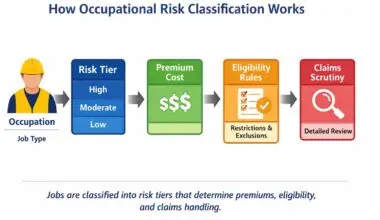

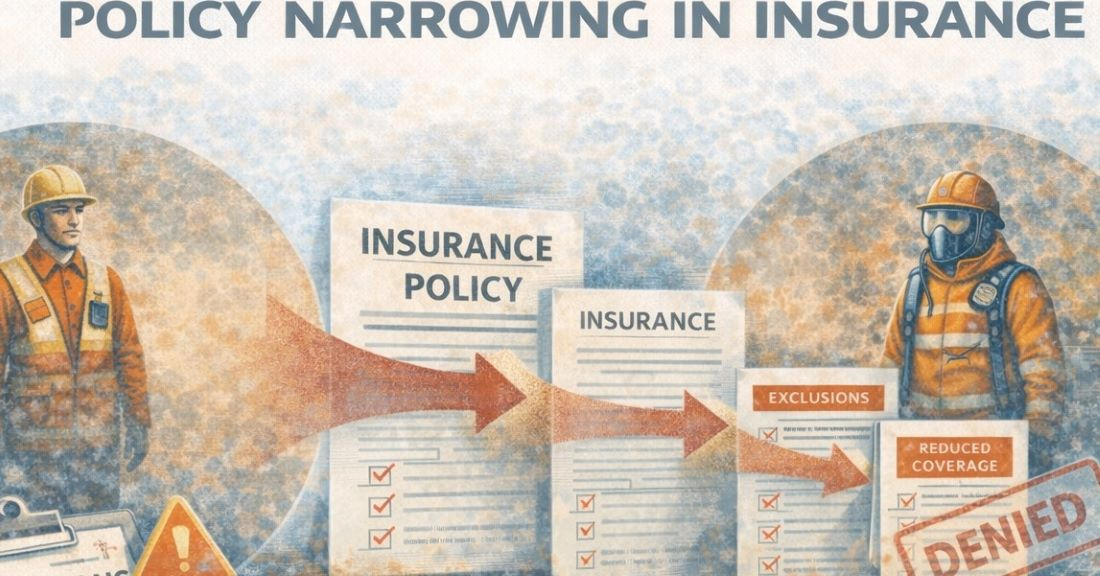

Policy narrowing is the process by which insurance coverage for high-risk jobs becomes more limited over time through exclusions, reduced definitions, and tighter conditions.

It is not about removing coverage.

It is about shrinking what coverage means.

High-risk insurance rarely disappears at once; it erodes.

What Policy Narrowing Means

When insurers face rising losses or uncertainty, they rarely cancel everything immediately.

Instead, they:

-

Add exclusions

-

Tighten definitions

-

Reduce what counts as a covered event

-

Narrow who qualifies

This gradual restriction is policy narrowing.

Industry groups such as the Insurance Information Institute explain how insurers use exclusions and coverage definitions to manage rising risk.

Why High-Risk Jobs Experience It First

High-risk work produces:

-

Expensive claims

-

Ambiguous injuries

-

Disputes over causation

Insurers respond by slowly tightening policies until only the safest scenarios remain covered.

Coverage still exists, but only on paper.

Policy narrowing is one of the main drivers of coverage fragility, making high-risk insurance unstable even when policies remain active.

How It Affects Workers

Policy narrowing means:

-

More things are excluded

-

Claims fail on technicalities

-

Workers believe they are insured when they are not

The policy looks the same. The protection is not.

Many of these restrictions come from moral hazard controls, which tighten coverage when insurers fear behavior-driven losses.

Why This Happens Quietly

Canceling coverage causes backlash.

Narrowing it avoids attention.

The risk is shifted away without headlines.

In the Risk Job Insurance System

Policy narrowing explains why:

-

High-risk policies feel hollow

-

Coverage shrinks after claims

-

Protection disappears without formal cancellation

It is one of the most common ways insurers retreat from dangerous work.