Table of Contents Hide

- What Insurers Mean by “High-Risk” Occupations

- Why Job Duties Matter More Than Job Titles

- Why Standard Life Insurance Often Excludes High-Risk Jobs

- Types of Life Insurance Available to High-Risk Workers

- How Pricing, Underwriting, and Risk Classification Work

- Common Exclusions, Limitations, and Eligibility Challenges

- Employer-Provided Life Insurance vs Personally Owned Policies

- Real-World Examples Across High-Risk Jobs

- FAQs

- When This Guide May Not Fully Apply

- What to Research Next Before Making Decisions

- Final Thoughts

Life insurance for high-risk occupations works differently from standard life insurance, even though the basic concept remains the same. While many policies are designed around office-based or low-risk work environments, people employed in construction, offshore operations, mining, transport, and other hazardous industries are assessed under separate risk frameworks.

For people in high-risk occupations, however, life insurance works differently in important ways.

Construction workers, offshore personnel, miners, industrial technicians, commercial drivers, and others who work around heavy equipment, hazardous environments, or extreme conditions often discover that standard life insurance assumptions do not apply to them. Policies may cost more, come with exclusions, require deeper scrutiny, or be unavailable in certain forms altogether.

This guide is written to explain clearly, calmly, and without sales pressure, how life insurance works for high-risk workers worldwide. It is designed for beginners with little or no insurance background and avoids provider recommendations, fear-based language, or jurisdiction-specific legal advice.

By the end, you should understand why insurers consider some jobs high-risk, how underwriting decisions are made, what types of coverage may be available, and what questions to research next before making any decisions.

This approach is part of what is broadly referred to as risk job insurance explained, where insurers evaluate workplace exposure, job duties, and historical safety data rather than relying on job titles alone.

What Insurers Mean by “High-Risk” Occupations

In everyday language, a “high-risk job” usually means work that feels dangerous. In insurance, the term has a more specific meaning.

Risk from an Insurer’s Perspective

Life insurers are concerned with one core question:

How likely is it that this person will die during the policy term compared to the average population?

Occupational risk is one of several factors insurers assess to answer that question. Others include age, health history, lifestyle, and sometimes hobbies. A job is considered “high-risk” if it statistically increases the likelihood of serious injury or death. Insurers rely on historical injury and fatality data from workplace safety and labor organizations, such as occupational injury and fatality statistics published by the International Labour Organization (ILO), to assess which jobs carry higher risk over time.

This assessment is not moral or judgmental. It is actuarial based on historical data, injury rates, fatality statistics, and claims experience.

Common Categories of High-Risk Work

While exact classifications vary between insurers and countries, high-risk occupations often include:

-

Construction and demolition work

-

Offshore oil and gas operations

-

Mining and quarrying

-

Industrial manufacturing and heavy machinery operation

-

Commercial driving and transport (trucking, aviation, marine)

-

Electrical and utility work at height or under live conditions

-

Emergency response and hazardous material handling

Not every role within these industries is treated the same, which leads to an important distinction many beginners miss.

Why Job Duties Matter More Than Job Titles

One of the most common misconceptions among high-risk workers is that insurers underwrite based on job titles alone. In reality, job duties matter far more than job names.

Titles Are Vague; Duties Are Specific

Two people may share the same job title but face very different levels of risk.

For example:

-

A “construction worker” who manages materials on the ground

-

A “construction worker” who regularly works at height on scaffolding

From an insurer’s perspective, these are not equivalent risks.

This is why insurance applications often ask detailed questions such as:

-

Do you work at height? If so, how often?

-

Do you operate heavy or mobile machinery?

-

Are you exposed to explosives, confined spaces, or open water?

-

Do you work offshore, underground, or in remote locations?

Why Insurers Focus on Duties

Actuarial risk models rely on exposure, not labels. Insurers want to understand:

-

Frequency of exposure (occasionally vs daily)

-

Environment (controlled site vs remote or offshore)

-

Severity potential (minor injury vs catastrophic risk)

-

Emergency access (immediate medical help vs delayed evacuation)

This approach explains why two people in the same industry can receive very different underwriting outcomes.

Why Standard Life Insurance Often Excludes High-Risk Jobs

Many workers assume that if life insurance is advertised as “standard” or “basic,” it should apply to everyone. In practice, standard policies are often designed around average-risk populations.

How Standard Policies Are Designed

Most retail life insurance products are priced assuming:

-

Stable working environments

-

Low occupational fatality rates

-

Predictable long-term risk patterns

High-risk occupations disrupt these assumptions. As a result, insurers may respond in several ways.

Common Outcomes for High-Risk Applicants

High-risk workers may encounter:

-

Higher premiums than average-risk workers

-

Coverage with occupational exclusions

-

Reduced policy limits

-

Longer underwriting processes

-

Declines for certain policy types

This does not mean life insurance is “unavailable,” but it does mean it often looks different than marketing brochures suggest.

Types of Life Insurance Available to High-Risk Workers

Understanding policy types helps clarify why outcomes differ between workers.

Term Life Insurance

Term life insurance provides coverage for a fixed period (for example, 10, 20, or 30 years).

How it works for high-risk workers:

-

Often the most accessible option

-

Premiums reflect occupational risk

-

May include exclusions related to specific duties

-

Coverage ends at the end of the term

Term life is commonly used to cover temporary financial responsibilities, such as dependents or debts.

Permanent Life Insurance (Whole or Universal)

Permanent policies are designed to last a lifetime and may include savings or investment components.

How it works for high-risk workers:

-

Often harder to qualify for

-

Underwriting is usually stricter

-

Higher costs due to long-term exposure

-

Some roles may be declined entirely

Because insurers commit to lifetime coverage, occupational risk weighs more heavily.

