Executive Summary

Workers’ compensation high-risk jobs is a legally mandated, employer-funded system that provides medical care, wage replacement, and disability benefits for work-related injuries and illnesses. In high-risk jobs, stricter classification rules, higher premiums, and more intensive claim validation apply, as documented by Occupational Safety and Health Administration and National Institute for Occupational Safety and Health. Coverage is automatic, but claim approval depends on classification accuracy, safety compliance, and verified workplace causation. This structure makes workers’ compensation reliable for access to benefits, but conditional in payout depending on validation outcomes in high-risk occupations.

What is workers’ compensation for high-risk jobs?

Workers’ compensation for high-risk jobs is a legally required insurance system that provides medical care and wage replacement for workplace injuries, with stricter classification rules, higher costs, and more intensive claim validation.

What Is Workers’ Compensation?

Workers’ compensation is a statutory risk-transfer system designed to protect both employees and employers when workplace injuries occur. It ensures that workers receive defined benefits without needing to prove employer negligence, while employers gain protection from most injury-related lawsuits.

The system typically covers:

- Medical treatment and rehabilitation

- Partial wage replacement

- Disability compensation (temporary or permanent)

- Death benefits for dependents

Unlike private insurance, workers’ compensation:

- Does not require individual underwriting

- Applies automatically to eligible employees

- Operates under regulated benefit structures

This system is part of the broader framework covered in workers’ compensation insurance for high-risk workers, where coverage structures, eligibility rules, and cost drivers are explained in full.

For a foundational breakdown of scope and eligibility, see: What Is Workers’ Compensation for High-Risk Occupations?

Workers’ Compensation vs Other Insurance Systems

Workers’ compensation is often misunderstood because it differs structurally from other insurance products.

| Feature | Workers’ Compensation | Disability Insurance |

|---|---|---|

| Trigger | Work-related injury | Any disability |

| Approval | Automatic | Underwritten |

| Claim Decision | Validation-based | Contract-based |

This distinction is critical:

Workers’ compensation removes entry barriers but introduces strict validation at the claim stage.

Understanding the difference between income protection systems is critical, especially when comparing workers’ compensation vs disability insurance for hazardous workers.

System Architecture (How the System Works)

Workers’ compensation operates as a structured system with three interconnected layers:

1. Risk Pooling (Financial Layer)

Employers pay premiums into a pooled fund used to cover workplace injuries. This spreads risk across industries but adjusts costs based on exposure.

2. Classification Engine (Risk Mapping Layer)

Each worker is assigned a classification code based on actual job duties—not job titles. This determines:

- Premium rates

- Expected risk level

- Claim boundaries

3. Claim Validation Engine (Decision Layer)

When an injury occurs, the insurer evaluates:

- Whether the injury is work-related

- Whether classification matches duties performed

- Whether safety procedures were followed

Workers’ compensation is not an approval system—it is a validation system activated at the point of injury.

Classification Logic (Core Risk Driver in High-Risk Jobs)

Classification is the foundation of workers’ compensation and becomes more critical in high-risk environments.

How Classification Works

Insurers assign codes based on:

- Industry type

- Specific job duties

- Exposure to hazards

- Work environment conditions

Why High-Risk Jobs Face Stricter Classification

High-risk occupations—such as construction, offshore work, and industrial labor, typically involve:

- Heavy machinery

- Hazardous materials

- Physical exposure risks

This results in:

- Higher premium rates

- Increased scrutiny during claims

- Greater audit risk

In workers’ compensation high-risk jobs, classification accuracy becomes a critical factor in both pricing and claim approval.

Decision Breakpoint

Misclassification becomes a claim failure trigger when the worker performs duties outside their assigned classification at the time of injury.

This classification system is detailed in how insurers classify high-risk workers for workers’ compensation and occupational risk class codes explained, where classification accuracy directly impacts claims and pricing.

Underwriting Logic (Employer-Level Risk Evaluation)

Workers’ compensation underwriting focuses on the employer, not the individual worker.

