Executive Summary

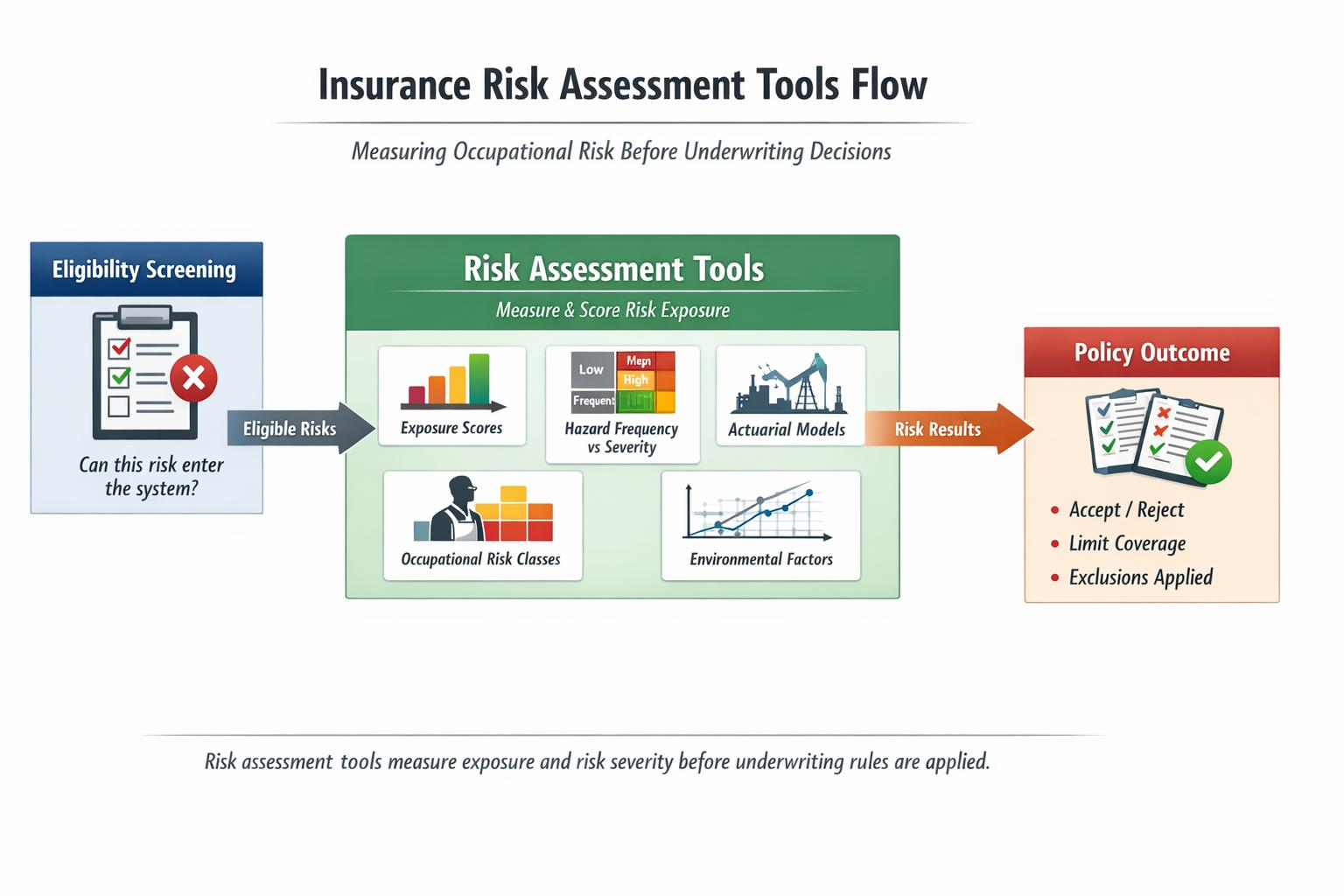

Risk assessment tools measure occupational exposure before underwriting decisions occur. According to actuarial modeling frameworks and occupational safety research, hazardous jobs produce highly variable loss outcomes, requiring structured risk measurement systems. These tools translate job duties, environments, and historical loss data into standardized signals that determine how underwriting rules will later apply.

Introduction

In insurance systems, risk assessment tools are mechanisms used to measure exposure, not to decide coverage. They translate complex, real-world hazards into structured signals that underwriting systems can process. For high-risk jobs, these tools are often the most decisive constraint in the entire insurance flow, shaping what underwriting can and cannot do long before a human reviewer becomes involved.

This article explains how insurers measure risk using structured tools and models, where those tools sit inside underwriting workflows, and why their outputs often feel rigid or impersonal, especially for dangerous occupations. It documents measurement logic and system limits, not qualification strategies or outcomes.

Within the Risk Job Insurance framework, this page serves as the primary reference for how insurers measure occupational risk before underwriting decisions are applied.

What “Risk Assessment Tools” Mean in Insurance

In insurance operations, risk assessment refers to structured risk measurement. These tools answer one question only:

How risky is this exposure, as defined by the system?

They do not answer:

-

Whether coverage will be offered

-

Whether a specific applicant qualifies

-

What price will be charged

Those decisions occur later, using the measurements produced here.

Risk assessment tools are distinct from:

-

Eligibility screening: Eligibility screening, explained in the Eligibility Requirements for Risk Job Insurance, determines whether a risk can enter the system at all.

-

Underwriting judgment (how rules are applied to measured risk)

-

Pricing models (how cost is assigned to accepted risk)

Confusing measurement with decision-making is the source of many misunderstandings around “risk-based” denials.

