Introduction: When Coverage Exists, but Insurance No Longer Can

Uninsurable risk for high-risk workers occurs when insurance coverage can no longer continue, even though danger, exposure, and income uncertainty remain. Yet insurance no longer responds.

At this point, workers are often told that coverage has “ended,” but that explanation feels incomplete. Policies may still exist. Some benefits may still appear active. However, insurers may no longer be able to extend or continue coverage for that level of exposure.

This is the moment when risk becomes uninsurable.

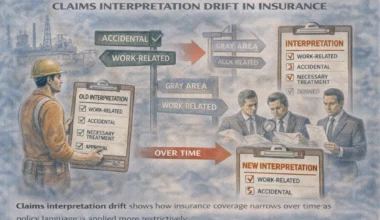

This guide explains what uninsurable risk means for high-risk workers, but it builds on a deeper idea first: insurance begins narrowing through exclusions. We explain that foundation in our main guide on insurance exclusions for high-risk jobs, which shows why coverage starts shrinking long before it fully ends.

What “Uninsurable Risk” Actually Means

This transition reflects the final boundary of the risk job insurance system, where coverage stops not because of denial, but because risk can no longer be shared.

Uninsurable risk does not mean the risk is imaginary or exaggerated.

It means the risk can no longer be:

-

Priced sustainably

-

Defined clearly

-

Limited contractually

-

Pooled safely across other insureds

Insurance only works when risk can be measured, limited, and shared. When those conditions collapse, insurance must stop, even if danger remains. This usually happens after the same stopping points described in our guide on when insurance coverage truly ends for high-risk workers, where limits, definitions, and enforcement confirm that insurance can no longer respond.

Uninsurable risk is not rejected risk. It is unmanageable risk.

For example, repeated severe injury risk, permanent loss of work capacity, or ongoing exposure that cannot be reduced.

How Risk Becomes Uninsurable for High-Risk Workers

Risk rarely becomes uninsurable overnight. It happens in stages.

1. Repeated or Severe Exposure

High-risk jobs involve:

-

Recurrent injury potential

-

Cumulative physical strain

-

Long recovery cycles

Over time, future outcomes become harder to predict and more expensive to absorb.

2. Limits and Definitions Are Exhausted

As explained earlier:

-

Policy limits cap payouts

-

Definitions narrow eligibility

-

Time-based benefits expire

Once these tools are fully used, insurance reaches the same enforcement point where coverage no longer responds.

3. Risk Can No Longer Be Pooled

Insurance relies on spreading risk across many people.

When a worker’s exposure becomes:

-

Highly individualized

-

Long-term

-

Statistically concentrated

That risk can no longer be pooled fairly without destabilizing the system.

At that point, insurance cannot extend further without breaking the structure it relies on.

This progression reflects patterns seen in global occupational injury and recovery data published by the International Labour Organization, where hazardous work shows higher severity, longer recovery, and increased lifetime exposure.

Why Insurance Cannot “Follow” Workers Indefinitely

Many workers assume insurance should adapt as circumstances change.

In reality, insurance does not evolve with worsening risk.

Insurance:

-

Does not retrain workers

-

Does not redesign careers

-

Does not absorb lifetime exposure

-

Does not replace long-term earning capacity

Once risk exceeds what contracts can control, insurance exits by design.

This is why escalation, appeals, disputes, or litigation cannot reopen coverage once risk becomes structurally uninsurable.

The Difference Between Uninsured and Uninsurable

This distinction matters.

-

Uninsured means coverage was not in place

-

Uninsurable means coverage cannot exist

High-risk workers often reach a point where:

-

Insurance was present

-

Insurance responded

-

Insurance enforced limits

-

Insurance exited

Not because of wrongdoing; but because the risk itself exceeded insurable boundaries.

This distinction explains why layered coverage exists in the first place, as outlined in why high-risk workers often need more than one insurance policy, where no single policy is designed to follow risk indefinitely.

Why This Reality Feels So Personal

Uninsurable risk feels personal because:

-

The body is involved

-

The job identity is involved

-

Income is involved

But insurance does not evaluate identity, effort, or fairness.

It evaluates:

-

Probability

-

Severity

-

Sustainability

When those fail, insurance stops; even when life does not.

How This Reality Fits Into The Broader Risk Job Insurance System.

Within the risk job insurance system:

-

Eligibility allows coverage to exist

-

Underwriting defines acceptable exposure

-

Pricing reflects volatility

-

Limits cap responsibility

-

Appeals verify enforcement

-

Disputes confirm boundaries

-

Un-insurability marks the endpoint

This is not failure. It is completion.

Reaching this point is rare, but it matters to understand, so expectations stay realistic.

What Comes After Uninsurable Risk

After insurance exits, decisions are no longer insurance decisions.

They become:

-

Job decisions

-

Capability decisions

-

Career decisions

-

Long-term risk management decisions

This is where job-specific realities replace policy language.

Why Job-Specific Guidance Begins Here

Up to now, this site has explained systems.

From here forward, guidance must change.

Because:

-

Risk differs by job

-

Physical demands differ

-

Transferable skills differ

-

Recovery outcomes differ

There is no universal answer beyond this point, only job-specific paths.

That is why job-specific insurance guidance begins after uninsurable risk is understood.

From this point forward, outcomes depend on the realities of each occupation, which is why job-specific insurance guidance follows after uninsurable risk is fully understood.

Conclusion: Insurance Stops Where Risk Can No Longer Be Shared

For high-risk workers, insurance does not fail.

It ends where risk can no longer be pooled, priced, or contained.

When risk becomes uninsurable:

-

Insurance has completed its role

-

Structure has reached its limit

-

Reality replaces policy

Understanding this moment is not discouraging. It is grounding.

From here on, protection is no longer about systems; it is about how specific jobs interact with risk over time.