Claims finality and enforcement outcomes in Risk Job Insurance (RJI) refer to the point at which a claim decision becomes binding, non-reviewable, and operationally enforced across the insurance system.

Once finality is reached, the claim outcome, approval, partial payment, or denial is no longer subject to internal appeal, and enforcement mechanisms are triggered to close the file, allocate loss, and protect underwriting integrity.

In RJI, finality is not administrative closure. It is system lock-in.

How Claims Reach Finality in RJI

Claims progress toward finality through a controlled sequence:

-

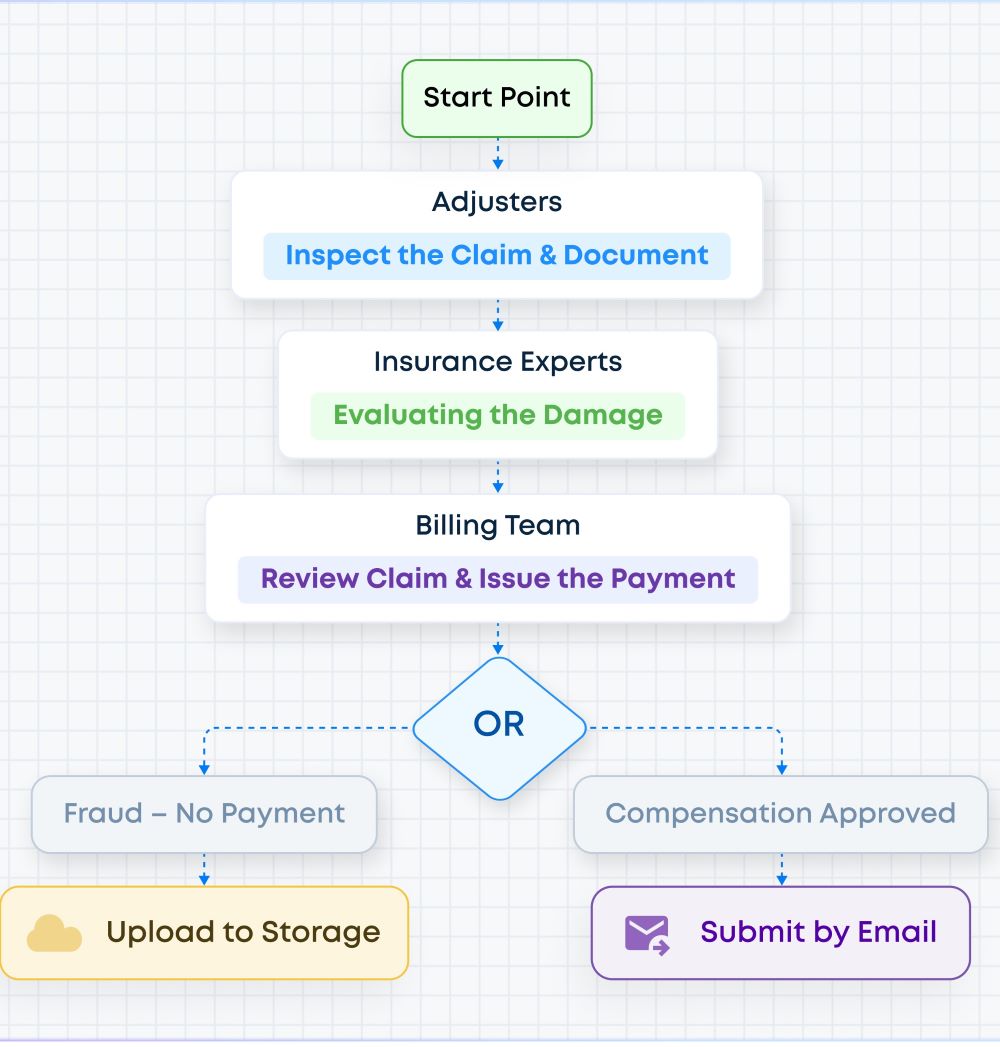

Qualification assessment

-

Adjudication and denial or approval

-

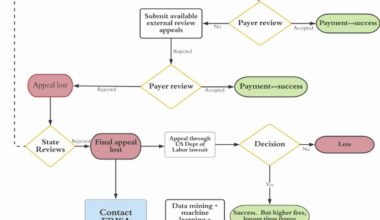

Appeals and dispute resolution (if applicable)

-

Final enforcement decision

This sequence is structurally dependent on:

-

Claims Qualification Criteria

-

Claims Denial

-

Claims Appeals & Dispute Resolution

Finality occurs only after all permitted review pathways are exhausted or time-barred.

What Permanently Closes at Finality

When a claim reaches finality:

-

Claim review authority permanently ends

-

Coverage determination cannot be revisited

-

No new evidence can be introduced

-

Payment status becomes fixed

-

The claim lifecycle cannot be re-entered

At this point, enforcement replaces evaluation entirely.

What Enforcement Means in Risk Job Insurance

Once a claim is final:

-

Payment decisions are executed or permanently refused

-

Reserves are released or crystallized

-

Subrogation or recovery rights are triggered (if applicable)

-

The policy record is updated for future underwriting

Enforcement ensures that risk assumptions made at underwriting remain intact after loss, even when outcomes are unfavorable to the worker.

Why Finality Is Stricter in High-Risk Insurance

Risk Job Insurance cannot allow indefinite reconsideration.

Because high-risk losses are:

-

Statistically concentrated

-

Severity-heavy

-

Exposure-sensitive

Finality protects:

-

Pool solvency

-

Program viability

-

Pricing accuracy

This is why appeals in RJI are finite by design, not open-ended.

When Finality Cannot Be Reopened

A finalized claim cannot be reopened due to:

-

Financial hardship

-

Injury severity escalation

-

Employer pressure

-

New legal arguments unrelated to policy error

Reopening is possible only if:

-

Fraud is discovered

-

Clerical or classification error is proven

-

Regulatory mandate intervenes

Otherwise, enforcement stands.

The same finality and enforcement constraints described here can be observed in large-scale insurance programs such as Owner Controlled Insurance Programs (OCIPs), where claims decisions ultimately reach a non-reviewable state governed by program rules and centralized control.

Why Claims Finality Matters in RJI

Finality explains why many workers perceive insurance as:

-

Inflexible

-

Unresponsive

-

Unfair

In reality, the system is operating exactly as structured.

Understanding finality clarifies:

-

Why appeals have limits

-

Why denials persist

-

Why enforcement overrides emotion

This definition forms part of the broader Risk Job Insurance framework, which explains how high-risk coverage systems are structured, enforced, and administered across occupations.

This entry is part of the Risk Job Insurance Definitions hub, which organizes and explains the core systems, terms, and mechanisms that govern high-risk insurance coverage.