Introduction

Construction job duties insurance approval often feels inconsistent for construction workers, especially when two people with the same title receive different insurance decisions. Two people can work on the same site, hold the same job title, and still receive very different insurance outcomes. One may face restrictions or exclusions, while the other does not. From the outside, this can seem arbitrary. In practice, it reflects how insurers interpret construction work.

Insurance approval in construction is shaped far more by what a worker actually does than by what their job title says. Titles provide a label. Duties reveal exposure. Insurers build decisions around the latter.

This article explains why job duties matter more than job titles when insurers assess construction workers. It focuses on how insurers break construction work into tasks, how frequency of risk affects approval, and why mixed or hands-on roles create complexity during underwriting. The goal is to make duty-based insurance decisions understandable, even when they feel frustrating.

Why Construction Job Duties Influence Insurance Approval More Than Job Titles

Job titles exist to describe roles within an organization. They help employers assign responsibility and workers identify their trade. Insurers use them only as an entry point.

In the context of construction job duties insurance approval, insurers focus on task-level exposure rather than job labels when classifying construction work.

A title such as “construction worker,” “site supervisor,” or “machine operator” does not provide enough detail to assess risk. Each of these roles can involve a wide range of activities, from low-exposure tasks to high-risk physical work. Insurers know that titles alone hide more than they reveal.

From an underwriting perspective, a title triggers questions rather than answers. It signals that construction-related exposure is likely, but it does not define how often, how intense, or how controllable that exposure is. Those details determine how risk is classified.

This is why insurance decisions often feel disconnected from titles. Insurers are not ignoring job descriptions. They are looking past them.

How Insurers Break Construction Work Into Duties

To assess construction risk, insurers deconstruct jobs into specific duties. Each duty is evaluated based on the type of exposure it creates and how frequently that exposure occurs.

Common categories insurers look at include:

-

Manual handling, such as lifting and carrying materials

-

Working at height, including ladders, scaffolding, and roofs

-

Machinery and tool operation

-

Environmental conditions, such as outdoor work or confined spaces

Each duty introduces different types of risk. Lifting creates long-term strain exposure. Working at height introduces fall risk. Machinery adds mechanical hazard. Environmental exposure affects predictability and control.

Insurers evaluate these duties individually and then consider how they combine. A role that involves one high-risk duty occasionally may be treated differently from a role that involves multiple high-risk duties daily. The cumulative effect matters.

This duty-based approach explains why two workers with the same title can receive different insurance decisions. The difference lies not in what they are called, but in how their workday is structured.

These task-level risks align with widely recognized construction workplace hazards, including fall exposure, machinery use, and changing site conditions that insurers consistently account for when assessing construction risk.

Why Frequency of Risk Matters More Than Occasional Tasks

One of the most important factors in insurance approval is how often a hazardous duty is performed. Occasional exposure and regular exposure are not treated the same way.

For example, a worker who climbs ladders once a month is assessed differently from a worker who does so every day. Even though the task is identical, the frequency changes the level of exposure and the likelihood of loss.

Insurers use frequency as a proxy for predictability. The more often a task is performed, the more likely it is that fatigue, repetition, or environmental variation will increase the chance of injury or impairment. This is especially relevant in construction, where physical demands accumulate over time.

This is also why mixed roles create complexity. A worker who splits time between lower-risk duties and higher-risk duties may not fit neatly into a single risk category. Insurers must decide which duties define the role, and that decision directly affects approval outcomes.

How Insurers Evaluate Physical Demands Like Lifting

Lifting is one of the most common and misunderstood construction duties from an insurance perspective. It is often viewed by workers as routine rather than hazardous. Insurers see it differently.

Manual handling creates cumulative exposure. Repeated lifting, even when done correctly, places ongoing strain on the musculoskeletal system. Injuries related to lifting are often gradual rather than sudden, making them harder to predict and manage.

Insurers assess not only the weight being lifted, but also how often lifting occurs, under what conditions, and whether it is sustained over long periods. A role involving constant material handling is evaluated differently from one where lifting is occasional or incidental.

This distinction matters because cumulative strain can lead to long-term impairment, which is costly and difficult to limit through policy design. As a result, lifting-heavy roles often attract stricter insurance treatment, regardless of how skilled the worker may be.