Where Risk Assessment Fits in the Insurance Flow

In most insurers, the flow is sequential and gated:

-

Eligibility gates

Determines whether the risk is even measurable by the system. -

Risk assessment tools

Quantify and categorize exposure using predefined models. -

Underwriting rules

Apply acceptance, limitation, or exclusion logic to those measurements.

Risk assessment sits between entry and decision. It does not approve or deny coverage, but it constrains every option that follows. If a risk exceeds model tolerances, underwriting discretion is often irrelevant.

Risk assessment tools operate as one stage within the broader underwriting system, sitting between eligibility screening and the application of underwriting rules, as explained in How Insurance Underwriting Works for High-Risk Jobs.

Types of Risk Assessment Tools Used by Insurers

Insurers rely on categories of tools rather than a single model. Common types include:

Exposure Scoring Models

Assign numeric or tiered scores based on task-level hazards, frequency, and intensity.

Hazard Frequency vs. Severity Matrices

Separate how often losses occur from how severe they are when they do, critical for dangerous work where severity dominates.

Occupational Risk Tables and Class Modifiers

Occupational Risk Tables and Class Modifiers translate job duties into standardized exposure categories, a process explained in occupation class ratings used by insurers.

Translate job duties into standardized risk classes that interact with broader actuarial assumptions.

Many risk assessment tools rely on occupational risk classification systems that group job duties into standardized exposure categories for modeling purposes, often using industry frameworks such as those maintained by NCCI for workers’ compensation.

These classification frameworks standardize how insurers interpret occupational hazards, ensuring that similar exposure patterns receive consistent risk measurements across different underwriting systems.

Actuarial Loss Projection Models

Estimate expected loss ranges based on historical data, adjusted for exposure characteristics.

Actuarial loss projection models rely on historical data and statistical methods to estimate future loss behavior, a core function of actuarial science.

Environmental and Situational Inputs

Account for context such as remoteness, offshore location, industrial setting, or transport dependency.

These tools are designed to be consistent, scalable, and defensible, not flexible.

Quantitative vs. Qualitative Risk Assessment

Quantitative Assessment

-

Automated

-

Numeric or categorical outputs

-

Threshold-driven

-

Often embedded directly into underwriting systems

These models dominate early-stage evaluation and frequently impose non-overridable ceilings for high-risk jobs.

Qualitative Assessment

-

Human-driven review

-

Narrative interpretation of duties and context

-

Used to interpret, not replace, model output

Hybrid Systems

Most insurers operate hybrids where human review exists but is constrained by quantitative limits. If a model flags catastrophic volatility, qualitative judgment may only confirm, not reverse the result.

How Job Risk Is Measured

Risk tools focus on what is done, not what a role is called. Measurement typically considers:

-

Actual job duties rather than titles

-

Hazard repetition (how often exposure occurs)

-

Hazard intensity (how damaging a single event can be)

-

Work environment (offshore, remote, industrial, mobile)

-

Task variability and uncontrolled exposure

For high-risk work, variability and lack of control often drive scores higher than the core task itself.

Non-Occupational Inputs That Affect Risk Scoring

Although job exposure dominates, many systems incorporate non-occupational signals at a structural level, including:

-

Age bands used for loss modeling

-

Prior injury or claim indicators as volatility signals

-

Physical or medical constraints as capacity assumptions

These inputs are not clinical evaluations or advice mechanisms. They exist to adjust loss projections, not to assess personal fitness.

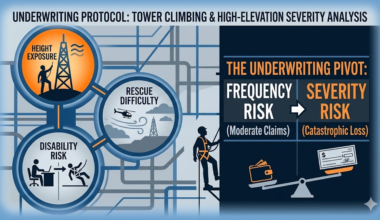

Why Risk Assessment Tools Are Stricter for High-Risk Jobs

As occupational danger increases, risk measurement models impose tighter thresholds because severe losses can destabilize insurance pools. This structural tightening explains why high-risk jobs face stricter insurance approval across most insurance systems.

-

Loss severity amplification overwhelms frequency-based assumptions

-

Volatility destabilizes pooled risk calculations

-

Catastrophic loss sensitivity forces conservative thresholds

-

Sparse or skewed data limits model confidence

As a result, generalized tools either over-restrict or fail entirely—leading insurers to impose hard limits rather than nuanced judgment.

Common Risk Assessment Failure Paths

Risk measurement systems commonly block underwriting progression when exposure exceeds predefined modeling thresholds. Typical failure points include:

• Misclassified job duties mapped to incorrect hazard classes

• Exposure levels exceeding model tolerance limits

• Mixed occupational roles that cannot be cleanly categorized

• Compounding occupational and personal risk indicators

• Environmental contexts associated with catastrophic loss volatility

When these thresholds are triggered, underwriting discretion is often removed entirely because the model output exceeds allowable exposure limits.

How Risk Assessment Shapes Underwriting and Claims

Risk assessment outputs determine:

-

Whether underwriting proceeds at all

-

Which exclusions or limitations are even permissible

-

How claims are later interpreted against assumed exposure

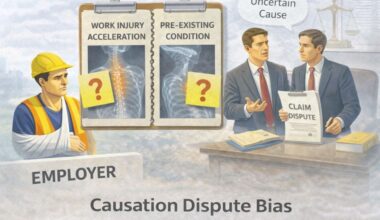

Claims disputes often trace back to mismatches between measured risk at underwriting and actual exposure at loss. The assessment becomes the reference point, even years later.

For how those measurements are operationalized, see the underwriting process explainer linked above.

Risk measurement is one stage within the broader insurance evaluation system for hazardous occupations. Related explanations include: