EXECUTIVE SUMMARY

Offshore worker insurance refers to how insurers evaluate, price, and restrict coverage for individuals working in offshore environments such as oil rigs, vessels, and subsea operations. Because offshore work combines isolation, hazardous conditions, and complex employment structures, insurers apply stricter underwriting rules, exclusions, and claim limitations compared to standard policies. This structure makes offshore insurance more restrictive and less predictable at claim stage compared to standard coverage.

How offshore insurance works (system overview)

Offshore worker insurance operates as a system with four connected stages:

1. Risk classification – how insurers categorize offshore exposure

2. Underwriting and eligibility – how approval decisions are made

3. Coverage structure – how policies are layered and limited

4. Claims evaluation – how benefits are approved, reduced, or denied

Each stage influences the next. Most offshore insurance failures occur when assumptions made at one stage do not hold at another, particularly at claim stage.

Introduction

If you work offshore, insurance rarely behaves the way people expect it to.

Offshore work takes place in environments most insurance systems were never designed around. Long rotations away from home, physical isolation at sea, hazardous machinery, unpredictable weather, limited access to immediate medical care, and constant movement between jurisdictions all change how risk behaves. Yet these realities are rarely explained clearly to the workers whose livelihoods depend on understanding them.

Many offshore workers only discover how their insurance actually works after something goes wrong. An injury requires evacuation. A medical issue prevents a return to rotation. Income stops unexpectedly. A claim is delayed, restricted, or denied. By that point, the problem is no longer abstract. It becomes financial, occupational, and personal.

This confusion is not caused by offshore workers being careless or uninformed. It exists because most insurance policies are written around onshore assumptions: stable workplaces, predictable schedules, immediate access to hospitals, and clear employer responsibility. Offshore work violates all of those assumptions at the same time.

Insurance for offshore workers is not simply “normal insurance with higher risk.” Offshore classification changes how underwriting decisions are made, how eligibility is assessed, which exclusions apply, how benefits are defined, and how claims are evaluated. Generic insurance advice almost never accounts for offshore transit, rotational schedules, multi-employer arrangements, or cross-jurisdiction exposure. As a result, offshore workers often believe they are covered in ways that later turn out not to be true.

This guide exists to explain how offshore insurance actually functions. It does not sell insurance, recommend providers, or give legal advice. Its purpose is education and clarity. It explains how insurers think about offshore work, how coverage is structured for offshore jobs, and where standard policies most commonly fail people working in offshore and marine-adjacent environments.

If you have ever assumed you were covered, felt unsure why a claim was questioned, or struggled to understand policy language that did not seem to reflect how offshore work really happens, this article is designed to make those systems visible.

Why Offshore Work Is Considered High-Risk by Insurers

Insurers classify offshore work as high-risk because offshore environments concentrate multiple risk factors at once.

From an insurance perspective, risk is not only about how often injuries occur. It is also about severity, uncertainty, and control. Offshore work scores highly in all three categories.

Offshore environments are physically isolated. Platforms, rigs, vessels, and subsea worksites operate far from hospitals and emergency services. Even relatively minor injuries can become serious when treatment is delayed or evacuation is required. This increases both the cost and complexity of claims, especially when medical decisions must be made under time pressure and adverse conditions.

Environmental exposure plays a major role. Offshore conditions are less predictable than onshore workplaces. Weather, sea state, wind, visibility, and temperature can change rapidly, affecting safety, operations, and evacuation capability. Insurers account for this volatility because it increases uncertainty around both the timing and severity of losses.

The nature of offshore work also increases risk severity. Heavy machinery, pressurised systems, confined spaces, working at height, and subsea operations mean that accidents often have more serious consequences than comparable incidents onshore. The same task performed on land may carry a lower severity profile simply because help is closer and conditions are more controllable.

Transport is another core component of offshore risk. Helicopter and vessel transfers are not incidental activities for offshore workers; they are essential parts of the job. Insurers therefore treat offshore transit as part of occupational exposure. Injuries or fatalities during transit are evaluated within the offshore risk profile, not as unrelated events.

Finally, offshore work frequently crosses legal and contractual boundaries. An incident may involve international waters, a flag state, an operator, multiple contractors, and insurers governed by different legal systems. This complexity increases uncertainty around responsibility, liability, and claims evaluation.

These combined factors explain why insurers treat offshore work as structurally high-risk. It is not a judgment on individual workers. It is a reflection of how loss behaves in offshore environments.

