Introduction

Life insurance for construction workers is often assumed to be simple:

pay the premium, keep the policy active, and your family is protected.

Because life insurance is not tied directly to job sites the way workers’ compensation is, many construction workers assume that their occupation matters very little once a policy is issued.

But construction plays a much bigger role than most people realize.

Life insurance evaluates risk before coverage exists. It looks at:

-

what kind of work you do,

-

how often you face severe hazards,

-

and how predictable your risk profile is.

These decisions happen quietly during underwriting, long before a claim ever occurs. Many construction workers never see this process; they only feel its effects when approval is delayed, premiums are higher, or exclusions appear in the policy.

This article explains how life insurance actually treats construction workers. It focuses on classification, underwriting logic, and why outcomes sometimes feel stricter than expected.

This explanation fits within the broader guide on how insurance systems actually work for construction workers, where life insurance is examined alongside other insurance systems that affect construction jobs.

Why Construction Work Matters in Life Insurance Underwriting

Life insurance underwriting is centered on mortality risk: the likelihood that an insured person may die during the policy term. Occupation becomes relevant when the nature of the work increases exposure to severe or unpredictable outcomes.

Construction work introduces several elements that insurers associate with elevated mortality risk. These include working at height, operating heavy machinery, exposure to hazardous environments, and sustained physical strain. Even when safety standards are high and protocols are followed, these elements introduce risk that cannot be fully eliminated.

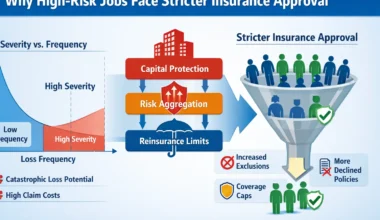

Life insurance underwriting focuses less on how often minor injuries occur and more on the severity of potential outcomes. Rare but catastrophic events carry more weight than frequent but manageable ones. From an insurer’s perspective, the question is not how safely work is usually performed, but what could plausibly happen under adverse conditions.

Construction combines multiple severity multipliers. Height increases the risk of fatal falls. Heavy equipment introduces the possibility of crushing or catastrophic trauma. Dynamic environments reduce predictability. Life insurance systems are designed to account for these factors even when incidents are uncommon.

Insurers are not assessing whether construction workers are careless. They are assessing whether the nature of the work increases the chance of irreversible outcomes. This distinction explains why construction is treated differently from many other occupations in life insurance underwriting, even when safety records are strong.

The construction industry itself is structured around this same idea. On large projects, risk is not treated as something owned by individual workers or employers, but as something created by the project environment. This is why many sites operate under owner-controlled or contractor-controlled insurance programs (OCIP or CCIP), where a single policy covers everyone on the project. Life insurers view construction workers through a similar lens: exposure comes from the environments they work in, not just from personal behavior. Research bodies that analyze construction site risk consistently show that large projects are governed by shared safety and insurance frameworks rather than by individual employers.

Example: A carpenter who works mainly indoors cutting trim faces different mortality exposure than an ironworker assembling structures at height every day.

Insurers account for occupational risk in construction work because it combines severity, unpredictability, and environmental exposure that affect long-term mortality assessment.

How Life Insurance Classifies Construction Workers

Life insurance does not treat “construction worker” as a single category. Insurers break construction work into risk classes based on duties, environments, and exposure frequency.

Two workers with the same job title may be placed in different risk categories depending on:

-

Whether they work at height

-

Whether they operate heavy equipment

-

Whether they perform hands-on labor or supervisory tasks

-

Whether work environments are controlled or variable

These classifications are not informal judgments. They are structured categories built into underwriting systems so risk can be applied consistently across large groups. Once a category exists, individual applicants are placed into it based on how their work is described.

The rigidity is intentional. Life insurance systems must remain stable across thousands or millions of policies. Allowing individual exceptions based on experience or perceived carefulness would undermine pricing consistency and risk pooling.

This is why life insurance does not adapt flexibly to individual narratives. The system protects its overall structure by applying the same categories repeatedly. Construction workers may experience this as inflexible or unfair, but from the insurer’s perspective, consistency is essential to the system’s survival.

This classification logic explains why life insurance outcomes can vary widely among construction workers who appear similar on paper. Small differences in duties or environments can place workers on different sides of classification boundaries, leading to different underwriting results.

Why Experience and Safety Records Do Not Offset Occupational Risk

A common assumption among construction workers is that experience, training, and a strong safety record should improve life insurance treatment. These qualities matter deeply on a job site, but they play a limited role in life insurance underwriting.

