Introduction

At 4:30 a.m., before the first glimmer of sunrise touches the water, offshore workers are already gearing up for another demanding shift. Whether it’s a drilling engineer boarding a crew boat, a commercial fisherman checking gear before heading 60 miles offshore, or a diver preparing for deep-water inspection, these workers operate in environments far removed from everyday life. Their workplaces move with the waves. Their risks multiply with weather, machinery, isolation, and long-distance evacuation challenges.

Offshore work is, by every measure, high-risk employment, and that reality shapes the financial responsibilities these workers carry. Families depend on them not just emotionally, but financially. This is where Offshore Workers Life Insurance becomes an essential part of their protection.

This risk structure is part of the broader insurance for oil and gas workers system, which explains how offshore, industrial, and maritime work is insured across different policies.

This article breaks down exactly what this specialized coverage means, how it works, what it includes, what it excludes, and why it matters.

For a full overview of how life insurance fits into offshore and oil & gas risk, see our life insurance for offshore workers guide.

What Is Offshore Workers Life Insurance?

Offshore Workers Life Insurance is a specialized form of life insurance designed to protect individuals who work in hazardous maritime and offshore environments. Unlike traditional life insurance, which assumes relatively controlled and low-risk working conditions, this type of policy is built for workers facing elevated risks on oil rigs, vessels, remote offshore installations, and open waters.

Why It Differs From Regular Life Insurance

Traditional life insurance products often classify offshore work as high-risk, sometimes even uninsurable, due to factors such as:

-

Hazardous machinery

-

Extreme weather exposure

-

Helicopter and crew boat transport

-

Long stints away from immediate medical care

-

Deep-water environments

-

Explosive materials (oil & gas industry)

Because of these elevated hazards, insurers design policies that:

-

Offer higher coverage limits tailored to offshore risks

-

Provide accidental death and dismemberment benefits specific to offshore injuries

-

Evaluate job role, vessel type, and industry sector more closely

-

Include planned premium adjustments based on risk class

Offshore Workers Life Insurance bridges the gap between what standard life insurance covers and what offshore professionals actually face.

Why Offshore Workers Need Specialized Life Insurance

Offshore workplaces are some of the most unpredictable professional environments in the world. Even with top-tier safety training, the risks remain. Offshore workers fall under strict international safety and compensation regulations such as the Maritime Labor Convention (MLC 2006), which outlines employer responsibilities for worker protection and financial security.

Common Hazards in Offshore Work

Here are realities offshore workers confront almost daily:

-

Heavy machinery (cranes, drill pipes, winches)

-

Slip-and-fall hazards on wet decks

-

Explosive or flammable materials in oil and gas operations

-

Storms, high waves, and harsh marine weather

-

Helicopter transport risks

-

Equipment failure during diving or underwater operations

-

Remote location challenges where medical evacuation may take hours

Real-World Scenarios

-

A drilling crew member injured during a sudden pipe handling malfunction.

-

A seafarer lost during an unexpected storm surge.

-

A diver experiencing a critical equipment failure underwater.

-

A commercial fisherman involved in a vessel collision or capsizing.

These aren’t hypothetical. They represent situations offshore families worry about every time their loved one steps onto a boat or platform.

Offshore Workers Life Insurance helps address those fears by providing meaningful financial protection.

These occupational classifications come from the same framework described in risk job insurance, which explains how insurers group dangerous work before applying any policy.

How Offshore Workers Life Insurance Works

Although the core principles are similar to standard life insurance, offshore policies include unique considerations.

1. Policy Structure

Typical components include:

-

Base life coverage (lump-sum payout on death)

-

Accidental Death & Dismemberment (AD&D) specifically tailored to offshore risks

-

Optional riders for illness, disability, or evacuation

-

Risk-rated premium based on job type

2. Eligibility

Eligibility usually depends on:

-

Job classification (driller, diver, deckhand, fisherman, etc.)

-

Age and health status

-

Level of experience

-

Safety certifications

-

Employer’s safety history

Certain extremely high-risk jobs may require additional underwriting.

3. How Claims Are Paid

In the event of a covered death:

-

Beneficiaries submit a claim along with required documents (death certificate, employer report, policy details).