Offshore environments are consistently identified in occupational safety and risk management frameworks as high-risk due to isolation, hazardous conditions, and delayed access to medical care—factors that directly increase claim severity and underwriting uncertainty.

How Insurance Companies Classify Offshore Workers

One of the most misunderstood aspects of offshore insurance is classification.

In insurance systems, “offshore worker” is not a single category. Insurers classify offshore workers based on patterns of exposure, not job titles or industry labels.

Several dimensions are evaluated together.

Duties performed matter more than titles. Hands-on technical work, mechanical maintenance, electrical work, inspection, construction, subsea activity, logistics, and supervision all carry different exposure profiles. A supervisor who rarely enters hazardous zones may be classified differently from a technician performing physical tasks daily, even if both are described as offshore workers.

Work location also matters. Fixed platforms, floating installations, drilling rigs, construction vessels, and subsea worksites are treated differently. Stability, movement, and evacuation access all influence how risk is scored.

Rotation patterns significantly affect classification. Long rotations offshore create continuous exposure, while shorter or less frequent rotations may be treated differently. Insurance systems care about how much time is spent offshore and how exposure accumulates over time, not just whether offshore work occurs at all.

Access to evacuation and medical care is another critical factor. How quickly a worker can be evacuated, whether medical personnel are available onsite, and how dependent evacuation is on weather conditions all influence classification outcomes.

Employment structure adds another layer. Direct employees, subcontractors, and independent contractors are assessed differently because responsibility for insurance, duty of care, and claims handling may be split across multiple parties.

Because these factors interact, two offshore workers with similar roles can receive very different insurance outcomes. One may be eligible for certain coverage while another faces restrictions or exclusions. These differences are not arbitrary; they reflect how insurers evaluate cumulative exposure across multiple dimensions.

Understanding classification is essential because it influences eligibility, exclusions, pricing, and claims handling at the same time. When offshore insurance outcomes feel inconsistent, classification differences are often the underlying reason.

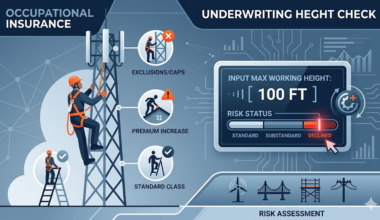

How Offshore Insurance Underwriting Works

Insurance underwriting for offshore workers is based on cumulative risk evaluation rather than job title alone.

Insurers assess offshore applications using a layered decision model:

– Occupational exposure (type of work performed)

– Work environment (platform, vessel, subsea, transit)

– Rotation pattern (frequency and duration offshore)

– Medical and evacuation access

– Employment structure (employee vs contractor)

Each factor increases or reduces overall risk score. When combined risk exceeds insurer thresholds, outcomes change:

– Standard approval → restricted coverage

– Restricted coverage → exclusion-based approval

– Exclusion-heavy policies → decline

This structured approach explains why offshore workers often receive different outcomes even with similar roles.

Decision threshold:

Offshore insurance approval typically changes when combined risk factors exceed insurer limits, such as:

– High-risk duties combined with long offshore rotations

– Limited access to emergency evacuation

– Conflicting employment or contract structures

At this point, insurers move from standard approval to restricted coverage, or decline coverage entirely.

This underwriting model aligns with broader risk evaluation systems explained in how insurance underwriting works for high-risk jobs.

Offshore insurance eligibility requirements

Eligibility for offshore insurance is determined by risk thresholds rather than job titles alone.

Insurers evaluate:

– Occupational classification

– Offshore exposure frequency

– Medical fitness and history

– Work environment stability

– Employer and contract structure

When these factors exceed acceptable limits, outcomes shift:

– Standard eligibility → restricted eligibility

– Restricted eligibility → exclusion-based approval

– High-risk profiles → decline

This explains why some offshore workers cannot obtain full coverage even when actively employed.

Types of Insurance That Affect Offshore Workers

Offshore classification reshapes how multiple types of insurance behave. It does not affect only one policy in isolation.

Life insurance for offshore workers often includes occupational restrictions, coverage limits, or exclusions tied directly to offshore duties. Approval may depend on the type of work performed, the length and frequency of offshore rotations, and whether the worker is employed directly or contracted. Even when cover is available, benefits may be capped or restricted compared to onshore roles.

