Introduction: When a Claim Doesn’t Go Through

Insurance claims denied in high-risk jobs are often misunderstood and feel personal, even though most denials follow clear policy rules. For many high-risk workers, a denied insurance claim is more shocking than an injury itself.

Construction workers, offshore crews, industrial operators, transport workers, and others in hazardous roles often assume that once a policy is active, benefits are guaranteed when something goes wrong. When a claim is denied, it can feel like betrayal, bad faith, or a system designed to avoid paying.

In reality, claim denials in high-risk jobs are common, but not for the reasons most workers assume.

This guide explains why insurance claims are denied in high-risk jobs, what those denials actually mean, and how they fit into the broader risk job insurance system. It is written to replace fear and suspicion with clarity.

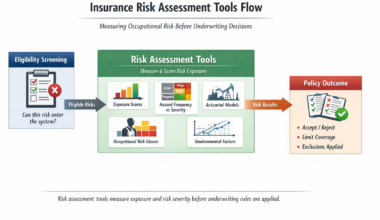

This article is part of our broader explanation of risk job insurance, where we show how eligibility, underwriting, pricing, and claims all connect. Claim denials make more sense when they’re viewed as one step in that larger system.

What a Claim Denial Really Is

A claim denial is not a judgment about a worker’s honesty or worth.

It is a determination that a specific claim does not meet the conditions defined in the policy. Insurance does not operate on intention or fairness. It operates on definitions, exclusions, and evidence.

In high-risk jobs, where claims are more frequent and more complex, those definitions are applied more strictly.

Understanding this distinction is essential. Most claim denials are about policy fit, not wrongdoing.

A denial does not always end the process. In some situations, workers can ask the insurer to review the decision. We explain the step-by-step process in our guide on how insurance appeals work for high-risk jobs, including when appeals actually succeed.

Many insurance claims denied in high-risk jobs happen not because insurers are unwilling to pay, but because the event doesn’t fit policy definitions.

Why Insurance Claims Denied in High-Risk Jobs Are More Common

These denial patterns align with occupational injury severity and recovery data published by the International Labour Organization, which shows higher long-term impact in hazardous jobs.

High-risk work increases both the likelihood of claims and the cost when claims occur. This combination forces insurers to apply policy terms carefully.

Industries involving heavy machinery, physical labor, hazardous environments, or remote locations experience:

-

More frequent injuries

-

More severe outcomes

-

Longer recovery periods

-

Greater risk of permanent impairment

Global occupational injury data from the International Labour Organization consistently shows that hazardous work accounts for a disproportionate share of serious injury and long-term disability.

Because exposure is higher, insurers must ensure that only claims that clearly fall within coverage terms are paid. This increases denial frequency compared to low-risk work, even when policies are active.

Denials often follow the same review process explained in why insurance claims are scrutinized more closely in high-risk jobs, where exposure increases verification requirements.

The Most Common Reasons Claims Are Denied

Claim denials in high-risk jobs tend to fall into predictable categories.

1. The Event Falls Outside Coverage Definitions

Insurance policies are written using precise definitions. If an injury, illness, or loss does not meet those definitions, the claim may be denied.

Common examples include:

-

Injuries classified as gradual rather than accidental

-

Conditions not meeting the policy’s definition of disability

-

Events occurring outside covered timeframes

These denials often surprise workers because the injury feels real and severe, even if it does not meet policy language.

2. Occupational Exclusions Apply

Many policies for high-risk jobs include exclusions related to specific duties, environments, or activities.

Examples include:

-

Certain types of machinery use

-

Offshore or remote work not disclosed at application

-

Temporary duties outside declared roles

When a claim involves an excluded activity, denial is often automatic, regardless of severity.

3. Job Duties Do Not Match What Was Disclosed

Underwriting decisions are based on how work was described during application.

If a claim reveals that actual duties were more hazardous than disclosed, insurers may deny coverage on the basis that the risk insured was not the risk experienced.

This is one of the most common and emotionally charged denial reasons, even when no misrepresentation was intentional.

These discrepancies often trace back to how insurers underwrite high-risk jobs, where coverage terms are built around disclosed duties and environments.

4. Medical Evidence Does Not Support the Claim

Claims require documentation.

Denials may occur when:

-

Medical records do not support functional limitation

-

Recovery timelines do not align with policy definitions

-

Independent assessments contradict treating providers

In physically demanding jobs, proving inability to work can be more complex than proving injury.

5. Policy Conditions Were Not Met

Some denials are procedural rather than substantive.

Examples include:

-

Late notification

-

Missing documentation

-

Failure to follow required treatment protocols

These denials feel especially frustrating because they are not about the injury itself, but about process.

Why Denial Does Not Mean the System Is Broken

From the worker’s perspective, a denial feels final. From the insurer’s perspective, it is part of enforcing policy boundaries.

Denials exist to:

-

Apply coverage consistently

-

Control exposure in high-risk environments

-

Prevent policies from becoming unsustainable

Without strict boundaries, insurance for dangerous jobs would become unavailable or unaffordable for everyone in the risk pool.

This does not make denials painless, but it explains why they exist.

Eligibility rules for hazardous work, explained in insurance eligibility for high-risk jobs, set the initial boundaries that later influence claim outcomes.

How Denials Fit Into Risk Job Insurance as a System

Claim denials are not isolated events. They are the visible outcome of earlier decisions.

Eligibility determines whether coverage can exist.

Underwriting defines what risks are accepted.

Pricing reflects exposure.

Claims enforce those rules.

Denials occur when a claim falls outside them.

Most claim disputes trace back to misunderstandings at earlier stages, not to the claim itself.

What a Denial Actually Means for the Worker

A denial does not always mean:

-

The policy is useless

-

Future claims will fail

-

The worker is uninsurable

It often means:

-

The claim does not fit this policy

-

Evidence was insufficient

-

Definitions were narrower than expected

Understanding this distinction is critical before assuming bad faith or permanent exclusion.

For some workers, the next step is appealing the decision. But appeals do not always succeed, especially in dangerous occupations. We explain this in detail in our guide on why insurance appeals fail in high-risk jobs, so workers understand what realistically changes, and what doesn’t, during an appeal.

Conclusion: Denial Is a Boundary, Not a Judgment

Insurance claim denials in high-risk jobs are structural, not personal.

They occur because dangerous work changes how strictly policies must be applied. Understanding why denials happen helps workers avoid fear-driven conclusions and prepares them to evaluate next steps with clarity.

This understanding sets the foundation for what happens next: first, whether an appeal makes sense, and then what to do if the dispute continues. In some situations, disagreements move beyond the insurer entirely, which we explain in our guide on when insurance disputes escalate to complaints, regulators, or legal action.

Understanding denials is the first step. Only after that does it make sense to look at whether an appeal is realistic, and what happens if the dispute doesn’t stop there.

For a full picture of how claims fit into the entire system, see our main guide: Risk Job Insurance Explained.