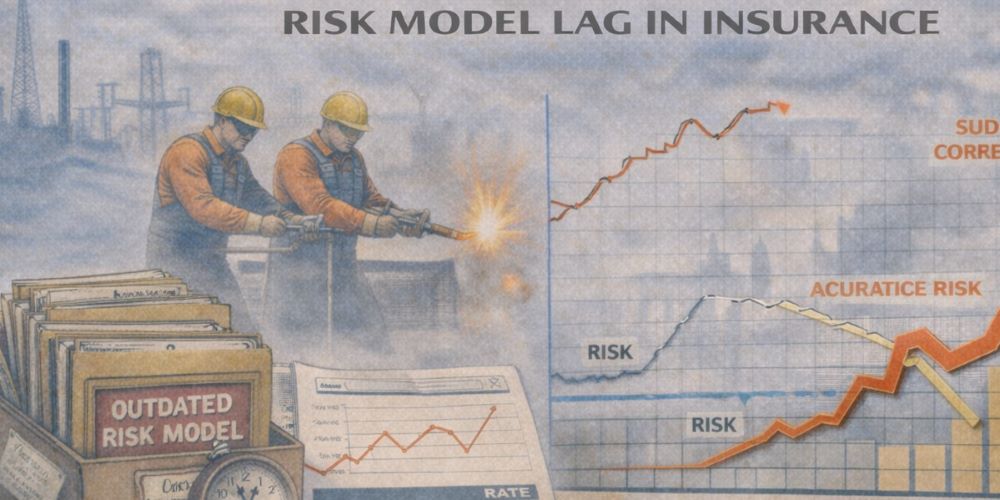

Risk model lag is the delay between real-world changes in job risk and when insurance risk models finally recognize and price those changes.

It is not about denial.

It is about the model being behind reality.

For high-risk workers, the danger evolves faster than the math.

What Risk Model Lag Means

Insurance pricing and eligibility rely on models built from:

-

Historical loss data

-

Past claim patterns

-

Established exposure assumptions

These models update slowly.

When jobs change new equipment, new methods, harsher environments, the model keeps using old assumptions.

That gap between reality and the model is risk model lag.

This delay closely mirrors risk pricing lag, where premiums remain artificially low until models finally catch up with losses.

Actuarial organizations such as the Society of Actuaries explain how insurance risk models depend on mature loss data before assumptions are updated.

Why High-Risk Jobs Experience It More

High-risk industries change rapidly:

-

New technology

-

New hazards

-

New failure modes

But insurers must wait for:

-

Losses to occur

-

Claims to mature

-

Data to stabilize

So models lag behind emerging danger.

When the update finally comes, it is abrupt.

How This Affects Workers

Risk model lag means:

-

Insurance looks affordable at first

-

Coverage is widely offered

-

Losses then surge

-

Prices spike and capacity disappears

Workers feel punished for risks they didn’t know were unrecognized.

Why Corrections Are Sudden

Models do not adjust gradually.

They reset after enough data accumulates.

That reset creates:

-

Premium shocks

-

Eligibility tightening

-

Market exits

The lag ends all at once.

When models finally reset, the result is often premium volatility, as insurers rush to correct years of under-recognized exposure.

In the Risk Job Insurance System

Risk model lag explains why:

-

Markets swing violently

-

Premium volatility appears sudden

-

Capacity withdraws after “surprise” losses

It is the blind spot that creates insurance whiplash.

This concept is part of the broader Risk Job Insurance Definitions, which explain how insurance systems treat high-risk work.

Related Risk Job Insurance Definitions

– Coverage Exhaustion

– Coverage Cliff Effects

– Risk Model Lag

– Coverage Latency