Executive Summary

High-risk occupations face stricter insurance approval because severe losses can destabilize insurance pools and capital reserves. According to insurance solvency frameworks and occupational safety research, hazardous industries generate low-frequency but high-severity claims. As risk severity increases, insurers narrow approval thresholds to protect capital, reinsurance agreements, and long-term pool stability.

Introduction: Approval as a System Constraint

Insurance approval often appears more restrictive in dangerous occupations, not because of individual circumstances, but because approval operates as a system-level control mechanism. As occupational danger increases, approval shifts from a flexible assessment to a tightly constrained decision governed by capital limits, loss tolerance, and aggregate exposure management.

This article explains why that tightening occurs. It does not address how approval is performed, how eligibility is determined, or how outcomes can be influenced. Those functions are documented separately in their respective canonical explanations. The focus here is structural: why approval rules become narrower as work becomes more hazardous.

This analysis explains why high-risk jobs face stricter insurance approval as occupational danger increases and underwriting tolerance narrows at a system level.

This structural role of approval is one component of the broader underwriting system explained in How Insurance Underwriting Works for High-Risk Jobs.

What “Approval” Means in Insurance Systems

Within insurance architecture, approval is a post-eligibility underwriting decision. Eligibility determines whether a risk can be considered at all. Approval determines whether that eligible risk can be accepted within defined system constraints.

Approval answers a narrow institutional question:

Can this risk be absorbed without breaching loss tolerance, capital protection rules, or pool stability thresholds?

This decision is governed by eligibility criteria for high-risk job insurance, where insurers translate occupational, medical, and exposure data into approval or decline outcomes.

It does not determine:

-

Whether coverage is legally allowed (eligibility)

-

What the premium would be (pricing)

Approval exists to protect the system, not to evaluate merit or effort. As risk severity increases, the margin for approval narrows accordingly.

Eligibility determines whether a risk may enter underwriting consideration at all, a distinction explained in detail in eligibility requirements for high-risk job insurance, where insurers define which risks can be evaluated in the first place.

Why Approval Standards Tighten as Risk Increases

Higher-risk occupations exert disproportionate pressure on insurance systems because they compress acceptable margins. When potential loss severity rises, insurers must assume that any accepted risk carries a higher probability of materially destabilizing outcomes.

As a result:

-

Tolerance for uncertainty declines.

-

Variance becomes less acceptable.

-

Approval thresholds move closer to hard limits.

In low-risk occupations, minor deviations can be absorbed without consequence. In dangerous work, similar deviations can produce losses that overwhelm reserves, disrupt reinsurance treaties, or impair future underwriting capacity. Approval tightens not to exclude individuals, but to prevent systemic stress.