Accident-Focused Coverage (Clarification Only)

Some workers encounter products that emphasize accidental death. These are not replacements for life insurance and often come with narrow definitions and exclusions.

This guide focuses on life insurance as traditionally defined, not supplemental accident products.

How Pricing, Underwriting, and Risk Classification Work

For high-risk workers, understanding underwriting removes much of the confusion around pricing differences.

Step 1: Application and Disclosure

Applicants typically provide:

-

Personal details (age, location)

-

Health information

-

Occupational duties and environment

Accuracy matters. Misstating duties can lead to denied claims later, even if the policy is issued.

Step 2: Risk Classification

Insurers assign a risk class based on combined factors. Occupational risk may:

-

Shift the applicant into a higher premium class

-

Trigger exclusions for specific activities

-

Require additional documentation or clarification

This is not a punishment. It reflects statistical likelihood.

Step 3: Pricing

Premiums are calculated using:

-

Mortality tables

-

Historical claims data

-

Occupational risk multipliers

This is why premiums can vary widely even between workers in similar industries.

Common Exclusions, Limitations, and Eligibility Challenges

High-risk workers should pay close attention to exclusions, as they often define the real limits of coverage.

Occupational Exclusions

Some policies exclude death resulting directly from specific duties, such as:

-

Working at extreme heights

-

Offshore platform operations

-

Underground mining

In these cases, death outside excluded activities may still be covered.

Geographic or Environmental Limitations

Certain policies limit coverage in:

-

Remote or undeveloped regions

-

Offshore or international waters

-

Conflict or war-adjacent zones

These limitations are particularly relevant for mobile or rotational workers.

Eligibility Constraints

Some roles may face:

-

Age-based restrictions combined with occupation

-

Maximum coverage limits lower than average

-

Requirement to change duties to qualify

These constraints vary widely by insurer and jurisdiction.

Employer-Provided Life Insurance vs Personally Owned Policies

Many high-risk workers first encounter life insurance through their employer. Understanding how employer-provided coverage differs from personally owned policies is a core part of how risk job insurance works for people in high-risk occupations.

Employer-Provided Coverage

Key characteristics:

-

Often group-based

-

Lower or no individual underwriting

-

Coverage tied to employment

-

Limited payout amounts

Employer policies may not fully reflect individual risk, but they usually end when employment ends.

Personally Owned Policies

Key characteristics:

-

Individually underwritten

-

Portable across jobs

-

More customizable

-

Subject to occupational scrutiny

For high-risk workers, the trade-off is often between convenience and long-term control.

Real-World Examples Across High-Risk Jobs

Examples help clarify how theory translates into practice.

Construction Worker at Height

A worker who regularly works on scaffolding may:

-

Face higher premiums

-

Encounter height-related exclusions

-

Be eligible for term coverage with limitations

A supervisor who rarely works at height may receive different terms.

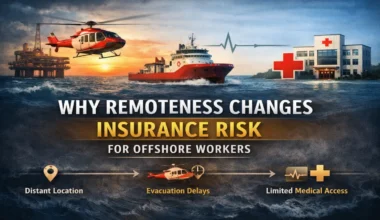

Offshore Oil and Gas Worker

Offshore workers may encounter:

-

Geographic exclusions

-

Additional scrutiny due to evacuation delays

-

Differing treatment based on rotation schedules and roles

Administrative offshore roles are often assessed differently from hands-on operational roles.

Mining and Underground Work

Mining roles often involve:

-

Confined spaces

-

Heavy machinery

-

Delayed emergency response

These factors commonly increase underwriting scrutiny and limit permanent policy options.

Commercial Transport and Industrial Work

Long-haul drivers, crane operators, and industrial technicians may see:

-

Duty-based differentiation

-

Emphasis on accident statistics

-

Premium variation based on equipment and environment

FAQs

How do insurers classify high-risk work?

Insurers use historical data, injury and fatality statistics, and duty-specific exposure analysis. Classification focuses on what you do, where you do it, and how often, not just job titles.

Why do premiums vary so widely for similar jobs?

Premium differences often reflect:

-

Specific duties

-

Frequency of hazardous exposure

-

Work environment

-

Policy type and duration

Two people in the same industry can legitimately receive very different quotes.

What happens if my job duties change?

Duty changes may:

-

Reduce risk and improve terms

-

Increase risk and trigger policy review

-

Require disclosure to maintain claim validity

Failing to disclose material changes can cause problems later.

Does this guide apply everywhere?

This guide is jurisdiction-neutral and educational. Local laws, regulations, tax treatment, and insurer practices vary by country and region. Military combat roles, extreme-risk assignments, and conflict zones often follow separate rules not fully covered here.

When This Guide May Not Fully Apply

Some situations fall outside standard civilian underwriting frameworks, including:

-

Active military combat deployments

-

Private security work in conflict zones

-

Experimental or unregulated industrial roles

-

Short-term emergency disaster response assignments

In these cases, specialized rules or exclusions often apply.

What to Research Next Before Making Decisions

Before pursuing coverage, high-risk workers benefit from understanding:

-

Their exact job duty classification

-

Whether exclusions apply to their daily work

-

How portable coverage is if roles change

-

What documentation insurers typically require

Life insurance for high-risk occupations is not about finding loopholes or shortcuts. It is about understanding how risk is measured and how coverage structures respond to it.

Final Thoughts

High-risk work is essential to modern economies, yet it rarely fits neatly into standard insurance models. Life insurance for high-risk occupations is neither impossible nor uniform; it is nuanced.

When approached with clear expectations and accurate information, high-risk workers can understand:

-

Why their occupation is treated differently

-

How insurers assess and price risk

-

What forms of coverage may exist

-

Which questions matter most before moving forward

Education, not urgency, is the foundation of good insurance decisions.