Introduction

Workers’ compensation exists to manage workplace injury risk, but in high-risk occupations—construction, offshore work, logging, mining, trucking—the system operates under much stricter assumptions about injury frequency, severity, and cost.

For high-risk workers, workers’ compensation is not comprehensive income protection. It is a narrowly defined system designed to cover medical care and partial wage loss for work-related injuries, while limiting employer liability.

This guide explains how workers’ compensation functions for high-risk jobs, where coverage expands, where it breaks down, and why exclusions and denied claims are more common in dangerous work.

For a system-level explanation of how workers’ compensation operates differently in dangerous jobs, and why its protections are limited, see how workers’ Compensation works for High-Risk jobs.

Workers’ compensation provides structured access to benefits, but it does not guarantee full income protection or automatic claim approval in high-risk occupations.

Explore This Topic Further

To fully understand how workers’ compensation insurance for high-risk workers operates, these in-depth guides break down the key components of the system:

- How Workers’ Compensation Works for High-Risk Jobs — system structure, claim validation, and decision logic

- How Workers’ Compensation Premiums Are Calculated — payroll, classification rates, and EMR explained

- Occupational Risk Class Codes Explained — how insurers assign and price job risk

- Workers’ Comp vs Disability Insurance for Hazardous Workers — key differences in coverage and payout structure

Evidence block

For updated data and injury trends, see the official: BLS workplace injury statistics, which provide detailed reports on fatal and non-fatal incidents across high-risk occupations.

This is why high-risk industries require specialized workers’ comp policies. Policies designed to accommodate higher risk class codes, stricter safety regulations, and elevated claims exposure.

Before we go deeper, it’s recommended that readers who need a foundational understanding of risk-heavy occupations read our supporting post “Risk Job Insurance Explained.”

How Workers’ Compensation Insurance for High-Risk Workers Actually Works (System Overview)

Workers’ compensation for high-risk workers operates through a structured system that connects risk classification, underwriting, and claim validation.

At a high level, the system follows three stages:

1. Risk Classification

Jobs are assigned risk class codes based on duties and hazard exposure.

2. Underwriting and Pricing

Insurers calculate premiums using payroll, classification rate, and experience modification rate (EMR).

3. Claim Validation

When an injury occurs, the claim is evaluated based on causation, classification accuracy, and safety compliance.

Failure at any stage can lead to increased costs, disputes, or claim denial.

This system structure explains why high-risk jobs face higher premiums and stricter claim scrutiny.

What Workers’ Compensation Is Designed to Do, and What It Is Not

Workers’ compensation is not designed to replace long-term earning capacity or protect against non-occupational injuries, limitations that become more visible in physically demanding jobs.

Core Purposes of Workers’ Compensation Insurance

-

Financial protection for injured workers

Covers medical expenses, lost income, rehabilitation therapy, and long-term disability. -

Legal protection for employers

Shields employers from lawsuits by providing employer liability coverage. -

Safety improvement incentive

Encourages businesses to comply with OSHA regulations and reduce workplace injuries.

How Workers’ Comp Differs for High-Risk Jobs

High-risk occupations deal with:

-

Increased accident exposure

-

Higher severity of injuries

-

More frequent claims

-

Specialized equipment risks

-

Hazardous work environments (e.g., heights, chemicals, explosives)

Because of these factors, insurance carriers distinguish between medical risk and occupational risk when underwriting workers’ compensation policies for high-risk jobs.

Why High-Risk Workers Need Specialized Workers’ Compensation Insurance

High-risk workers face significantly higher injury frequency and severity, which increases both claim costs and the likelihood of long-term disability. This elevated exposure creates what insurers classify as “catastrophic loss potential,” where a single incident can result in extended medical treatment, permanent impairment, or death.

Understanding Hazard Exposure

High-risk jobs tend to include:

-

Working at heights (roofers, tower climbers)

-

Burn risk (welders, refinery laborers)

-

Exposure to toxic chemicals (manufacturing, oil & gas)

-

Heavy machinery operation (construction, mining)

-

Remote and offshore locations (offshore drilling, fishing)

-

Long-hour driving and road hazards (commercial truckers)

These conditions increase the probability of:

-

Spinal injuries

-

Crush injuries

-

Traumatic brain injuries

-

Respiratory illnesses

-

Amputations

-

Permanent disability

This is where workers’ comp benefits become vital. Medical, disability, and wage replacement benefits help workers recover without financial hardship.

Industries Classified as High-Risk by NCCI

NCCI identifies certain occupations as “maximum risk” due to claim frequency and severity, such as:

-

Construction

-

Logging

-

Roofing

-

Commercial trucking

-

Mining

-

Oil and gas extraction

-

Offshore operations: Offshore and maritime workers may fall outside standard state workers’ compensation systems and instead be governed by separate federal frameworks.

-

Industrial manufacturing

Each industry receives its own risk class code, which directly affects premium costs.

