Insurance underwriting for high-risk jobs operates under a different set of structural constraints than underwriting for standard occupations. As occupational danger increases, underwriting shifts from flexible risk evaluation toward rigid system control, driven by capital protection requirements, loss severity limits, and risk aggregation management. Eligibility rules, medical requirements, and approval outcomes are downstream effects of underwriting constraints, not independent decisions.

Many workers expect insurance approval to reflect fairness, experience, or personal responsibility. In practice, underwriting decisions are governed by systems designed to control loss exposure, not to evaluate individual care, skill, or intent. In high-risk occupations, this disconnect between expectation and system logic is the primary source of confusion, restriction, and rejection.

This page explains how insurance underwriting functions at a system level for dangerous work. It does not assess individual outcomes, define eligibility rules, or describe approval decisions in isolation. Those components are addressed in their respective canonical explainers.

To understand why underwriting decisions affect coverage the way they do, it helps to view them within the larger context of insurance systems across high-risk occupations.

How Underwriting Functions as a System

Insurance underwriting for high-risk jobs is not a single decision. It is a layered risk-control system designed to limit loss exposure before a policy is ever issued.

At a system level, underwriting performs three functions:

-

Filters which occupational risks may enter the insurance pool

-

Constrains how much exposure the insurer can accept

-

Shapes coverage structure before pricing or claims occur

Each function is governed by different constraints, and each is documented separately within this cluster. Confusion arises when these functions are treated as interchangeable.

These constraints are enforced through eligibility filters, classification systems, and approval thresholds, each operating independently within underwriting frameworks.

Why Insurance Feels Different for High-Risk Workers

High-risk workers experience insurance differently because underwriting treats their jobs as exposure problems, not individual situations.

Underwriting is not a judgment of character, safety awareness, or professionalism. It is a filtering process that decides:

-

Who is allowed into the insurance system

-

How much risk an insurer is willing to carry

-

Where coverage must be limited, priced higher, or excluded entirely

For many workers, this only becomes visible after:

-

An application is declined

-

Coverage is restricted

-

A claim fails due to exclusions that were never clearly explained

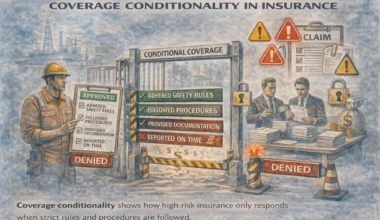

Underwriting limits for hazardous occupations are aligned with capital adequacy frameworks designed to preserve solvency under adverse loss scenarios. These frameworks prioritize protection against extreme outcomes rather than accommodation of marginal risk, which materially reduces underwriting tolerance as occupational severity increases.

Understanding underwriting early prevents false expectations later.

What Insurance Underwriting Actually Is

Insurance underwriting is a risk selection and risk control system. Its purpose is to prevent insurers from accepting exposure that could produce losses larger than the premiums collected.

Insurance systems separate underwriting into distinct controls that are often conflated:

-

Eligibility determines whether a risk may be considered at all

-

Approval determines whether that eligible risk can be accepted within system limits

-

Pricing determines cost after acceptance

Each control is constrained by different models and thresholds. Approval outcomes cannot override eligibility limits, and pricing cannot compensate for risks that exceed approval tolerance.

Being “insured” does not mean being underwritten favorably. A policy can exist while still containing:

-

Strict eligibility conditions

-

Occupational exclusions

-

Coverage caps

-

Claim limitations tied to job duties

Underwriting decisions are made before pricing, before coverage wording, and long before any claim occurs. Once an underwriting decision is made, everything else follows from it.

At a regulatory level, insurance underwriting refers to the process by which insurers assess risk exposure and establish eligibility, pricing, and coverage conditions prior to issuing a policy.

The Four-Layer Underwriting System for High-Risk Jobs

Underwriting for high-risk work operates through multiple decision layers, not a single approval step. Each layer acts as a gate. These layers include classification systems, medical risk controls, and external data inputs such as occupational health reporting, each influencing underwriting outcomes independently. Failing any one gate can restrict or eliminate coverage.

These layers are:

-

Eligibility and approval gates

-

Risk assessment and occupational classification

-

Medical and human risk factors

-

Modifiers, variations, and outcome changes

Understanding these layers explains why similar workers can receive very different outcomes.

Eligibility & Approval Gates

How Insurers Decide Who Can Apply at All

Before pricing or policy design begins, insurers determine basic eligibility. At this stage, underwriting asks:

-

Is this job type insurable at all?

-

Does it exceed automatic risk limits?

-

Does it require manual underwriting or specialist approval?

Some high-risk jobs are declined automatically based on historical loss data alone. Others are allowed through only under strict conditions.

Eligibility represents the first gate in this system, determining whether a risk may even enter underwriting consideration before approval, pricing, or coverage structure are evaluated through the eligibility requirements for high-risk jobs.

Why High-Risk Jobs Face Stricter Approval

High-risk occupations produce:

-

Higher injury severity

-

Longer recovery times

-

More complex claims

-

Greater litigation exposure

Reinsurance arrangements further constrain approval outcomes. Treaty conditions frequently impose attachment thresholds, concentration limits, and hazard exclusions that insurers must enforce at the underwriting stage. When occupational risk profiles threaten these limits, approval standards tighten regardless of individual circumstances.

Underwriting responds by tightening approval rules. This is not personal. It is statistical.