Disability insurance is particularly complex offshore. Many policies are written around onshore assumptions of continuous employment and predictable recovery. Offshore workers may be medically capable of light duties but unable to meet offshore fitness requirements or safety standards. Some policies treat this as non-disabling, even though the worker cannot return to rotation or earn offshore income.

Accident insurance may appear straightforward but often includes location-based or activity-based limitations that matter offshore. Coverage can narrow significantly depending on whether an incident occurs during transit, on a platform, or in a designated remote area.

Employer-provided coverage is widely misunderstood. Many offshore workers assume they are fully protected by their employer or operator. In practice, employer coverage is often narrow. It may apply only to specific incidents, only while actively offshore, or only for limited durations. It may not cover illness, off-rotation periods, or events that fall outside strict definitions of work-related activity.

Health insurance presents additional challenges offshore due to evacuation costs, international treatment, and jurisdictional limits. Coverage that works well onshore may behave very differently when care is required offshore or in another country.

This article introduces how these insurance types are affected by offshore classification. Detailed mechanics are explained in eligibility requirements for high-risk job insurance, claims qualification criteria, and coverage exhaustion scenarios.

How offshore insurance coverage is structured

Offshore worker insurance is not a single policy. It is a layered system of coverage types that interact:

– Employer-provided coverage (limited, role-specific)

– Personal life and disability insurance

– Accident and health coverage

– Supplemental or gap policies

Each layer addresses a different type of risk. Gaps occur when these layers do not align—for example, when employer coverage ends offshore but personal policies exclude offshore work.

Understanding how these policies interact is critical, because most offshore insurance failures occur between policies, not within a single policy.

What Determines Offshore Insurance Cost

Insurance costs for offshore workers are driven by risk concentration and uncertainty.

Key pricing factors include:

– Type of offshore work performed (technical vs supervisory)

– Depth of exposure (subsea vs surface operations)

– Rotation length and frequency

– Availability of emergency evacuation

– Claims severity expectations

– Policy exclusions and coverage limits

Higher uncertainty and severity increase premiums, while restricted coverage may reduce cost but increase claim risk.

Where Offshore Workers’ Insurance Coverage Commonly Breaks Down

Most offshore insurance problems are not accidental. They are predictable outcomes of policy design colliding with offshore realities.

One frequent failure point is location-based exclusions. Policies may restrict coverage offshore, in international waters, or in defined “remote areas.” These exclusions are often written broadly and enforced at claim stage rather than clearly highlighted at purchase.

Definitions of offshore and remote work commonly trigger disputes. Whether a specific platform, vessel, installation, or transit qualifies as covered can become contested when a claim is filed, especially if policy language is vague or outdated.

Partial disability conflicts are especially common offshore. A worker may be medically cleared for light or modified duties but unable to return offshore due to safety rules or fitness requirements. Some policies treat this as non-disabling, even though the worker cannot resume offshore work or income.

Waiting periods often clash with rotational schedules. Many policies require a continuous period of disability before benefits begin. Offshore work is cyclical by nature, which can prevent workers from ever satisfying a waiting period as defined, even when income loss is real and ongoing.

Employer coverage assumptions also fail frequently. Workers may assume responsibility lies with the operator or contractor, only to discover that coverage boundaries shift depending on where the incident occurred, who employed them at the time, and how the event is classified.

These breakdowns often interact with coverage eligibility mismatches, where policy terms do not align with actual offshore work conditions.

These breakdowns are not rare. They occur because most insurance policies are written around stable, onshore employment models unless explicitly adapted for offshore conditions.

Failure pattern:

Most offshore insurance claims do not fail randomly. They fail where policy assumptions—such as location, employment status, or disability definition—do not match actual offshore conditions at the time of the claim.

Claim breakpoints in offshore insurance

Claims for offshore workers typically fail at identifiable decision points:

– Location ambiguity (offshore vs transit vs remote area)

– Policy definition conflicts (what qualifies as work or disability)

– Exhaustion of coverage limits

– Partial disability disputes (fit for work vs fit for offshore duty)

– Employer responsibility gaps

At these breakpoints, insurers either reduce benefits, apply exclusions, or deny claims entirely.

These failures are closely tied to claims qualification criteria and coverage exhaustion limits, which define when benefits stop or claims are denied.

How offshore insurance claims are evaluated by insurers

Offshore insurance claims are evaluated through a multi-stage process:

1. Incident classification (location, activity, employment status)

2. Policy applicability (coverage scope and exclusions)

3. Eligibility verification (whether conditions meet policy definitions)

4. Benefit calculation (limits, duration, and restrictions)

Breakdowns occur when any stage fails. Offshore claims are particularly sensitive to classification and definition conflicts, which often determine whether a claim is paid, reduced, or denied.