Eligibility Requirements for Workers’ Compensation Insurance for High-Risk Workers

High-risk industries must follow strict eligibility criteria before employees qualify for Workers’ Compensation Insurance for High-Risk Workers. Eligibility varies by state, but several universal requirements apply.

Who Qualifies as a High-Risk Worker?

A worker is considered “high-risk” if their job involves:

-

Working at heights (roofers, tower climbers)

-

Operating heavy machinery (construction workers, miners)

-

Handling hazardous chemicals (oil & gas, manufacturing)

-

Driving long distances (truck drivers)

-

Offshore or remote operations (offshore oil workers, seafarers)

-

High physical or environmental hazards (loggers, welders)

These workers fall into NCCI high-risk class codes, which increases both coverage requirements and workers’ comp premium rates.

Employee vs. Independent Contractor Eligibility

Workers’ compensation laws generally cover employees, not independent contractors. However:

-

Some states require coverage for contractors in construction.

-

Some companies misclassify workers, leading to claim denial or regulatory penalties.

Risk job insurance classification guide

Misclassification is common in high-risk industries and often results from misunderstanding how insurers and regulators apply occupational risk classification based on job duties rather than titles.

Subcontractors in High-Risk Jobs

Subcontractors in roofing, construction, or oil & gas often must carry their own workers’ comp. Failure to do so results in:

-

The general contractor being held liable

-

Higher premium rates for the employer

-

Potential state fines

Some states legally mandate that subcontractors show proof of workers’ comp before entering a worksite.

NCCI Class Codes & Risk Classification Requirements

Insurance carriers use NCCI class codes to determine job risk and premium levels. High-risk jobs receive codes with higher rates.

Examples:

-

0042 Logging (very high risk)

-

0106 Tree pruning

-

5474 Painting, steel structures

-

6217 Excavation work

-

7228 Long-haul trucking

For more details on how risk classification affects premium rates, review the NCCI classification guide.

State-Specific Eligibility Rules

Some states require workers’ comp for any business with 1 employee, while others require it only for 4+ employees.

Monopolistic states (Ohio, Wyoming, Washington, North Dakota) require purchasing from state-run funds.

How Insurers Evaluate High-Risk Workers’ Compensation Policies

Workers’ compensation insurance for high-risk workers is not priced or managed randomly. Insurers evaluate employer risk using a structured underwriting framework that determines coverage cost, eligibility conditions, and claim scrutiny levels.

At a system level, this evaluation focuses on five core factors:

1. Classification Accuracy

Insurers assess whether job roles are correctly assigned to risk class codes based on actual duties and exposure. In high-risk industries, even small classification errors can significantly affect premium pricing and claim outcomes.

2. Payroll Exposure

Total payroll determines the scale of risk. Higher payroll in hazardous roles increases the insurer’s potential liability and directly impacts premium calculations.

3. Claims History

Past claims are used to predict future risk. Frequent or severe claims signal higher exposure and lead to stricter underwriting conditions.

4. Experience Modification Rate (EMR)

The EMR reflects how a company’s claims history compares to industry averages:

- EMR below 1.0 → lower-than-average risk

- EMR above 1.0 → higher-than-average risk

This factor directly increases or reduces premium costs.

5. Safety and Compliance Systems

Insurers evaluate whether employers enforce safety protocols, training, and reporting procedures. Weak compliance increases both claim frequency and the likelihood of disputes.

Underwriting Insight

In workers’ compensation for high-risk jobs, underwriting determines how risk is priced and monitored, but claim validation ultimately determines whether that risk results in a payout.

What Workers’ Compensation Insurance for High-Risk Workers Covers

Coverage under Workers’ Compensation Insurance for High-Risk Workers is more comprehensive than standard workers’ comp policies due to elevated accident potential.

The following benefits provide financial protection to workers while also shielding employers from liability.

Medical Benefits & Emergency Care Coverage

Workers’ comp pays for all medical treatment related to a workplace injury, including:

-

Emergency room transport

-

Surgery and hospitalization

-

Specialist care

-

Occupational therapy

-

Prescription medications

-

Diagnostic imaging (X-ray, MRI, CT)

-

Long-term rehabilitation

High-risk workers suffer more severe injuries (fractures, burns, amputations), resulting in significantly higher medical claims.

Employers must adhere to workplace health requirements outlined in the OSHA medical treatment guidelines.

Lost Wages & Temporary Disability Benefits

If a worker cannot perform their job after an accident, they receive temporary total disability (TTD) or temporary partial disability (TPD) benefits.

Most states pay two-thirds of the worker’s average weekly wage, up to the state’s maximum benefit limit.

Common high-risk injuries that trigger wage replacement:

-

Back injuries

-

Crush injuries

-

Traumatic brain injuries

-

Burns

-

Falls from height

This ensures the worker maintains financial stability during recovery.

Permanent Disability Benefits

If the injury results in a permanent impairment, the worker may receive:

-

Permanent Partial Disability (PPD)

-

Permanent Total Disability (PTD)

This may include lifetime wage replacement.

