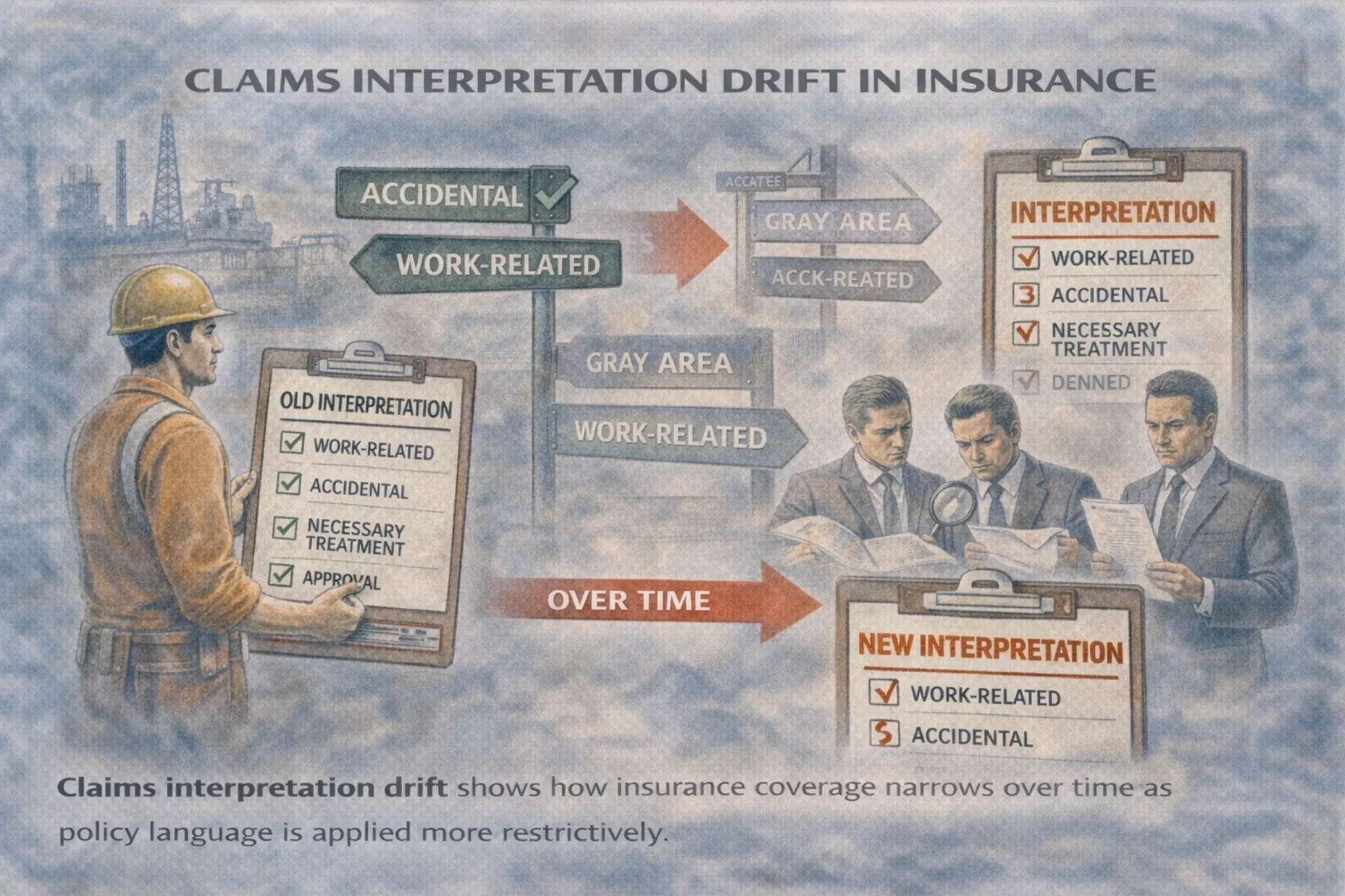

Claims interpretation drift is the gradual change in how insurers interpret policy language over time, often narrowing how coverage responds to high-risk claims.

It is not a policy rewrite.

It is a shift in meaning.

For high-risk workers, the same words can stop protecting them.

What Claims Interpretation Drift Means

Insurance policies rely on interpretation.

Over time, insurers adjust how they read:

-

“Work-related”

-

“Accidental”

-

“Necessary treatment”

-

“Occupational duties”

These shifts usually follow:

-

Court rulings

-

Loss experience

-

Regulatory pressure

-

Internal claims guidance

The policy text stays the same.

The outcome changes.

That is claims interpretation drift.

Over time, this process increases claims friction, as workers face longer reviews and more resistance even when policy wording appears unchanged.

Why High-Risk Claims Are Affected First

High-risk claims involve:

-

Complex causation

-

Gray areas

-

Expensive consequences

So insurers refine interpretations to limit exposure.

Each adjustment seems reasonable alone.

Together, they narrow coverage.

These narrowing interpretations often develop alongside claims severity bias, where insurers expect high-cost outcomes before a claim is fully evaluated.

How This Affects Workers

Claims interpretation drift means:

-

Old claims would have paid

-

New claims are questioned

-

Coverage feels inconsistent

-

Workers lose trust in policy language

The promise changes without notice.

Why This Is Hard to Challenge

Drift happens internally.

Workers only see the result, not the rule change.

By the time patterns appear, the interpretation is already “standard.”

Regulatory and legal analysis from organizations such as the National Association of Insurance Commissioners show how claims guidance and interpretation standards evolve without formal policy amendments.

In the Risk Job Insurance System

Claims interpretation drift explains why:

-

Policies feel weaker over time

-

Identical injuries get different outcomes

-

High-risk insurance becomes unpredictable

It is how insurers quietly adapt coverage without rewriting contracts.

See the full Risk Job Insurance definitions for related system-level concepts.