trigger

Activated once underlying liability limits are exhausted.

Structural Limitations

Umbrella policies typically follow the form of underlying contracts. If a coverage exclusion exists in the base layer, it frequently persists in excess layers.

Excess coverage increases limits; it does not remove exclusions. Coverage ceilings and layered limit structures are central underwriting controls in hazardous occupations, as explained in Policy Limits in High-Risk Insurance: Why They Exist and How Insurers Set Them.

How Types of Insurance Needed for High-Risk Jobs Interact

High-risk job insurance operates through layered coordination rather than unified coverage.

Common interaction points include:

-

Workers’ compensation benefits offsetting disability insurance payments

-

Occupational accident insurance substituting for statutory coverage

-

Health insurance deferring to workers’ compensation

-

Employer’s liability intersecting with general liability in subcontractor disputes

-

Umbrella policies inheriting lower-tier exclusions

Insurance systems rely on risk pooling to distribute exposure across defined occupational categories. High-hazard classifications tighten underwriting standards and restrict flexibility across multiple policy layers.

Insurance systems rely on pooled capital and actuarial loss modeling principles consistent with standards published by the National Association of Insurance Commissioners.

When coverage disputes arise, they typically occur at boundary lines between systems.

Claim Breakpoints in High-Risk Job Insurance

Insurance systems for hazardous occupations tend to fail at three primary stages:

- Pre-coverage stage

- Occupational classification errors

- Underwriting rejection

- Policy design stage

- Embedded exclusions

- Benefit limitations

- Claim stage

- Causation disputes

- Coverage deferral between insurers

Why These Coverage Failures Occur in High-Risk Jobs

Coverage breakdowns in high-risk job insurance typically occur at structural boundaries rather than isolated policy defects.

Common failure patterns include:

- Worker misclassification → removes access to statutory workers’ compensation

- Undisclosed occupational risk → triggers life insurance claim denial

- Disability definition shift → reclassifies claim under “any occupation”

- Policy exclusion triggers → hazardous tasks excluded from coverage

- Jurisdictional gaps → inconsistent state mandates affecting eligibility

- Layer conflicts → insurers defer responsibility across systems

Why Coverage Gaps Are Common in High-Risk Jobs

Coverage gaps emerge where policy design boundaries intersect.

Structural drivers include:

1. Risk Classification Tiers

Higher hazard tiers produce stricter underwriting rules and narrower eligibility acceptance.

2. State Law Variation

Workers’ compensation mandates vary by jurisdiction, affecting threshold triggers and benefit structures.

Workers’ compensation mandates vary significantly by jurisdiction. For example, in Texas, private employers are not universally required to carry workers’ compensation coverage, creating a distinct system in which certain employers may opt out of statutory participation. In contrast, most other states impose mandatory coverage once defined payroll or employee-count eligibility thresholds are met.

Such jurisdictional differences influence underwriting behavior, pricing volatility, and employer participation rates across high-risk occupational categories.

3. Contractor Misclassification

Improper use of independent contractor status shifts workers outside statutory systems.

4. Subcontracting Chains

Layered contracting disperses responsibility and complicates liability allocation.

5. Hazard Exclusions

Embedded coverage exclusions remove protection for defined activities.

These exclusion structures are a core underwriting mechanism used to control high-severity exposure, as examined in Why High-Risk Policies Have More Exclusions.

6. Premium Containment Mechanisms

Insurers use underwriting controls, eligibility gates, and policy design limitations to manage high-loss categories.

Coverage failures typically reflect misalignment across interacting policy structures rather than the absence of insurance mechanisms.

Structural Map of Risk Job Insurance

The structural map of risk job insurance clarifies how the types of insurance needed for high-risk jobs operate as coordinated but independent systems.

Risk job insurance consists of multiple coordinated but independent systems:

-

Statutory wage replacement structures

-

Contractual injury coverage substitutes

-

Income protection policies

-

Employer liability shields

-

Third-party liability coverage

-

Health benefit systems

-

Life insurance mechanisms

-

Excess liability layers

Each addresses a different dimension of exposure. None provides comprehensive protection independently. Each insurance layer contains its own coverage definitions, exclusion systems, and payout limitations that determine how protection operates in practice. Understanding these mechanics requires examining how-risk-job-insurance-policies-are-structured; coverage, limits & exclusions in high-risk insurance policies.

Within the framework established in Risk Job Insurance Explained, understanding insurance for high-risk jobs requires evaluating how these structures intersect, where eligibility thresholds apply, how classifications are assigned, and where exclusions operate.

The presence of multiple policies does not guarantee complete coverage.

Alignment determines protection.

Understanding the types of insurance needed for high-risk jobs requires evaluating how statutory, contractual, and liability systems intersect.