-

Insurer validates the cause of death.

-

Lump-sum payment is released once eligibility is confirmed.

4. Typical Beneficiaries

Most commonly:

-

Spouses

-

Children

-

Parents

-

Other dependents

Some employers also allow workers to designate an estate or trust.

Types of Coverage Available

Offshore Workers Life Insurance is not one-size-fits-all. Workers often combine several types to ensure comprehensive protection.

1. Term Life Insurance for Offshore Workers

Designed to provide financial security for a fixed period (10, 20, or 30 years), term life insurance is often the most affordable option.

Best for:

-

Offshore workers with younger families

-

Workers wanting high coverage at lower cost

-

Short-term offshore careers

Term life policies may require risk loading due to the offshore environment.

2. Whole Life Insurance Options

Whole life provides:

-

Lifetime coverage

-

Cash value growth

-

Potential borrowing options

It’s more expensive but offers long-term stability.

Best for:

-

Senior offshore workers

-

Workers planning estate protection

-

Individuals wanting lifelong financial planning

3. Accidental Death & Dismemberment (AD&D)

AD&D is especially important for offshore workers due to:

-

Machinery accidents

-

Vessel-related injuries

-

Fall hazards

-

Explosion risks

-

Diving-related injuries

Some policies include:

-

Loss of limb benefits

-

Loss of sight or hearing benefits

-

Partial disability benefits

4. Employer-Provided Group Policies vs Individual Plans

Employer-Provided Coverage

Many offshore companies offer group life coverage, but these usually have:

-

Limited benefit amounts

-

No portability if employment ends

-

Exclusions for specific offshore activities

Individual Plans

Provide:

-

Higher coverage

-

More flexibility

-

Custom riders

-

Long-term stability

Ideal Strategy

Most offshore workers benefit from both employer-provided coverage as a foundation, and individual coverage for complete protection.

5. Additional Riders

Common riders include:

-

Critical illness rider

-

Disability income rider

-

Emergency evacuation rider

-

Family protection rider

-

Accident upgrade rider

These expand coverage beyond basic life insurance.

What Offshore Workers Life Insurance Covers

Coverage varies by insurer, but typically includes:

1. Death Benefits

Paid in cases of:

-

On-the-job accidents

-

Non-work-related deaths

-

Illness (if included)

2. Job-Related Accidents

Including:

-

Machinery accidents

-

Falls

-

Helicopter crashes

-

Vessel incidents

3. Non-Job Related Incidents

Coverage often applies whether the worker is onshore or offshore at the time of death.

4. Medical Emergencies (Depending on Policy)

Some policies cover:

-

Emergency evacuation

-

Critical care

-

Treatment resulting from offshore hazards

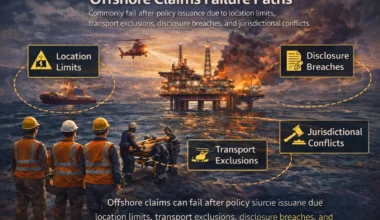

What Offshore Workers Life Insurance Does NOT Cover

Exclusions vary, but often include:

-

Death caused by alcohol or drug use

-

Intentional self-harm

-

Participation in criminal activities

-

War zones without special riders

-

Unauthorized offshore work

-

Failure to meet medical disclosure requirements

Common Misconceptions

Misconception: “My employer’s group life insurance is enough.”

Reality: Employer policies are usually limited and may end when employment ends.

Misconception: “All offshore workers are automatically covered.”

Reality: Some workers require specialized underwriting based on job risk level.

Cost of Offshore Workers Life Insurance

Factors That Influence Premiums

-

Age and health

-

Job category (divers, drillers, deckhands have different risk loads)

-

Years of experience

-

Employer’s safety record

-

Policy amount and length

-

Additional riders

Example Cost Range (General Estimate)

-

Younger workers (20s-30s): Moderate premiums

-

Mid-career workers: Higher premiums due to risk exposure

-

Divers and drillers: Highest premium category

Note: These are general educational observations, not financial advice.

How to Choose the Right Policy

Key Considerations for Offshore Workers

-

Does the policy explicitly cover offshore duties?

