Introduction: Why High-Risk Workers Are Declined or Restricted and What Those Decisions Actually Mean

For many high-risk workers, the most confusing moment in the insurance process is not the application itself, but the outcome.

Being declined, restricted, or postponed can feel personal. Workers often assume these decisions mean they are uninsurable, treated unfairly, or permanently excluded from coverage. In reality, these outcomes are common in dangerous work and are part of how insurance systems manage risk.

This guide explains why high-risk workers are sometimes declined, restricted, or postponed, what each outcome actually means, and how these decisions fit into the broader risk job insurance system.

What Decline, Restriction, and Postponement Mean

These three outcomes are often misunderstood, even though they represent very different situations.

A decline means coverage cannot be offered under current conditions because risk exceeds what the insurer can reasonably manage.

A restriction means coverage is offered, but with limits, exclusions, or modified terms related to specific risks.

A postponement means a decision is delayed until certain conditions change, such as recovery from an injury or stabilization of health.

Understanding the difference helps prevent unnecessary fear and incorrect assumptions.

Why high-risk workers are declined or restricted often comes down to how insurers assess exposure, recovery risk, and the limits of sustainable coverage.

These outcomes occur after initial eligibility is assessed, which we explain in detail in our guide on insurance eligibility for high-risk jobs.

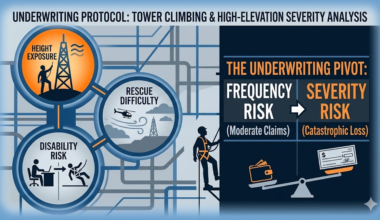

Why High-Risk Work Increases These Outcomes

Global workplace injury and recovery data published by the International Labour Organization shows that hazardous jobs involve higher injury severity and longer recovery periods, which increases the likelihood of restrictions or postponements during underwriting.

Insurance is built on predicting risk over time.

High-risk jobs increase:

-

The likelihood of injury or illness

-

The severity of outcomes

-

The complexity of recovery

When job risk combines with health factors, insurers must control exposure carefully. Declines, restrictions, and postponements are tools for managing this complexity.

These controls exist for the same reasons outlined in our guide on why high-risk jobs require special insurance rules.

These outcomes do not mean coverage is impossible; they mean risk must be aligned with realistic limits.

These decisions stem directly from how insurers evaluate exposure and recovery risk, which is explained in our guide on how insurers underwrite high-risk jobs.

When High-Risk Workers Are Declined

Declines occur when risk exceeds acceptable thresholds.

Common reasons include:

-

Extremely hazardous job duties

-

Recent serious injury or unresolved medical condition

-

Combination of high-risk work and health limitations

-

Insufficient information to assess exposure

A decline is often situational, not permanent. Changes in job duties, recovery status, or time can alter outcomes.

When Coverage Is Restricted

Restrictions are more common than declines.

Coverage may be offered with:

-

Exclusions for specific job tasks

-

Modified definitions of disability or injury

-

Limits on benefit amounts or duration

Restrictions allow coverage to exist while controlling exposure. For many high-risk workers, restricted coverage is the most realistic outcome.

When Applications Are Postponed

Postponement is often misunderstood as rejection.

It usually occurs when:

-

Recovery from injury is incomplete

-

A medical condition is unstable

-

Recent events make risk difficult to assess

Postponement reflects timing, not eligibility. Once stability is demonstrated, applications are often reconsidered.

Why These Decisions Feel Arbitrary

High-risk workers often compare outcomes and feel decisions are inconsistent.

This perception comes from:

-

Different insurer risk tolerances

-

Variations in job duties

-

Timing differences in health history

-

Differences between insurance types

What feels arbitrary is usually the result of different risk models, not random judgment.

How These Outcomes Fit Into Risk Job Insurance

Declines, restrictions, and postponements sit at the intersection of eligibility and underwriting.

They explain why:

-

Some workers are covered with limits

-

Others must wait

-

Some are declined temporarily

Most claim disputes and misunderstandings trace back to these decisions rather than to claim handling itself.

Conclusion: These Decisions Are About Risk, Not Worth

Being declined, restricted, or postponed does not define a worker’s value or future.

These outcomes are risk-management tools designed to align insurance coverage with real-world exposure. Understanding what they mean helps high-risk workers avoid fear-based assumptions and approach insurance with clarity rather than frustration.

This understanding completes the eligibility and underwriting foundation of risk job insurance.