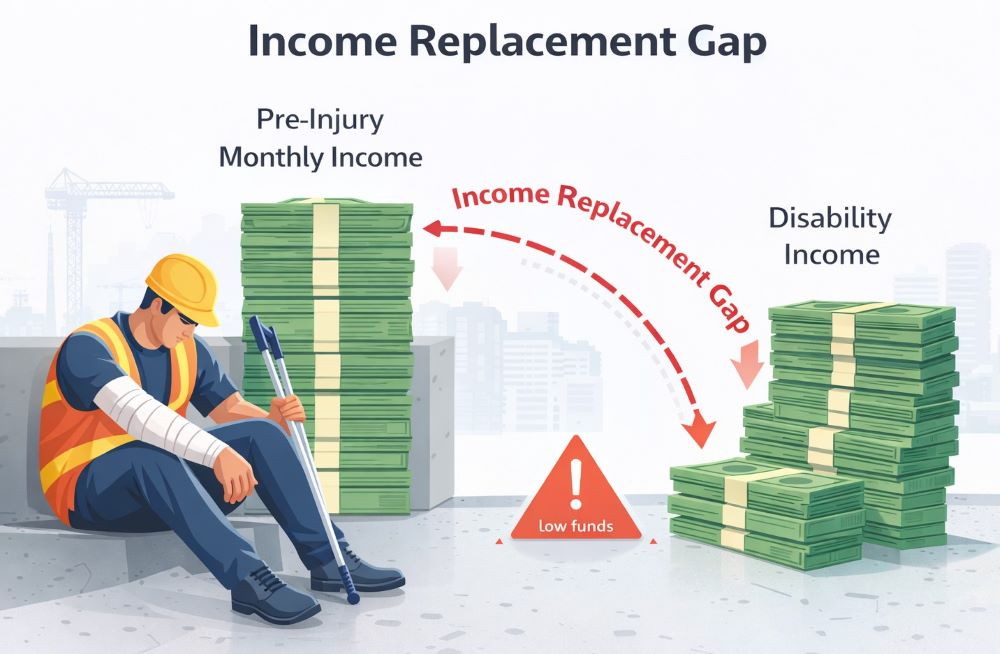

Income Replacement Gap – Definition

Income replacement gap refers to the shortfall between a high-risk worker’s pre-injury earnings and the actual income received during disability, after insurance benefit caps, offsets, exclusions, and duration limits are applied.

Income replacement gaps emerge after coverage activation and reflect adequacy failures rather than eligibility or claims approval issues.

In Risk Job Insurance, this gap arises when benefits technically activate but fail to replace enough income to sustain the worker during occupational disability, forcing reliance on savings, debt, or premature return-to-work decisions.

How the Income Replacement Gap Forms

Income replacement gaps typically emerge due to a combination of:

-

Benefit percentage caps that underrepresent high-risk earnings

-

Maximum monthly benefit limits that truncate payouts

-

Partial disability reclassification, reducing benefit amounts

-

Benefit duration limits that end payments before recovery

-

Offsets from workers’ compensation, social programs, or employer benefits

Individually these mechanisms appear reasonable.

Collectively, they create a material income shortfall.

Income Replacement vs Disability Status

The income replacement gap is independent of disability eligibility.

A worker may be:

-

Fully recognized as occupationally disabled, yet

-

Still experience severe income loss due to benefit inadequacy

This distinction explains why many valid claims still result in financial instability, even when coverage is technically honored.

Even when disability is formally recognized, generalized disability income replacement standards often fail to account for the wage structure and recovery realities of high-risk occupations, resulting in persistent income shortfalls.

Common Income Replacement Failure Paths

Income replacement gaps are most often triggered when:

-

Policies cap benefits below realistic high-risk wage levels

-

Partial disability classifications reduce payout percentages

-

Delayed claim approval consumes benefit time without payment

-

Benefit periods expire before occupational recovery

-

Cost-of-living adjustments are absent during long claims

These failures disproportionately affect workers with physically indivisible roles and limited redeployment options.

Why the Income Replacement Gap Is Amplified in High-Risk Jobs

High-risk occupations magnify income replacement gaps because:

-

Wages reflect hazard exposure, not interchangeable labor

-

Light-duty or alternative work pays substantially less

-

Licensing, certification, or safety restrictions limit job mobility

-

Early return-to-work increases reinjury and claim termination risk

As a result, even short-term income gaps can cause long-term financial damage.

Relationship to Other Risk Job Insurance Systems

Income replacement gap directly interacts with:

Together, these systems determine whether disability coverage preserves livelihood or merely delays financial collapse.

Key Takeaway

Income replacement gap is not about whether benefits are paid; it is about whether income is actually replaced.

In Risk Job Insurance, unaddressed gaps turn valid coverage into incomplete protection.

Income Replacement Gap is a documented concept within the Risk Job Insurance framework, indexed in the Definitions Hub, and positioned at the intersection of the Claims System and Benefits Structure clusters that govern disability payouts and income continuity.