High-risk industries (logging, mining, offshore) have the highest percentage of permanent disability claims.

For broader income protection beyond workers’ comp, workers should also consider disability insurance for high-risk workers, which covers non-work-related injuries as well.

Death Benefits for Families

If a worker dies on the job, workers’ compensation provides:

-

Funeral expense coverage

-

Weekly income to surviving dependents

-

Long-term financial support for children

High-risk industries consistently show elevated injury frequency and severity, which directly results in stricter classification enforcement, higher premium ranges, and more aggressive claim validation thresholds.

Employer Liability Protection (Legal Defense Coverage)

Workers’ compensation protects employers against lawsuits by injured employees.

This coverage includes:

-

Attorney fees

-

Court costs

-

Settlements

-

Employer negligence claims (with exceptions)

This is essential for high-risk industries where litigation risks are higher.

What Workers’ Compensation Insurance for High-Risk Workers Does Not Cover

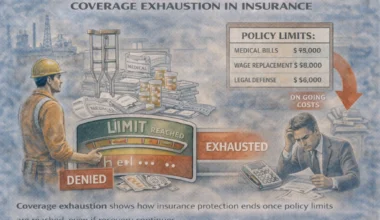

In high-risk jobs, denied claims are not rare exceptions; they are a structural feature of how workers’ compensation limits exposure.

Even though Workers’ Compensation Insurance for High-Risk Workers provides broad protection, it does not cover every situation. Knowing these exclusions helps workers avoid claim denial and helps employers ensure compliance.

Below are the common exclusions across almost all U.S. states.

Injuries Not Related to Work Activities

Workers’ comp only covers injuries that occur because of work or within the course of employment.

The following are not covered:

-

Injuries happening during personal time or lunch breaks

-

Injuries at home (for remote workers without clear employer direction)

-

Commuting accidents (unless the employee is a driver, trucker, or transport worker)

Injuries Caused by Substance Abuse or Intoxication

If a worker is under the influence of drugs or alcohol and this directly contributes to an accident, the claim is typically denied.

Employers often conduct post-accident drug testing to protect their employer liability exposure.

Injuries Resulting from Violating Company Policies

If a worker ignores safety procedures (removing PPE, bypassing lockout/tag-out, operating unauthorized machinery), the insurer may deny the claim.

Intentional Self-Inflicted Injuries

Workers’ comp does not cover injuries caused intentionally by the worker, including attempts to create a claim or fraud.

Non-Work-Related Illnesses or Pre-Existing Conditions

Pre-existing conditions are not covered unless the job aggravates the condition.

Example:

-

A miner with previous breathing issues may qualify if workplace dust worsens the condition.

-

A construction worker with a past back injury won’t qualify unless work activity caused aggravation.

For income protection outside workplace injuries, employees should consider Disability Insurance for High-Risk Workers, which covers non-work-related accidents and illnesses.

Why Workers’ Compensation Breaks Down in High-Risk Jobs

Workers’ compensation does not fail randomly; it breaks down at predictable points:

Single failure:

– Minor disputes or delays

Dual failure:

– High likelihood of claim investigation

Triple failure:

– Claim denial or reduced payout

Common failure combinations:

– Misclassification + safety violation

– Late reporting + inconsistent documentation

– Contractor status dispute + lack of job duty proof

These failure patterns become most visible during the claims process, where validation determines whether benefits are approved or denied.

Step-by-Step Workers’ Compensation Claims Process for High-Risk Workers

The claims process below explains how workers’ compensation functions administratively in high-risk claims, not how to maximize outcomes.

High-risk industries experience a higher volume of claims, and the process tends to be more complex due to severe injury types, longer treatment durations, and multiple parties involved (employers, insurers, medical providers, safety inspectors, etc.).

Understanding the Workers’ Compensation Insurance for High-Risk Workers claims process is essential for ensuring timely approvals and avoiding disputes.

Here is a clear step-by-step breakdown.

Step 1 – Report the Injury Immediately

Workers must notify their employer as soon as the injury occurs or as soon as they become aware of a work-related illness.

Typical state deadlines:

-

Most states: 24-48 hours

-

Some states allow up to 7-30 days

High-risk jobs (roofing, mining, trucking, oil & gas) often require same-day reporting because delayed reporting increases suspicion of claim fraud.

Key details the worker must report:

-

What happened

-

How the injury occurred

-

Location, date, and time

-

Whether equipment was involved

-

Witnesses present

Step 2 – Employer Files the Official Claim Form

After receiving notice, the employer must complete and submit a First Report of Injury (FROI) to their workers’ compensation insurer and, in some cases, to the state board.

Employer responsibilities include:

-

Completing required paperwork

-

Providing workers with claim documents

-

Reporting to the insurer on time

-

Ensuring the injured worker receives medical evaluation.

To understand broader employer responsibilities in hazardous industries, see our guide on Risk Job Insurance Explained.

