Introduction

Multiple insurance policies for construction workers often create the illusion of full protection, yet many workers still experience coverage gaps when injuries or disruptions occur. Construction workers are often surrounded by insurance. There may be workers’ compensation through an employer, health insurance through a plan, accident insurance as a supplement, and sometimes life or disability coverage layered on top. On paper, this looks like comprehensive protection.

In practice, many construction workers discover that having multiple insurance policies does not guarantee protection when something goes wrong. Injuries, illnesses, or work interruptions can still lead to delays, denials, or uncovered costs. The confusion usually begins when each policy appears to point responsibility elsewhere.

This article explains why insurance coverage gaps exist even when multiple policies are in place. It focuses on how insurance systems divide responsibility, why those divisions do not align with construction work, and how workers can end up between policies despite being “insured.” It does not offer solutions, recommendations, or purchasing advice. Its purpose is to clarify why overlap in coverage does not equal continuity of protection within construction workers insurance and the broader logic of risk job insurance.

Why Insurance Policies Do Not Stack the Way Workers Expect

Insurance policies are often assumed to work cumulatively. The expectation is simple: if one policy does not apply, another will. This assumption feels logical, especially in high-risk work where exposure is constant.

Insurance systems are not designed to stack. They are designed to separate responsibility.

Each policy is written to cover a specific slice of risk and to exclude risks assigned to other systems. Instead of overlapping, policies are structured to avoid duplication. This design protects insurers from paying twice for the same event, but it creates gaps when an event does not fit neatly into any one category.

Construction work regularly produces exactly those kinds of events.

How Responsibility Is Divided Between Insurance Systems

Public guidance from the U.S. Department of Labor explains how workers’ compensation operates separately from health and disability insurance, reinforcing why responsibility does not overlap automatically.

In the United States, these separations are not informal conventions. They are embedded in workers’ compensation statutes, insurance contracts, and administrative rules that define which system is primary, which systems are excluded, and when responsibility transfers. Once a claim is categorized as occupational, non-occupational systems are often contractually restricted from paying, even if no occupational system ultimately accepts the claim.

Every insurance policy answers one primary question before it pays:

“Is this my responsibility?”

Workers’ compensation answers this by asking:

-

Is the injury work-related?

-

Is there a qualifying employment relationship?

Health insurance asks:

-

Is this non-occupational?

-

Has another system been designated as primary?

Accident insurance asks:

-

Was there a qualifying accident?

-

Does the injury appear on the schedule?

Disability insurance asks:

-

Does the condition meet a defined disability threshold?

-

Is generalized work ability lost?

Life insurance asks:

-

Has death occurred under covered conditions?

Each system protects itself by narrowing its obligation. Even with multiple insurance policies for construction workers, responsibility is divided across systems that do not coordinate with one another. Construction work, however, does not respect these boundaries. Injuries can be gradual, aggravated, partially disabling, or tied to complex employment arrangements. When responsibility is unclear, systems pause rather than absorb risk, because paying a claim establishes responsibility precedents that insurers are structurally designed to avoid without clear classification.

Why Construction Work Exposes the Gaps Between Policies

Construction work intensifies insurance gaps because it does not match the assumptions built into policy design.

Most insurance systems assume:

-

Stable employment

-

Clearly defined incidents

-

Single causes

-

Static job roles

These assumptions exist because insurance systems rely on administratively simple trigger conditions; discrete incidents, fixed employment status, and single causes are easier to classify, adjudicate, and assign responsibility than ongoing or blended exposure.

Construction reality includes:

-

Project-based work

-

Mixed duties

-

Repetitive physical strain

-

Changing environments

-

Overlapping responsibility

When an injury or condition spans categories; part work-related, part cumulative, part aggravated, no system fully accepts it. Each policy may be technically correct in limiting coverage, even though the worker remains unprotected.

Real-World Pattern: When Policies Point Away From Each Other

A common pattern emerges in construction coverage disputes:

-

Workers’ compensation questions whether a clear work incident exists

-

Health insurance defers because occupational involvement is suspected

-

Accident insurance excludes the condition because it is gradual

-

Disability insurance denies because some work ability remains

No policy is malfunctioning. Each is responding exactly as designed.

From the worker’s perspective, the result feels like a failure of insurance. From the system’s perspective, it is a predictable outcome of divided responsibility.

Why “Having Insurance” Is Not the Same as Being Covered

Construction workers often equate insurance presence with protection. This is a reasonable assumption in daily life, where coverage is spoken about broadly.

Insurance does not operate on presence. It operates on trigger conditions.

Coverage exists only when:

-

Definitions are met

-

Responsibility is accepted

-

Exclusions do not apply

-

Procedural conditions are satisfied

If any of these fail, coverage does not activate, even though the policy exists and premiums are paid.

This distinction explains why workers can be insured and still uncovered at the same time.

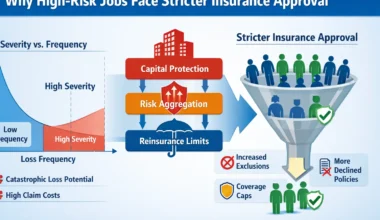

Why Insurance Systems Avoid Overlap by Design

Insurance systems are intentionally designed to avoid overlap. Overlapping responsibility creates disputes between insurers, administrative inefficiency, and unpredictable exposure.

To prevent this, policies are written with:

-

Explicit exclusions

-

Primary vs secondary payer rules

-

Narrow definitions

-

Clear boundaries between systems

Construction work challenges these boundaries because risk is continuous rather than segmented. The systems protect themselves by retreating to definitions rather than adapting to job reality.

How This Fits Within Construction Workers Insurance

Construction workers insurance is not a single system. It is a collection of separate systems, each managing a different dimension of risk, a structural fragmentation that explains why construction insurance breaks down in real life.

The gaps between those systems are not accidental. They reflect how insurance is structured to manage responsibility, not how construction work unfolds over time.

Within risk job insurance, construction highlights the limits of system design more clearly than many other occupations. Exposure is obvious. Consequences are physical. But responsibility is still divided administratively.

Understanding this explains why coverage gaps persist even when multiple policies exist.

These coverage gaps are a recurring feature of construction workers insurance, where multiple systems manage different risks without shared responsibility.

This same pattern appears across other high-risk occupations where exposure evolves over time rather than occurring as a single event.

Frequently Asked Questions

Why are insurance systems structured to avoid automatic coordination?

Because each policy is written to cover a specific risk and exclude others. Coordination is limited by design.

Does increasing the number of insurance policies eliminate structural coverage gaps?

Not necessarily. More policies increase complexity if responsibility boundaries are unclear.

Why do insurance systems determine responsibility before responding?

Because paying implies accepting responsibility. Insurance systems determine responsibility before responding.

Is this problem unique to construction?

No, but construction experiences it more often due to physical work, mixed duties, and unstable employment structures.

Are coverage gaps caused by mistakes?

Usually not. They result from how insurance systems are structured rather than errors by workers.

Final Note

Insurance gaps in construction are not caused by lack of coverage. They are caused by divided responsibility. Each system protects itself by narrowing its role, while construction work expands risk across boundaries those systems were never designed to bridge.

Understanding this does not eliminate the gap, but it explains why it exists and why multiple policies do not guarantee protection within construction workers insurance, a recurring pattern explored in why construction insurance breaks down in real life.