Claims friction in insurance is the resistance that occurs inside insurance systems when a claim moves through review, verification, and approval, especially when the claim involves a high-risk occupation.

It is not always denial.

It is the drag placed on the claim by the system.

For many high-risk workers, coverage does not fail because a policy does not exist. It fails because the system makes the claim hard to pass.

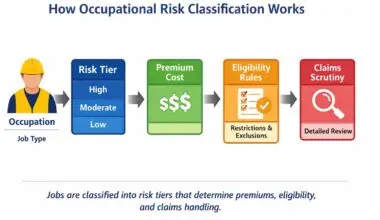

What Claims Friction Means in Insurance

When a claim is filed, it must pass through multiple system checks:

-

Occupational verification

-

Exposure review

-

Causation analysis

-

Policy definition matching

-

Exclusion screening

Each step introduces friction.

Low-risk jobs move through these steps quickly because their exposure patterns are simple and predictable. High-risk jobs trigger extra layers of review because their losses are larger, more complex, and more expensive.

That extra scrutiny is claims friction.

When injuries result from exposure stacking, insurers must analyze multiple hazards and causes, which increases claim complexity and delays.

Why High-Risk Claims Face More Resistance

High-risk work produces injuries and losses that are:

-

More severe

-

More ambiguous

-

More costly

-

More likely to involve multiple causes

This makes it harder for insurance systems to decide whether a claim fits neatly inside policy definitions.

So instead of paying quickly, insurers slow the process.

They ask for:

-

More documentation

-

More investigation

-

More verification

-

More interpretation

This does not always mean the claim will be denied.

It means it will not move smoothly.

The same systems that create eligibility gating also increase claims friction, because high-cost workers are treated as structurally risky even after they are insured.

How Claims Friction Changes Outcomes

As friction increases:

-

Payments are delayed

-

Benefits are reduced

-

Disputes become more common

-

Workers abandon or settle claims

Two workers can have the same injury and the same policy, yet experience completely different outcomes because one job creates more system friction than the other.

This type of claims friction is common in offshore injury cases, where workers’ compensation claims involve jurisdictional review, employer liability questions, and extended investigation timelines.

Insurance regulators such as the National Association of Insurance Commissioners document how claims are reviewed, disputed, and escalated when coverage is questioned.

Why Good Policies Still Produce Bad Experiences

Many high-risk workers believe their coverage failed because their policy was bad.

In reality, the policy may be fine.

The problem is that the claim had to pass through a system designed to resist high-cost, high-uncertainty losses.

That resistance is claims friction.

In the Risk Job Insurance System

Claims friction explains why:

-

High-risk workers wait longer for payments

-

Claims are challenged more aggressively

-

Legal and administrative disputes are common

It is the mechanism that turns occupational risk into real-world insurance stress.

Without understanding claims friction, workers assume insurers are acting unfairly.

With it, the behavior becomes structurally predictable.