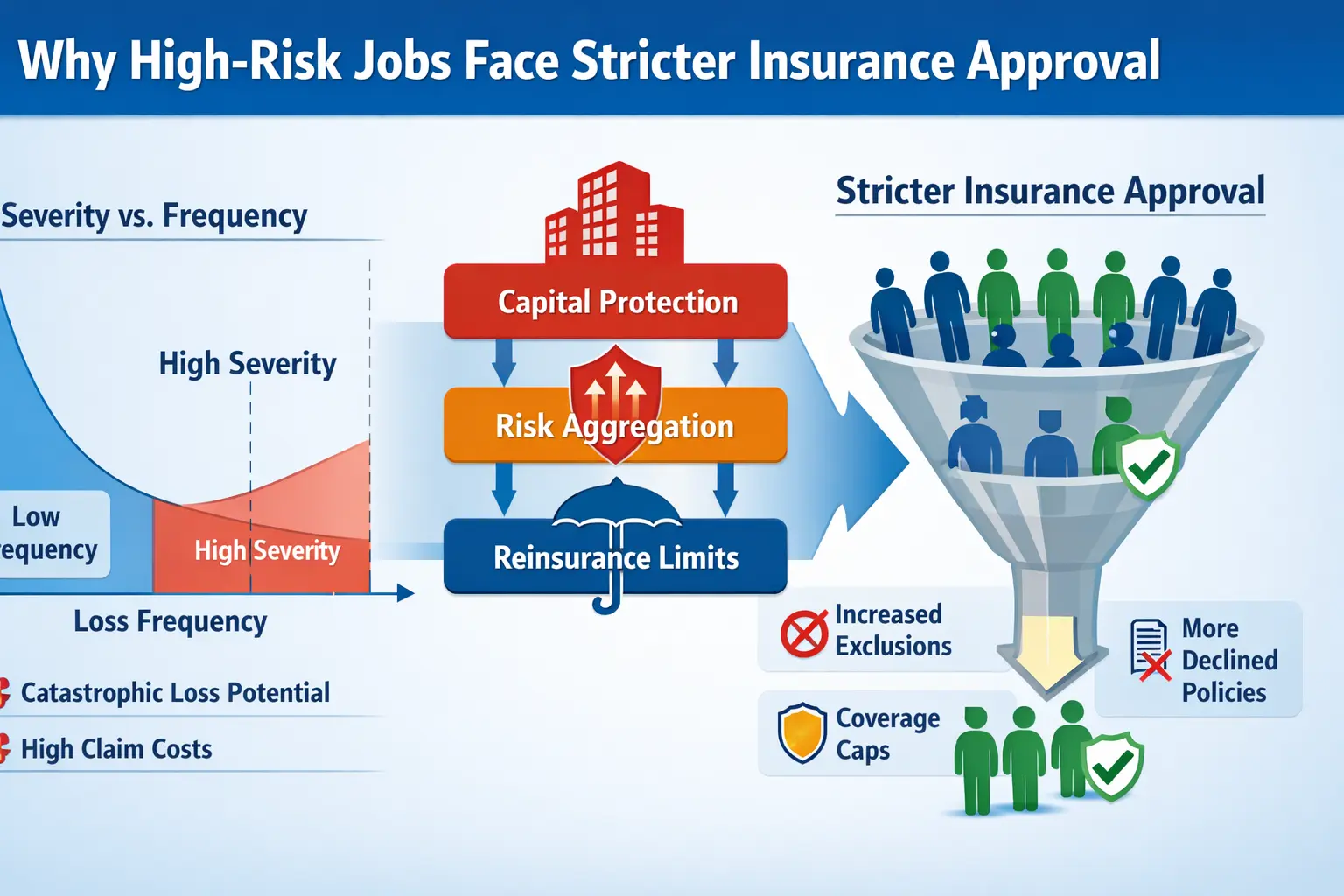

Severity vs. Frequency in High-Risk Occupations

High-risk jobs are often characterized by low claim frequency but extreme loss severity. This distinction is central to approval logic.

Frequent, low-severity losses can be modeled, pooled, and priced with relative stability. Severe losses, even if rare, introduce volatility that insurance systems are structurally designed to avoid.

From an actuarial perspective, severity-driven risk introduces tail exposure that cannot be diversified through volume alone. Insurers rely on structured risk assessment tools used by insurers to model catastrophic exposure and determine when approval thresholds must tighten under severity-driven risk conditions.

When a single claim can:

-

Exhaust a significant portion of pooled funds

-

Trigger reinsurance recoveries

-

Alter future underwriting assumptions

Approval gates become stricter. These gates exist to prevent a small number of severe claims from destabilizing the entire risk pool.

Capital Protection and Risk Pool Sustainability

Insurers operate under capital adequacy requirements designed to ensure long-term solvency. Approval rules are one of the primary mechanisms used to protect:

-

Statutory capital reserves

-

Contractual reinsurance arrangements

-

Multi-year pool sustainability

Insurance approval thresholds are aligned with capital adequacy frameworks used across regulated markets, including risk-based capital models that limit exposure to low-frequency, high-severity loss events. These models are designed to ensure solvency under stress scenarios rather than average conditions, which materially constrains approval tolerance for hazardous occupations.

Approval discipline is further shaped by reinsurance structures. Reinsurance treaties frequently impose attachment points, exclusions, and concentration limits that insurers must honor at the underwriting stage. When occupational risk profiles threaten treaty thresholds, approval standards tighten regardless of individual applicant characteristics.

These constraints operate within insurer risk appetite frameworks, where carriers define how much severe occupational exposure can be accepted without breaching capital or reinsurance limits.