Step 3 – Worker Receives Medical Evaluation

The medical assessment determines:

-

Injury severity

-

Treatment needed

-

Time off work

-

Whether the injury causes temporary or permanent disability

Some states allow workers to choose their doctor; others require using an employer-approved provider.

Step 4 – Insurer Reviews and Investigates the Claim

The insurance carrier will:

-

Review the injury details

-

Interview the worker

-

Speak with supervisors

-

Evaluate medical records

-

Assess workplace conditions

High-risk industries undergo deeper investigation because:

-

Injury costs are higher

-

There is a higher chance of long-term disability

-

Employer liability exposure is greater

For more information on how state agencies monitor claim filing and investigation, refer to the State Workers’ Compensation Board directory

Step 5 – Claim Approval or Denial

If Approved:

Worker receives:

-

Medical treatment coverage

-

Lost wage benefits

-

Temporary or permanent disability payments

If Denied:

Reasons may include:

-

Late reporting

-

Inconsistent injury statements

-

Lack of medical evidence

-

Employer disputes the injury

-

Non-work-related cause

A denied claim can be appealed through the state board workers’ compensation appeals process

Step 6 – Returning to Work or Modified Duty

If the doctor approves, the worker may return to:

-

Regular duty

-

Modified or light-duty

-

Gradual return-to-work programs

High-risk industries rely heavily on modified duty to reduce lost wage payments and lower long-term claim costs.

Step 7 – Claim Closure or Long-Term Benefits

Claim closes when:

-

Worker fully recovers

-

Benefits reach maximum medical improvement (MMI)

-

Disability classification is determined

For severe injuries: amputations, spinal injuries, catastrophic burns, the worker may receive lifetime benefits.

Why Workers’ Compensation Costs Escalate in High-Risk Jobs

The cost of Workers’ Compensation Insurance for High-Risk Workers is significantly higher than standard occupations, primarily because claim frequency and claim severity are dramatically elevated in dangerous jobs.

Workers’ compensation cost depends heavily on:

-

The nature of the job

-

Risk class code

-

Injury history

-

State requirements

-

Payroll size

Let’s break down the core cost factors.

Key Factors That Influence Workers’ Compensation Premium Rates

Workers’ comp premiums are calculated using:

1. Risk Class Codes (NCCI Codes)

Every job has a classification code. High-risk codes — such as logging (0042), roofing (5551), or trucking (7228) carry the highest costs.

You can explore all industry codes in the NCCI workers’ compensation classification codes directory.

2. The Experience Modification Rate (EMR)

This number reflects an employer’s injury history.

-

EMR of 1.0 = average risk

-

EMR above 1.0 = higher premiums

-

EMR below 1.0 = premium discounts

High-risk industries often see EMRs between 1.2 and 1.8, depending on claims.

3. Payroll Size

Premiums are based partly on payroll:

Higher payroll = higher exposure = higher premium.

High-risk industries like construction and oil & gas typically have large crews, increasing costs.

4. State Workers’ Comp Laws

State rules significantly impact pricing.

Examples:

-

Texas: allows employers to opt out (non-subscription).

-

California: highest average premium rates due to injury frequency.

-

Florida: strict rules for construction worker coverage.

-

Monopolistic states: only the state fund can provide workers’ comp.

For more on state workers’ compensation agencies.

Average Workers’ Compensation Costs by High-Risk Industry

Average premium costs (national estimates):

| High-Risk Industry | Average Rate (per $100 payroll) |

|---|---|

| Logging | $22-$35 |

| Roofing | $15-$25 |

| Trucking (long-haul) | $10-$18 |

| Construction | $7-$14 |

| Oil & Gas | $9-$20 |

| Mining | $8-$16 |

These rates vary by state, EMR, and claim severity.

How Employers Can Reduce Workers’ Compensation Costs

Even high-risk industries can lower premium rates using risk reduction strategies.

1. Implement OSHA-Compliant Safety Programs

Fewer injuries = lower EMR = cheaper premiums.

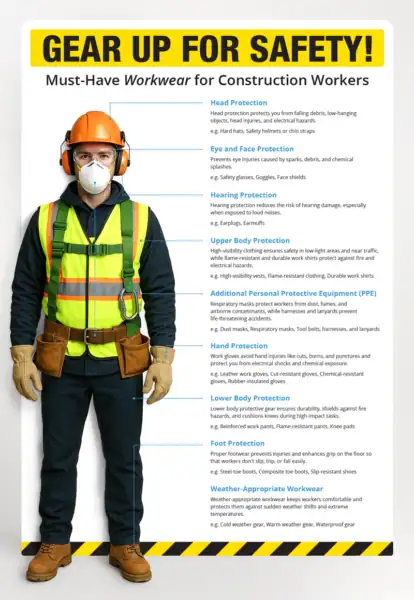

2. Provide Better Training & PPE Compliance

Fall protection, hazard communication, lockout/tag-out, these reduce major accidents.

3. Use Return-to-Work Programs

Allows injured workers to perform light-duty tasks, reducing wage replacement costs.

4. Conduct Safety Audits & Risk Assessments

Prevents recurring accidents that increase premiums.