Key Factors Insurers Evaluate

- Total payroll exposure

- Industry risk classification

- Claims history

- Experience Modification Rate (EMR)

- Safety programs and compliance systems

Experience Modification Rate (EMR)

EMR reflects a company’s past claims performance:

- EMR < 1.0 → Lower-than-average risk

- EMR > 1.0 → Higher-than-average risk

This evaluation framework aligns with the broader system explained in how insurance underwriting works for high-risk jobs, where insurers balance classification accuracy, verification, and financial exposure.

Critical Insight

Underwriting determines how risk is priced, but claim validation determines whether benefits are paid.

These pricing factors are fully broken down in how workers’ compensation premiums are calculated, including payroll, classification rates, and EMR.

How Much Does Workers’ Compensation Cost for High-Risk Jobs?

The cost of workers’ compensation high-risk jobs policies is significantly higher due to increased injury probability and claim severity.

Premiums are calculated using:

Premium = Payroll × Classification Rate × EMR

Typical Cost Ranges

- Construction: 5%–20% of payroll

- Offshore / Oil & Gas: 10%–30%

- Hazardous manufacturing: 3%–15%

Actual rates vary by jurisdiction, claims history, and classification accuracy.

Cost Drivers

- High injury frequency

- Severe claims

- Weak safety practices

- Misclassification discovered during audits

Cost Insight

Workers’ compensation costs are driven more by cumulative exposure than by individual incidents.

High-risk occupations face significantly higher premiums, as explained in why dangerous jobs pay higher workers’ compensation premiums.

Who Is Covered Under Workers’ Compensation?

Covered:

- Full-time employees

- Part-time employees

Typically Not Covered:

- Independent contractors

- Self-employed individuals

Coverage Breakpoint

Misclassification of worker status (employee vs contractor) is a major cause of claim disputes and denial.

How the System Works (Step-by-Step Process)

- Employer purchases workers’ compensation policy

- Worker performs assigned duties

- Injury occurs

- Incident is reported

- Claim is filed

- Insurer investigates

- Claim is approved, adjusted, or denied

Transition Insight

Filing a claim activates the validation system, where eligibility is tested against defined rules.

What Should You Do After a Workplace Injury?

- Report the injury immediately

- Seek medical treatment

- Document the incident

- File a claim through your employer

Action Insight

Delayed reporting significantly increases the likelihood of claim denial or dispute.

How Long Do Workers’ Compensation Claims Take?

- Simple claims: a few days to weeks

- Complex high-risk claims: weeks to months

Time Insight

Claims involving classification disputes or safety violations take significantly longer to resolve.

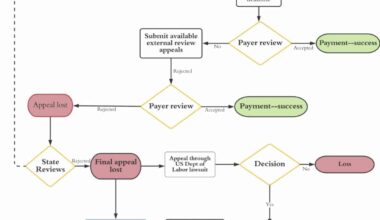

Claim Validation Engine (Where Claims Are Won or Lost)

Claims in workers’ compensation high-risk jobs environments are subject to stricter validation due to higher risk exposure.

Every claim is evaluated through three core tests:

1. Causation Test

Was the injury directly related to work activities?

2. Classification Test

Was the worker performing duties within their assigned classification?

3. Compliance Test

Were safety protocols followed?

Decision Thresholds That Trigger Denial

Claims are most likely denied when:

- Classification mismatch occurs at the time of injury

- Safety violation is clearly linked to the incident

- Reporting delay exceeds acceptable timelines

- Worker status is disputed

Decision escalation threshold:

Claims move from review to denial when two or more validation failures occur simultaneously, particularly:

– Classification mismatch + safety violation

– Late reporting + inconsistent documentation

– Worker status dispute + lack of verifiable job duty alignment

At this point, insurers classify the claim as unmanaged or unverifiable risk, leading to denial or reduced payout.

Failure Paths (Why Claims Are Denied)

Workers’ compensation high-risk jobs claims are more likely to be denied when classification or compliance conditions are violated.

Common reasons include:

- Injury not work-related

- Misclassification

- Safety violations

- Late reporting

- Contractor disputes

- Fraud or inconsistent reporting

High-risk claim failure pattern:

Single failure → Increased scrutiny

Dual failure → High dispute probability

Triple failure → Likely denial

This layered failure structure explains why high-risk job claims fail more frequently than standard workplace claims.