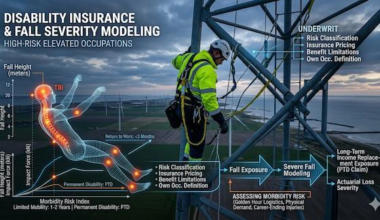

Working at Height and the Challenge of Severity

Working at height is another duty that carries disproportionate weight in insurance assessment. Falls are unpredictable, and when they occur, the consequences are often severe.

Insurers are less concerned with whether safety equipment is used and more concerned with the reality that even well-managed height work carries inherent risk. Equipment failure, environmental conditions, or momentary missteps can lead to significant injury.

From an underwriting standpoint, severity matters as much as likelihood. A low-probability event with high potential impact can influence approval more than a frequent but minor risk. Height-related duties fall squarely into this category.

This is why roles involving regular work at height are often classified more conservatively, even when safety standards are high and incidents are rare.

Machinery Operation and Mechanical Exposure

Operating machinery introduces a different type of risk. Mechanical hazards are often sudden and can involve both injury and property damage. Insurers account for the interaction between human operation, equipment condition, and site environment.

Machinery-related duties are evaluated based on the type of equipment, the level of operator control, and how often the machinery is used. Heavy equipment and power tools create higher exposure than hand tools, especially when used continuously.

Even experienced operators are subject to this evaluation. Skill reduces certain risks but does not eliminate mechanical exposure. Insurers focus on what could happen, not on how well tasks are usually performed.

Environmental Exposure and Variability

Construction environments are rarely static. Outdoor sites are affected by weather, terrain, and visibility. Indoor sites may involve confined spaces, incomplete structures, or temporary layouts.

Insurers view environmental variability as a risk multiplier. The less predictable the environment, the harder it is to control outcomes. This is why similar duties performed in different settings can lead to different insurance decisions.

A worker performing the same task in a controlled environment may be assessed differently from one doing it in changing or remote conditions. Environment shapes exposure, and exposure shapes approval.

Hands-On vs Supervisory Roles in Insurance Assessment

One of the clearest examples of duty-based classification is the distinction between hands-on and supervisory roles. Two workers may share a title such as “site supervisor,” but their daily activities may differ significantly.

A supervisory role focused on planning, coordination, and oversight typically involves lower physical exposure. A supervisory role that still includes regular hands-on work retains higher exposure.

Insurers assess which duties define the role in practice. Occasional site presence is not treated the same as daily physical involvement. This distinction explains why some supervisory workers face fewer restrictions than others with the same title.

Again, this is not a judgment about responsibility or importance. It is a reflection of exposure.

Why Mixed Job Duties Create Approval Challenges

Mixed-duty roles are common in construction. Workers often adapt to site needs, performing a range of tasks depending on the day. While this flexibility is valuable on site, it complicates insurance assessment.

Insurers prefer clearly defined roles because they allow for consistent classification. Mixed duties blur boundaries. When a role includes both low-risk and high-risk tasks, insurers must decide which duties dominate.

This decision affects approval outcomes. If higher-risk duties are frequent or essential, they tend to define the role. If they are rare or incidental, they may carry less weight. The challenge lies in determining where that line is drawn.

This is why mixed roles often experience inconsistent insurance outcomes. The complexity is not personal. It is structural.

The broader system behind these structural outcomes is explained in why construction workers are treated differently by insurance, which shows how insurers classify construction work long before individual duties are reviewed.

How This Fits Within Construction Workers Insurance

These duty-based assessments are a core part of how construction workers insurance functions. Insurance decisions are built around exposure patterns created by daily work, not around titles or seniority.

This approach reflects a broader principle within risk job insurance: occupational reality shapes insurance outcomes more than labels or assumptions. Construction makes this principle especially visible because duties vary widely even within the same role.

Understanding how insurers interpret job duties helps explain why approval decisions can differ so sharply between workers who appear similar on paper.

Final Note

This article does not suggest how duties should be described or how approval might be improved. Its purpose is clarity. When insurance decisions are understood as responses to exposure rather than judgments about individuals, duty-based outcomes become easier to interpret, even when they feel inconsistent.