Cost Example Scenario (Real-Life Case)

Scenario: Roofing Company With 12 Employees

-

Payroll: $600,000

-

Risk class code rate: $18 per $100 payroll

-

EMR: 1.3 (above average due to past accidents)

Premium calculation:

$600,000 ÷ 100 = 6,000

6,000 × $18 = $108,000

$108,000 × 1.3 EMR = $140,400 annual premium

This demonstrates how costly high-risk occupations can be and why safety improvements matter.

In high-risk industries, premium volatility is driven more by claims frequency and severity trends than by base classification rates alone.

Common Workers’ Compensation Claims Mistakes and How to Avoid Them

High-risk workers are more vulnerable to claim disputes because their injuries are costly and insurers scrutinize them heavily. Preventing mistakes can mean the difference between approval and denial.

Claim denials in high-risk jobs often occur not because injuries are invalid, but because coverage rules break down under classification, reporting, or eligibility constraints.

Below are the most common errors and how to avoid them.

Mistake 1 – Delayed Injury Reporting

Delays raise red flags for insurance carriers and often lead to denial.

How to avoid it:

Report injuries immediately, even if symptoms seem minor.

Small injuries can become major medical issues later.

Mistake 2 – Incomplete or Inaccurate Paperwork

Missing forms or incomplete accident descriptions are common issues.

How to avoid it:

-

Double-check forms

-

Provide detailed statements

-

Keep copies of everything submitted

Employers should ensure workers receive guidance on necessary documentation.

Mistake 3 – Failing to Follow Medical Treatment Plans

If the worker skips appointments or ignores treatment advice, insurers may argue the worker is non-compliant.

How to avoid it:

-

Attend all appointments

-

Follow doctor instructions

-

Keep medical receipts and reports

Mistake 4 – Not Reporting All Symptoms or Secondary Injuries

Workers often report the primary injury but fail to mention:

-

Radiating pain

-

Numbness

-

Headaches

-

Mental stress

-

Secondary injuries

How to avoid it:

Always give doctors a complete list of symptoms.

Mistake 5 – Giving Inconsistent Statements

Any inconsistencies between:

-

Worker report

-

Employer report

-

Witness statements

-

Medical examiner notes

…can trigger a denial.

How to avoid it:

Provide a clear, consistent account from the start.

Mistake 6 – Not Understanding Coverage Limits

Some workers assume workers’ comp covers all losses, but exclusions apply.

To understand what injuries and situations fall outside workers’ comp, review our guide on Disability Insurance for High-Risk Workers, which fills coverage gaps.

Mistake 7 – Accepting a Denial Without Appealing

Thousands of legitimate claims are denied annually because workers believe the insurer has the final say.

How to avoid it:

-

File an appeal

-

Provide additional medical evidence

-

Request an administrative hearing

Mistake 8 – Employers Misclassifying Workers

This is very common in construction, trucking, and offshore industries.

Misclassification results in:

-

Denied claims

-

Fines

-

Higher premiums for employers

How to avoid it:

Ensure job descriptions, class codes, and employment status match the worker’s actual duties.

State-by-State Differences in Workers’ Compensation Insurance for High-Risk Workers

Workers’ compensation laws are determined at the state level, not the federal level. This means the rules governing benefits, claim deadlines, employer requirements, and cost structures vary dramatically depending on where the business operates.

For high-risk industries such as construction, trucking, offshore operations, mining, and oil & gas, these differences can significantly impact workers’ compensation costs, eligibility, and coverage.

Understanding these variations is essential for compliance and ensuring adequate protection.

Benefit Amounts and Wage Replacement Vary by State

States determine:

-

Maximum weekly wage replacement

-

Waiting periods before benefits begin

-

Maximum number of weeks a worker can receive payments

-

The formula used to calculate wage loss

Example:

-

California: One of the highest benefit caps due to high living costs

-

Florida: Lower caps and specific high-risk industry restrictions

-

Texas: Unique “non-subscription system,” where some employers may opt out.

You can review current rules for each state through the State Workers’ Compensation Agency directory.

Waiting Period Before Benefits Begin

Each state has a defined “waiting period,” typically 3 to 7 days, before temporary disability benefits begin.

If the worker remains disabled beyond a certain number of days (e.g., 14 days), the waiting period may be reimbursed.

Examples:

-

Georgia: 7-day waiting period

-

New York: 7 days

-

Texas: 7 days

-

California: 3 days

This greatly affects high-risk workers who often sustain severe injuries requiring immediate wage replacement.

Employer Penalties for Non-Compliance

States enforce strict penalties for employers who fail to carry workers’ comp insurance. Penalties may include:

-

Heavy fines

-

Business closure

-

Criminal charges (in some states)

-

Loss of contracts (especially in construction)

-

Civil liability lawsuits

High-risk industries face heightened enforcement because safety risks are elevated.