High-risk occupational approvals are evaluated not only on expected loss, but on worst-case exposure. Even when probability is low, the magnitude of potential loss requires tighter controls.

Stricter approval is therefore a capital preservation function. It is designed to prevent concentration of exposure that could compromise the insurer’s ability to meet obligations across all policyholders.

Underwriting approval thresholds for hazardous occupations are aligned with risk-based capital requirements, which limit how much severe loss exposure insurers can carry while remaining solvent under stress scenarios.

Occupational Risk Aggregation Effects

Approval decisions are rarely isolated. These controls operate through standardized occupational classification systems that group workers according to exposure patterns and historical loss severity. These classifications determine whether approval discretion exists at all, since certain occupational classes exceed the tolerance limits embedded in insurer capital models.

High-risk roles tend to cluster within industries, worksites, or operational environments. This creates risk aggregation, where losses are correlated rather than independent.

Examples include:

-

Offshore crews exposed to shared operational hazards

-

Transport fleets subject to systemic accident patterns

-

Industrial teams working under uniform risk conditions

When similar roles produce correlated losses, insurers respond at the category level, not the individual level. Approval rules tighten across the occupation to prevent over-concentration, regardless of individual experience or history.

These category-level controls rely on standardized classification systems explained in occupation class ratings explained, where jobs are grouped based on loss severity and exposure patterns.

Why Manual Underwriting Has Limits in Dangerous Jobs

Manual underwriting discretion decreases as occupational risk increases. This is not a reflection of underwriter capability, but of system constraints.

At high severity levels:

-

Automated thresholds override human judgment

-

Reinsurance conditions impose non-negotiable limits

-

Capital models restrict discretionary acceptance

In these cases, underwriters may be unable to approve risks even when qualitative factors appear favorable. Discretion ends where system tolerance is exhausted. Caps, exclusions, or declines occur not because judgment fails, but because discretion is structurally limited.

In high-severity occupational classes, underwriting discretion is subordinate to system limits derived from capital modeling, reinsurance obligations, and historical loss development. Once these limits are reached, approval outcomes become deterministic rather than judgment-based.

Approval vs Exclusions vs Modified Coverage

Stricter approval does not always result in outright denial. Insurance systems employ multiple tools to preserve insurability while controlling exposure.

These include:

-

Conditional approvals, where acceptance is tied to defined constraints

-

Hazard-specific exclusions, removing exposure to the most severe risks

-

Benefit caps or waiting periods, limiting maximum loss impact

These mechanisms allow partial participation in the risk pool without exposing the system to unacceptable severity.

Common Approval Failure Paths for High-Risk Jobs

Certain structural conditions consistently lead to approval failure in dangerous occupations.

These include:

• Hazard severity exceeding modeled tolerance

• Combined occupational and personal risk load exceeding aggregate limits. These combined risk signals are often validated through occupational health reports, where medical conditions are assessed against job-specific exposure patterns to determine underwriting acceptability.

• Work environments associated with correlated catastrophic loss

• Industry-specific loss triggers identified through historical claims data

• Jurisdictional or regulatory conflicts affecting coverage scope

These failure paths are not discretionary decisions. They reflect predefined boundaries embedded in underwriting systems to prevent destabilizing exposure.

How Stricter Approval Shapes Claims Outcomes Later

Approval architecture influences downstream claims behavior. Conditions imposed at approval define how coverage is interpreted, how exclusions are enforced, and how claims are evaluated.

Stricter approval typically results in:

-

Narrower coverage interpretation

-

Heightened scrutiny of excluded hazards

-

Firm enforcement of caps and limits

Claims outcomes therefore reflect approval decisions made long before any loss occurs. This linkage is explored further in dedicated claims explainers, which build on the approval logic outlined here.

Understanding why approval becomes stricter in hazardous occupations requires viewing the full underwriting system:

Eligibility requirements for high-risk job insurance — defines which risks can enter the system at all.

Risk assessment tools used by insurers — explains how catastrophic exposure is modeled before approval.

Occupation class ratings explained — explains how jobs are grouped to control loss severity.

How insurance underwriting works for high-risk jobs — explains how all system components interact.