Compound Failure Insight

The highest denial risk occurs when multiple failure factors, especially classification and compliance overlap.

Claim Breakpoints (Where Outcomes Change)

Claims typically shift at three stages:

Stage 1: Initial Screening

Immediate rejection if not work-related

Stage 2: Investigation Phase

Disputes over classification or compliance

Stage 3: Final Determination

- Full approval

- Partial payout

- Denial

Why Workers’ Compensation High-Risk Jobs Claims Are Denied

Claims are denied due to misclassification, safety violations, non-work-related injuries, late reporting, or disputes over employment status.

Breakpoint Insight

Claim outcomes depend more on validation criteria than injury severity.

Structural Exclusions (What Is Not Covered)

Workers’ compensation does not cover:

- Off-duty injuries

- Intentional harm

- Injuries caused by policy violations

- Non-work-related activities

Many denied claims arise from structural exclusions, as detailed in common workers’ compensation exclusions in high-risk industries.

Limitations of Workers’ Compensation in High-Risk Jobs

- Income replacement is partial

- Benefit caps may limit payouts

- Complex roles have higher dispute rates

- Misclassification increases uncertainty

Workers’ compensation provides structured access to benefits, but does not guarantee full financial protection in high-risk scenarios.

When Workers’ Compensation Is Not Enough

Additional protection may be necessary when:

- Income exceeds benefit caps

- Long-term disability risk is high

- Employer compliance is uncertain

Legal Interaction: Employer Liability

Workers’ compensation limits lawsuits but does not eliminate employer liability in all situations.

Workers’ compensation interacts with broader liability systems, which are explained in employer liability vs workers’ compensation explained.

Evidence Block (Why High-Risk Jobs Face Stricter Systems)

Data from Occupational Safety and Health Administration and National Institute for Occupational Safety and Health shows:

- Higher injury rates in hazardous industries

- Increased fatality risk in construction and industrial sectors

Industry-specific injury rates can also be reviewed through Bureau of Labor Statistics

High-risk industries consistently show materially higher injury frequency and severity rates, which directly correlates with stricter classification enforcement, elevated premium ranges, and more aggressive claim validation thresholds.

Claim Validation Checklist (High-Risk Jobs)

- Was the injury work-related?

- Was classification accurate?

- Were safety procedures followed?

- Was the injury reported immediately?

Employer Risk Exposure

Employers face:

- Premium increases after claims

- Regulatory inspections

- Audit penalties

- Retroactive premium adjustments

Audit Insight

Misclassification can trigger audits, backdated premiums, and claim disputes simultaneously.

Regulatory Variation (Important)

Workers’ compensation rules, benefits, and limits vary by jurisdiction and regulatory framework.

Real-World Scenario (Approval vs Denial)

Approved Case:

- Correct classification

- Safety compliance

- Verified work-related injury

Denied Case:

- Task outside classification

- Safety violation

- Inconsistent reporting

Outcome Insight

Claim outcomes are determined by validation logic, not the existence of coverage.

Key Takeaways

- Workers’ compensation is mandatory and system-driven

- No medical underwriting is required

- High-risk jobs increase cost and scrutiny

- Claims are validated, not guaranteed

- Classification and compliance determine outcomes

Final system insight:

Workers’ compensation does not remove workplace risk; it redistributes and regulates it, shifting the critical decision point from policy issuance to claim validation, where classification accuracy and compliance determine financial outcomes.

Part of the Workers’ Compensation System

This article is part of the broader guide on workers’ compensation insurance for high-risk workers, which explains how coverage, pricing, underwriting, and claims interact across hazardous occupations.

- What Is Workers’ Compensation for High-Risk Occupations?

- How Insurers Classify High-Risk Workers for Workers’ Comp

- Occupational Risk Class Codes Explained

- How Workers’ Compensation Premiums Are Calculated

- Why Dangerous Jobs Pay Higher Workers’ Comp Premiums

- Workers’ Comp vs Disability Insurance for Hazardous Workers

- Employer Liability vs Workers’ Compensation Explained

- Common Workers’ Compensation Exclusions in High-Risk Industries