Monopolistic vs. Competitive States

Only four U.S. states require businesses to buy workers’ comp directly from the state fund:

-

Ohio

-

North Dakota

-

Wyoming

-

Washington

These are called monopolistic states.

All other states allow employers to buy coverage from private insurers, known as competitive states.

High-risk industries in monopolistic states often face higher cost but greater claim support, whereas competitive markets offer more flexibility and carrier options.

State Differences for High-Risk Industries

States regulate certain industries more aggressively:

-

Construction (mandatory coverage in nearly all states)

-

Roofing (risk classification surcharges)

-

Oil & Gas (special reporting rules)

-

Mining (federal + state regulations combined)

-

Trucking (multi-state coverage complexities)

-

Offshore work (overlap with federal maritime laws).

This makes compliance more challenging for employers operating in multiple jurisdictions.

Workers’ Rights & Employer Responsibilities Under Workers’ Compensation Insurance for High-Risk Workers

Workers’ compensation is a mutual protection system:

-

Workers receive guaranteed medical care and wage replacement.

-

Employers receive legal protection from injury lawsuits.

For the system to function correctly, both workers and employers must understand their rights and obligations.

Workers’ Rights Under Workers’ Compensation Insurance

High-risk workers have several important rights, which cannot be waived or removed by employer policy.

1. The Right to Medical Treatment at No Cost to the Worker

Workers must receive:

-

Emergency care

-

Diagnostic tests

-

Surgery

-

Medication

-

Rehabilitation

All covered by the employer’s workers’ comp insurance.

2. The Right to Wage Replacement

Workers unable to perform duties are entitled to:

-

Temporary disability benefits

-

Permanent disability benefits (if applicable)

Most states pay two-thirds of the worker’s average weekly wage.

3. The Right to File a Claim Without Retaliation

It is illegal for an employer to punish or fire a worker for reporting a workplace injury.

Forms of retaliation include:

-

Termination

-

Reduced hours

-

Threats or intimidation

-

Demotion

4. The Right to Dispute a Denied Claim

If the insurance carrier denies a claim, workers may:

-

File an appeal

-

Request a hearing

-

Submit additional medical evidence

-

Hire legal representation

This ensures fairness in the claims process.

Employer Responsibilities Under Workers’ Compensation Laws

Employers, particularly in hazardous industries, must comply with strict rules to protect workers and avoid penalties.

Below are the key obligations.

1. Provide Workers’ Compensation Coverage

All high-risk employers must carry workers’ comp unless operating in an opt-out state like Texas.

Failing to carry insurance can result in:

-

Civil penalties

-

Criminal penalties

-

Business shutdown

-

Liability lawsuits

2. Maintain a Safe Workplace

This includes:

-

Following OSHA standards

-

Conducting safety meetings

-

Providing PPE

-

Training employees on hazards

-

Maintaining equipment

High-risk industries require extensive safety documentation.

3. Report Injuries Promptly

Employers must:

-

Document incidents

-

File the First Report of Injury

-

Notify the insurer

-

Provide workers with claim forms

Delayed reporting increases claim disputes.

4. Cooperate With the Claims Investigation

Employers must:

-

Provide worker statements

-

Supply training records

-

Share safety logs

-

Allow access to workplace sites

Lack of cooperation can increase employer liability.

5. Support Return-to-Work Programs

Employers should provide:

-

Modified duty

-

Transitional jobs

-

Reduced physical tasks

This lowers workers’ compensation cost and improves recovery outcomes.

To explore additional insurance protections that support high-risk workers and employers, read our in-depth guide on Risk Job Insurance Explained.

How Employers Should Evaluate Workers’ Compensation Insurance Providers

Insurance carriers apply stricter evaluation criteria when underwriting workers’ compensation policies for high-risk employers. These evaluations focus on exposure severity, claims history, safety controls, and regulatory compliance rather than consumer preference or pricing alone.

A poor-quality policy can lead to:

-

Delayed claim processing

-

Limited benefit payouts

-

Higher long-term premiums

-

Legal disputes

-

Non-compliance penalties

Below are the essential factors employers must evaluate.

Assess the Insurance Carrier’s Expertise in High-Risk Industries

Not all insurance companies understand the unique risks associated with:

-

Construction

-

Offshore oil & gas operations

-

Mining

-

Logging

-

Trucking

-

Roofing

-

Industrial manufacturing

When evaluating a carrier, employers should ask:

-

Do you provide specialized workers’ comp coverage for high-risk industries?

-

What is your loss-handling experience?

-

How long have you underwritten hazardous jobs insurance?

Tip:

Specialized carriers often offer custom pricing, risk control consultants, and improved claims support.

Evaluate the Strength of the Claims Support System

The quality of claims management determines whether injured workers receive timely benefits and whether the employer’s EMR remains low.

Employers should look for:

-

Dedicated high-risk claims specialists

-

24/7 injury reporting

-

Clear communication protocols

-

Medical case managers

-

Robust appeals support

A strong claims system minimizes disputes and reduces future costs.

Review Policy Exclusions and Optional Coverages

High-risk employers often require extended protections.