Life insurance systems are designed to evaluate risk at scale. They rely on role-based exposure rather than individual behavior. An experienced worker and a new worker performing the same duties are exposed to the same underlying hazards from an insurer’s perspective.

Insurers cannot reliably verify or quantify caution, judgment, or professionalism in a way that can be priced consistently. Self-reported safety practices do not translate into actuarial inputs. Even documented training does not remove exposure to height, machinery, or hazardous environments.

Skill can reduce the likelihood of certain incidents, but it does not eliminate exposure. Life insurance evaluates the presence of risk factors, not the probability that an individual will avoid them successfully.

This disconnect explains why underwriting decisions often feel disconnected from personal work history. The system is not dismissing experience; it is operating at a level where experience cannot be meaningfully priced. Experience helps prevent incidents, but it cannot eliminate exposure. Life insurance prices exposure, not confidence.

Exclusions and Occupational Limitations in Life Insurance

Life insurance policies may include exclusions or limitations related to occupational risk. These provisions are designed to control exposure rather than to penalize workers.

In construction, exclusions may relate to:

-

Specific high-risk activities

-

Certain environments or duties

-

Non-routine or specialized tasks

These exclusions are typically written broadly. They exist before any individual applies for coverage and are applied consistently across categories. They are not negotiated per worker, nor are they adjusted based on personal safety records.

Exclusions function as guardrails within the policy structure. They protect the insurer from exposure that exceeds the assumptions built into the pricing model. Because construction work can vary widely, exclusions are often drafted conservatively to account for worst-case scenarios.

In construction, exclusions sometimes include:

-

Work at height above a certain limit

-

Explosives or demolition work

-

Offshore or remote construction

-

Crane or high-risk equipment operation

When a claim intersects with an excluded activity, coverage may be limited or denied even though the policy was active. This outcome feels unexpected because exclusions are rarely discussed in practical terms before they are triggered.

Understanding that exclusions are structural rather than personal helps explain why they can feel sudden or harsh. They are not responses to behavior; they are components of system design.

Why Life Insurance Does Not Respond to Injury or Career Loss

Another common misunderstanding is the belief that life insurance provides protection when construction work becomes impossible due to injury or illness.

Life insurance responds only to death. It does not replace income, address disability, or respond to career-ending physical limitations. For construction workers, this distinction matters because the most common disruptions to work occur long before life insurance would ever apply.

A worker may lose the ability to perform construction work due to injury, illness, or physical decline, yet life insurance remains unchanged because no death has occurred. From a practical standpoint, this can be devastating. From an insurance standpoint, the policy is functioning exactly as designed.

Life insurance is not built to protect careers or earning capacity. It exists to manage mortality risk. Confusion arises when workers assume it operates as a general safety net rather than a narrowly defined system.

If work stops due to injury, disability insurance for construction workers, not life insurance, is the system designed to respond.

Why Life Insurance Outcomes Feel Inconsistent in Construction

Construction workers often compare life insurance experiences and feel confused by differences. One worker may receive standard terms, while another faces restrictions or delays.

These differences usually result from:

-

Duty-based risk classification

-

Environment and exposure frequency

-

How work is categorized within underwriting systems

Small differences in duties can lead to significant classification changes. Construction amplifies these boundary effects because roles are often mixed and environments shift from project to project.

From the worker’s perspective, outcomes feel inconsistent. From the insurer’s perspective, they reflect structured risk segmentation applied consistently across categories.

Example:

Two workers may have the same job title, but one spends most days supervising on the ground while the other works primarily at height. The second worker may receive a higher premium or limited coverage, even though both say they are “construction workers.”

Understanding this helps explain why life insurance decisions can feel unpredictable even when the system itself is highly ordered.

How This Fits Within Construction Workers Insurance

Life insurance is one component of construction workers insurance, but it operates independently from job-site systems like workers’ compensation. It evaluates risk through long-term mortality exposure rather than through immediate work-related injury.

Within risk job insurance, life insurance highlights how different systems assess different dimensions of risk. For construction workers, this often means that life insurance outcomes are shaped by occupational classification even when no incident has occurred.

In simple terms, life insurance judges the role, not the worker. Classification matters more than personal history.

Understanding this helps place life insurance decisions in context rather than viewing them as arbitrary or personal.

Final Note

This article does not explain how to obtain life insurance or how to improve approval outcomes. Its purpose is clarity. Life insurance treats construction work as elevated exposure, not as a measure of character or competence. Understanding this logic reduces confusion, even when decisions feel restrictive.