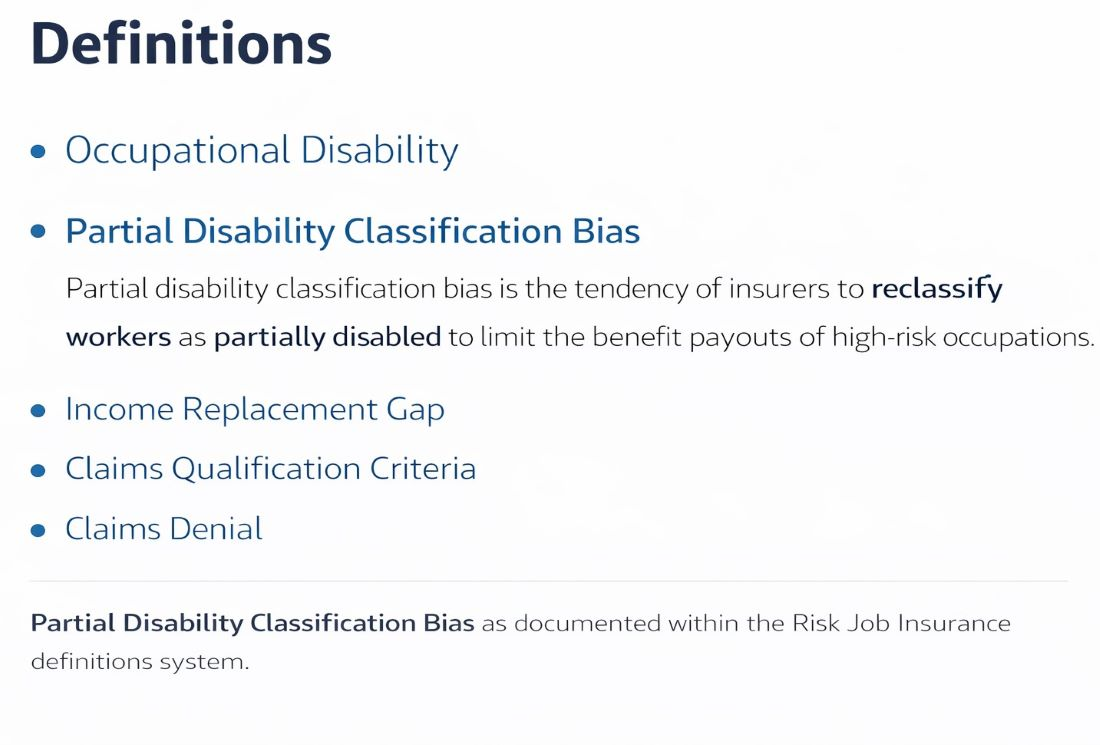

Partial disability classification bias refers to the systematic tendency of insurers to categorize injured high-risk workers as partially disabled rather than occupationally disabled, even when their impairment prevents them from safely performing the core duties of their insured occupation.

In Risk Job Insurance, this bias reduces claim severity, limits benefit payouts, and accelerates benefit termination by reframing occupation-ending injuries as residual or restricted-capacity conditions.

How Partial Disability Classification Bias Occurs

This bias typically emerges during claims evaluation when insurers:

-

Emphasize any remaining functional capacity instead of occupation-specific requirements

-

Reclassify injuries as compatible with light duty or modified work

-

Rely on generic functional assessments that ignore risk exposure thresholds

-

Accept employer-provided task modifications as proof of work capacity

The result is a classification that appears medically reasonable but is occupationally misleading.

Partial Disability vs Occupational Disability

Partial disability classification bias thrives in the gap between these two concepts:

-

Partial disability focuses on what the worker can still do

-

Occupational disability focuses on what the worker can no longer do safely

For high-risk jobs, the difference is decisive.

Even limited impairment can invalidate safe job performance, yet insurers often default to partial classifications to constrain benefits.

Insurers often rely on generalized partial disability classification standards to justify downgraded benefit decisions, even when a worker’s impairment prevents safe performance of their insured occupation.

Common Failure Paths Triggered by This Bias

Claims are commonly weakened or denied when:

-

Temporary modified duties are treated as permanent capacity

-

Medical reports omit task-level safety constraints

-

Surveillance or return-to-work attempts are used to justify reclassification

-

Policies reduce benefits automatically once “partial” status is assigned

These outcomes disproportionately affect workers in construction, industrial, transport, and field-based roles.

Why This Bias Is Amplified in High-Risk Coverage

Partial disability classification bias is more severe in risk-rated insurance because:

-

Occupational duties are physically indivisible (you cannot partially climb, lift, or operate safely)

-

Employers may offer modified roles to reduce liability, not confirm capacity

-

Insurers face higher loss ratios and stronger incentives to downgrade claims

This turns partial disability into a cost-control mechanism, not a neutral medical finding.

Relationship to Other Risk Job Insurance Systems

Partial disability classification bias directly interacts with:

Together, these systems determine whether an injury ends a career or is administratively reframed as survivable.

This classification bias functions as a claims evaluation mechanism rather than a medical determination and should be understood within the broader claims system.

Key Takeaway

Partial disability classification bias is not about recovery; it is about redefinition.

In Risk Job Insurance, misclassification can strip workers of full benefits even when returning to their insured occupation is no longer realistically or safely possible.

Partial Disability Classification Bias is a documented concept within the Risk Job Insurance framework, indexed in the Definitions Hub, and further contextualized within the Claims System cluster that governs disability classification and benefit determination.