This tightening process reflects systemic capital protection behavior rather than individual evaluation, a framework analyzed more fully in why high-risk jobs face stricter insurance approval.

Job Titles vs Actual Job Duties

Underwriting systems rely heavily on job titles, even when those titles do not reflect real duties. A misclassified role can:

-

Trigger exclusions

-

Change occupation class ratings

-

Reduce eligibility without warning

This is why job description accuracy matters more than intent.

Common Rejection Patterns for High-Risk Workers

Certain workers are frequently rejected due to:

-

Mixed or undefined duties

-

Rotational or offshore schedules

-

Exposure to height, heavy machinery, water, or isolation

-

Prior claims combined with hazardous roles

Rejection patterns are systemic, not random.

Risk Assessment & Occupational Classification

How Insurers Measure Occupational Risk

Underwriting measures risk using:

-

Historical claims data

-

Industry loss ratios

-

Frequency and severity modeling

-

Worst-case exposure assumptions

These models simplify real jobs into categories that underwriting systems can manage.

Occupation Class Ratings Explained

Occupation classes group jobs by expected loss behavior, not danger alone. Two roles may look similar in practice but fall into different classes due to:

-

Injury severity trends

-

Claim duration

-

Recovery costs

Once assigned, an occupation class influences pricing, exclusions, and eligibility.

The structure and impact of classification systems are explained in occupation class ratings explained, where underwriting groups jobs based on loss behavior rather than perceived danger.

Risk Assessment Tools Used by Insurers

Underwriting tools include scoring systems, internal risk models, and underwriting manuals. These tools prioritize consistency over nuance, which is why they often misrepresent complex jobs.

For a system-level explanation of how insurers quantify occupational exposure before approval decisions are made, see Risk Assessment Tools Used by Insurers.

Employer, Health, and Background Inputs

Underwriting may also review:

-

Occupational health reports

-

Employer safety history

-

Compliance and background indicators

These inputs rarely override occupational risk but can worsen outcomes when negative.

One of the most influential but misunderstood inputs is analyzed in the role of occupational health reports, where employer-provided medical and safety data can reinforce or undermine underwriting decisions.

Occupational classification functions as a loss-correlation control rather than a descriptive label. Underwriting systems rely on category-level behavior because correlated losses within hazardous industries cannot be diversified through individual assessment alone.

Medical & Human Risk Factors

Why Medical Exams Are Common for High-Risk Jobs

Medical underwriting is used to control severity risk, not to assess overall health. Exams focus on:

-

Pre-existing conditions

-

Injury aggravation risk

-

Recovery probability

Passing a medical exam does not eliminate occupational exclusions.

Medical requirements in hazardous occupations are examined in medical exams required for high-risk coverage, where insurers use health data to control severity risk and recovery uncertainty.

Non-Medical Insurance Options and Their Limits

Non-medical coverage may exist for high-risk jobs, but it often includes:

-

Lower coverage limits

-

Stricter exclusions

-

Higher premiums

These options reduce underwriting friction, not risk.

Alternative pathways without medical screening are explored in non-medical insurance options for dangerous jobs, where reduced underwriting shifts risk control into pricing limits and policy restrictions.

How Age and Experience Affect Eligibility

Experience can reduce frequency risk but not severity risk. Age increases recovery complexity. Underwriting balances both, often resulting in tighter limits for older or long-tenured workers in hazardous roles.

Modifiers, Variations & Outcome Changes

Why Underwriting Differs by Country

Underwriting rules vary due to:

-

Regulation

-

Enforcement standards

-

Local claims history

-

Litigation environments

The same job can receive different underwriting outcomes across borders.

The Conditional Role of Safety Training

Safety training can help only when:

-

It is standardized

-

It is verifiable

-

It aligns with underwriting models

Training rarely overrides occupational risk on its own.

Can Approval Chances Be Improved?

Some factors can be improved:

-

Accurate job classification

-

Clear duty definitions

-

Documentation quality

Many factors cannot be changed:

-

Core occupational risk

-

Industry loss history

-

Insurer risk appetite

Improvement is conditional, not guaranteed.

Why Underwriting Outcomes Change Over Time

Underwriting is dynamic. Approval rules shift due to:

-

Claims cycles

-

Industry loss spikes

-

Regulatory pressure

-

Carrier appetite changes

Workers may lose access to coverage even when their job does not change.

Why Understanding Underwriting Matters Before You Apply

Most insurance failures happen before a claim, during underwriting. Understanding the system helps workers:

-

Avoid unsuitable applications

-

Set realistic expectations

-

Identify hidden restrictions early

Insurance does not fail randomly. It fails predictably, based on underwriting logic.

How the Underwriting System Fits Together

Underwriting outcomes for high-risk jobs are produced through a sequence of constrained evaluations rather than a single decision. Eligibility determines whether a risk may be considered, approval determines whether it can be accepted within system limits, and coverage structure determines how exposure is controlled after acceptance.

Each component operates under different constraints and is documented separately within this cluster:

-

Eligibility requirements explain how insurers determine whether a risk may enter underwriting consideration at all

-

Occupational classification explains how jobs are grouped to control correlated loss exposure

-

Approval limitations explain why acceptance standards tighten as occupational severity increases

-

Medical underwriting explains how severity and recovery risk are managed at the individual level

-

Rejection patterns and exclusions explain where system limits are enforced

Understanding underwriting requires viewing these components together rather than evaluating outcomes in isolation.