Make sure the policy doesn’t exclude critical hazards such as:

-

Working at heights

-

Use of explosives

-

Remote operations

-

Heavy machinery use

-

Offshore travel

-

Hazmat exposure

Optional endorsements may include:

-

Employer liability extensions

-

Occupational accident coverage

-

Stop-gap coverage (monopolistic states)

Compare Premium Rates and Safety Program Discounts

Premiums vary substantially between carriers.

When comparing quotes, consider:

-

Cost per $100 payroll

-

Experience modification rate (EMR) impact

-

Industry risk rating

-

Safety credit eligibility

Carriers often give premium discounts for:

-

OSHA-compliant safety programs

-

Training certifications

-

Equipment maintenance logs

-

Return-to-work programs

Confirm the Carrier’s Understanding of State Law Variations

Since workers’ compensation regulations differ by state, your insurer must be competent in:

-

Multistate trucking rules

-

Construction-specific mandates

-

Mining and oil & gas regulatory overlaps

-

Monopolistic state requirements

-

Offshore and maritime classifications

Carriers lacking state-specific experience may mishandle claims or misclassify workers.

Assess Financial Strength & Industry Ratings

Before selecting a carrier, employers should verify:

-

AM Best rating

-

NAIC reports

-

Financial stability

-

Claim payout trends

Employers can review insurer financial reliability using the NAIC company search tool.

Industry-Specific Workers’ Compensation Guides for High-Risk Workers

Each high-risk industry comes with unique injury risks and regulatory requirements. Below is a breakdown of workers’ compensation needs for the most hazardous jobs in the U.S.

Workers’ Compensation for Construction Workers

Construction has one of the highest injury rates due to:

-

Falls from height

-

Scaffolding incidents

-

Heavy machinery accidents

-

Electrical hazards

-

Falling objects

Common claims include fractures, back injuries, amputations, and traumatic brain injuries.

Special considerations:

-

Strict OSHA compliance

-

Class codes like 5403, 5515, 5221

-

Higher EMR impact

-

Mandatory coverage in nearly all states

Workers’ Compensation for Offshore Workers

Offshore work is among the most dangerous occupations. Risks include:

-

Explosions

-

Fires

-

Vessel accidents

-

Slip hazards

-

Hazardous gases

-

Heavy lifting in unstable environments

Offshore workers may be covered under:

-

State workers’ comp

-

The Longshore and Harbor Workers’ Compensation Act (LHWCA)

-

Jones Act (for seafarers)

Offshore employees may also need additional protection such as Life Insurance for Offshore Workers, which complements workers’ comp coverage.

Workers’ Compensation for Truck Drivers

Truckers face unique risks such as:

-

Road accidents

-

Fatigue-related injuries

-

Loading/unloading accidents

-

Weather-related hazards

-

Multi-state coverage complexities

Key considerations:

-

Class codes like 7219, 7228

-

Long-haul vs. short-haul coverage

-

Non-owned vehicle exposures

-

Multi-jurisdictional claims (accidents across states)

Workers’ Compensation for Oil & Gas Workers

Oil rigs and drilling fields involve:

-

Explosive environments

-

Hazardous chemicals

-

Heavy machinery

-

Extreme weather

Common injuries:

-

Burns

-

Crush injuries

-

Respiratory illnesses

-

Hearing damage

Policies may include:

-

Blowout prevention endorsements

-

Specialized liability protections

Workers’ Compensation for Miners

Mining workers face extreme hazards including:

-

Cave-ins

-

Explosions

-

Toxic gas exposure

-

Heavy equipment injuries

Federal Mine Safety & Health Administration (MSHA) regulations overlap with state workers’ comp.

Workers’ Compensation for Roofers

Roofing is consistently the #1 or #2 most dangerous job in America due to:

-

Falls from height

-

Heat exhaustion

-

Sharp tool injuries

Premium rates for roofers are among the highest in the country.

Workers’ Compensation for Loggers

Logging has an injury fatality rate nearly 30 times the national average due to:

-

Falling trees

-

Chainsaw accidents

-

Remote work sites

Workers’ comp becomes extremely costly, but necessary for hazard protection.

Workers’ Compensation for Manufacturing & Industrial Workers

Risks include:

-

Machine entanglement

-

Chemical burns

-

Fire hazards

-

Slip-and-fall injuries

-

Repetitive strain injuries

Industrial coverage includes special classifications like:

-

3632 Machine shops

-

3113 Tool manufacturing

Frequently Asked Questions About Workers’ Compensation Insurance for High-Risk Workers

Quick answers to common questions about workers’ compensation insurance for high-risk workers:

1: What qualifies someone as a high-risk worker under workers’ compensation?

A high-risk worker is someone employed in an occupation with elevated exposure to hazards such as heights, heavy equipment, chemicals, fire, unstable environments, or long-hour driving. Industries like construction, roofing, trucking, offshore oil, mining, logging, and manufacturing fall into this category.

2: Does workers’ compensation cover all workplace injuries?