-

What incidents qualify for AD&D benefits?

-

Are both onshore and offshore risks covered?

-

How much coverage does your family realistically need?

-

Is the policy portable if you change employers?

Questions to Ask Insurers

-

How does my job classification affect premiums?

-

What offshore activities are excluded?

-

Can I add riders later?

-

Are helicopter or vessel transportation incidents covered?

-

Does the policy include evacuation benefits?

Important Clauses to Review

-

Occupational exclusions

-

Waiting periods

-

Risk-loading fees

-

Geographic limitations

Common Mistakes Offshore Workers Should Avoid

-

Relying solely on employer-provided coverage

-

Failing to disclose accurate job duties

-

Choosing the cheapest policy instead of adequate protection

-

Not reviewing exclusions

-

Forgetting to update beneficiaries

Employer-Provided vs Individual Offshore Workers Life Insurance

Employer Provided – Pros

-

Free or low-cost

-

Easy enrollment

-

Good baseline protection

Employer Provided – Cons

-

Not always portable

-

Limited payout

-

May exclude certain offshore roles

Individual Plans – Pros

-

Tailored coverage

-

Higher limits

-

Custom riders

Individual Plans – Cons

-

Higher cost

-

Requires full underwriting

Best Approach

Combine both to create a comprehensive safety net.

How to File a Claim

Step-by-Step Guide

-

Notify the insurer as soon as possible.

-

Submit the death certificate and employer’s incident report.

-

Provide policy documents and proof of beneficiary identity.

-

Insurer reviews and verifies the claim.

-

Beneficiaries receive the lump-sum payout once approved.

How Long Do Claims Take?

Most claims process within weeks, but offshore incident investigations may take longer.

Global and Regional Considerations

While this article maintains a neutral global tone, here are high-level differences:

United States

Strong regulatory oversight; offshore oil and gas workers need specialized riders.

United Kingdom / North Sea

Strict safety requirements; policies may factor in harsh weather risk.

Canada

Cold-water risks influence underwriting.

Middle East / GCC

Large expatriate offshore workforce; policies often tied to employer contracts.

Africa (Nigeria, Angola, Ghana)

Growing offshore sectors; insurers may require detailed job descriptions due to varied risk levels.

Common Myths About Offshore Workers Life Insurance

Myth 1: Offshore insurance is unnecessary because accidents are rare.

Truth: Offshore accidents remain significantly higher than most industries.

Myth 2: My employer will take care of everything.

Truth: Employer benefits may not fully protect families financially.

Myth 3: Premiums are unaffordable.

Truth: Many affordable options exist, especially term life plans.

Who Truly Needs Offshore Workers Life Insurance?

Workers in the following roles benefit the most:

1. Oil & Gas Workers

High exposure to machinery, explosive materials, and extreme weather.

2. Offshore Drillers

Risk from drilling equipment, drill floor hazards, and pipe movement.

3. Commercial Fishermen

One of the world’s most dangerous professions due to vessel risks and weather.

4. Marine Engineers & Technicians

Mechanical failures or confined space hazards increase risk.

5. Divers (Commercial, Saturation, and Inspection Divers)

Underwater work carries inherent life-threatening risks.

6. Offshore Construction Crews

Heavy machinery, cranes, and structural hazards increase injury probability.

7. Seafarers and Deckhands

Exposure to open waters, storms, and vessel collisions.

Conclusion

Offshore work is demanding, courageous, and critical to global industries but it is also undeniably high-risk. Offshore Workers Life Insurance provides the financial safety net that offshore professionals and their families need, ensuring that if the unexpected happens, loved ones are protected.

This type of coverage goes beyond standard life insurance. It accounts for real offshore hazards, from machinery and weather to transportation and remote location challenges. Whether you work on an oil rig, fishing vessel, dive crew, or shipping route, having the right insurance is not just wise, it’s essential.

By understanding what offshore life insurance includes, what it excludes, how it works, and how to choose the best policy, workers can make informed, confident decisions that safeguard their families’ futures.

If you’re an offshore worker or someone who loves one, having the right coverage brings peace of mind no matter how far from shore life takes you.