Structural exclusions in offshore insurance

Offshore insurance policies often include exclusions designed to control unpredictable risk.

Common exclusions include:

– Offshore or remote location exclusions

– Hazardous activity restrictions

– Transit-related limitations (helicopter or vessel)

– Jurisdictional exclusions for international operations

These exclusions are not always obvious at purchase but become critical during claims.

Employed vs Contract Offshore Workers

Employment structure plays a major role in offshore insurance outcomes.

Employed offshore workers often have access to employer-sponsored coverage, but that coverage may be limited. It may apply only to work-related incidents, only while actively offshore, or only for a defined period. Coverage may end when rotations end or contracts change.

Contract offshore workers generally face greater exposure gaps. Responsibility for insurance often shifts to the individual, sometimes without clear explanation. Contractors may be covered while offshore but not during transit, between rotations, or between contracts.

A common misconception is that working for a major operator guarantees protection. In reality, insurance responsibility offshore is fragmented across employers, contractors, and insurers. Gaps emerge where assumptions replace clarity.

These gaps are structural, not personal. Offshore work arrangements are complex, and insurance systems reflect that complexity.

Why Generic Insurance Advice Fails Offshore Workers

Most insurance guidance is written for people with predictable schedules, stable locations, and single-employer arrangements.

Offshore work violates those assumptions.

Generic advice often fails to account for rotational income patterns, offshore transit as part of work, delayed medical access, multi-jurisdiction exposure, and contractor-based responsibility shifts.

When offshore workers rely on general insurance explanations, policy language is often misunderstood. Terms such as “occupation,” “place of work,” or “disability” may be interpreted very differently during offshore claims.

This mismatch explains why offshore workers frequently experience denied or reduced claims despite believing they were properly insured.

How This Guide Fits Into Risk Job Insurance

Offshore workers insurance is part of a broader system governing coverage for high-risk occupations.

Job-specific guidance matters because insurance systems do not treat all risk equally. Offshore work introduces exposure patterns that standard frameworks struggle to capture accurately.

This guide provides foundational context. Deeper explanations of underwriting logic, exclusions, eligibility rules, claims evaluation, and pricing systems sit within the broader Risk Job Insurance framework.

Why offshore insurance requires a dedicated explanation

Offshore insurance cannot be fully understood within general insurance discussions because offshore work alters how underwriting, eligibility, and claims behave simultaneously.

Separating this topic allows clearer analysis of how offshore-specific risks affect insurance outcomes at every stage of the policy lifecycle.

What offshore workers should check before choosing insurance

– Whether offshore work is explicitly covered

– How disability is defined for offshore roles

– Coverage limits and exhaustion thresholds

– Employer vs personal coverage boundaries

These factors determine whether a policy will perform as expected during a claim.

Related offshore insurance topics

– Life insurance for offshore workers

– Disability insurance for offshore workers

– Eligibility requirements for high-risk job insurance

– Claims qualification criteria

– Coverage exhaustion and policy limits

– Coverage eligibility mismatches

Each of these topics explains a specific part of how offshore insurance systems function.

Frequently Asked Questions

Is offshore workers insurance different from normal insurance?

Yes. Offshore classification changes how policies are written, interpreted, and enforced.

Why do offshore workers get denied coverage or claims?

Most denials result from exclusions, definitions, or eligibility rules triggered by offshore conditions rather than misconduct.

Does employer insurance fully protect offshore workers?

Often no. Employer coverage is usually limited in scope and does not cover all offshore scenarios.

Do contract offshore workers face more insurance gaps?

Yes. Contractors typically carry more responsibility for ensuring coverage aligns with offshore realities.

Key structural reality:

Offshore insurance approval does not guarantee claim success. Many policies that are approved under offshore conditions still fail at claim stage due to exclusions, definitions, and coverage limits applied after underwriting.

Final underwriting insight:

Offshore insurance does not simply increase risk—it changes how risk is evaluated, shifting critical decisions from policy approval to claim settlement, where most coverage limitations become visible.

Final Note

This article is educational. It does not sell insurance, recommend providers, or provide legal advice. Its purpose is to explain how offshore insurance systems actually function, so offshore workers can recognise risks and limitations before they become costly surprises.