Workers’ comp covers most work-related injuries, but not all.

Exclusions include:

-

Injuries caused by intoxication

-

Intentional self-harm

-

Violations of safety policies

-

Non-work-related illnesses

-

Off-duty activities

3: How much wage replacement does workers’ compensation pay?

Most states pay two-thirds of the worker’s average weekly wage, up to the state’s maximum weekly benefit. High-risk workers with severe injuries may qualify for long-term wage benefits or permanent disability compensation.

4: Who pays for workers’ compensation insurance?

The employer pays 100% of the premium. Workers cannot be legally required to contribute. This protects employees from financial burdens if injury occurs.

5: Do high-risk workers pay more for workers’ compensation?

Workers themselves do not pay more, but employers in high-risk industries pay significantly higher premiums because of:

-

Elevated injury frequency

-

Increased claim severity

-

Risk class codes

-

Higher EMR ratings

6: What happens if a workers’ comp claim is denied?

Workers can:

-

Request reconsideration

-

File an appeal with the state workers’ comp board

-

Attend a hearing

-

Provide additional medical evidence

7: Can independent contractors get workers’ comp coverage?

Generally, no. Unless state law or the contract requires it.

However, contractors in construction, trucking, or oil & gas may be required by the general contractor to carry their own policy.

8: Does workers’ comp cover illnesses or only injuries?

It covers both, as long as the illness is work-related. Examples:

-

Respiratory illness from chemical exposure

-

Heat exhaustion

-

Occupational hearing loss

Pre-existing conditions are typically excluded unless the job aggravates them.

9: Are offshore workers covered under standard workers’ comp policies?

Often no. Offshore workers may fall under:

-

The Longshore and Harbor Workers’ Compensation Act (LHWCA)

-

Jones Act (for seafarers)

-

State maritime workers’ comp

10: Can an employer be sued even if they carry workers’ comp?

Generally, workers’ comp shields employers from lawsuits. However, exceptions include:

-

Gross negligence

-

Intentional harm

-

Violations of safety laws

-

Failure to carry coverage (illegal in most states)

11: How long does a workers’ comp claim take to settle?

Most claims settle within:

-

30-90 days for minor injuries

-

6-18 months for moderate injuries

-

1-3+ years for severe injuries involving permanent disability

High-risk injury claims often take longer due to medical complexity.

12: Are workers’ compensation benefits taxable?

No.

Workers’ comp benefits are not considered taxable income, including disability payments under workers’ comp laws.

13: Can a worker choose their own doctor?

This depends on the state.

Some states allow free choice, others require the employer’s approved medical provider.

High-risk industries often encourage using occupational specialists for accurate reporting and treatment.

14: What happens if my employer doesn’t have workers’ comp insurance?

Workers may:

-

Report the employer to the state board

-

File a claim through a state uninsured employer fund (in some states)

-

Sue the employer for negligence

Employers may face:

-

Heavy fines

-

Criminal charges

-

Business shutdowns

15: Does workers’ comp cover mental health injuries?

Some states cover:

-

PTSD

-

Anxiety

-

Work-related stress

However, mental health claims are harder to prove and more regulated.

High-risk occupations like firefighting, trucking, or rescue operations see more of these claims.

Key Structural Takeaways for High-Risk Workers and Employers

To wrap up your comprehensive guide on Workers’ Compensation Insurance for High-Risk Workers, here is a practical checklist employers and workers can apply immediately.

Workers’ Compensation Checklist for High-Risk Industries

✔ For Employers

-

Maintain active workers’ comp coverage in all states of operation

-

Verify correct NCCI risk class codes

-

Review your EMR annually

-

Implement OSHA-compliant safety training

-

Establish clear injury reporting procedures

-

Maintain incident logs and safety audits

-

Use return-to-work programs for cost reduction

-

Choose a carrier experienced in high-risk occupations

-

Provide PPE and enforce compliance

-

Document subcontractor insurance requirements

✔ For High-Risk Workers

-

Report injuries immediately

-

Keep detailed medical records

-

Follow treatment plans

-

Understand your wage replacement rights

-

Know what injuries are and aren’t covered

-

File appeals when necessary

-

Ask your employer for the official workers’ comp provider

-

Confirm you are classified correctly (employee vs contractor)

-

Understand long-term disability options

-

Consider supplemental insurance:

How This Guide Fits Into the Workers’ Compensation System

This guide serves as the central pillar for understanding workers’ compensation insurance for high-risk workers.

Supporting guides expand on specific areas such as:

– Cost calculation

– Classification systems

– Claim denial reasons

– Coverage comparisons

Together, these resources form a complete system for evaluating risk, coverage, and claim outcomes in hazardous occupations.

Final Insight

Workers’ compensation insurance for high-risk workers does not eliminate workplace risk; it structures how that risk is funded, controlled, and validated.

The critical decision point is not when the policy is purchased, but when a claim is filed, where classification accuracy, compliance, and documentation determine whether benefits are paid or denied.