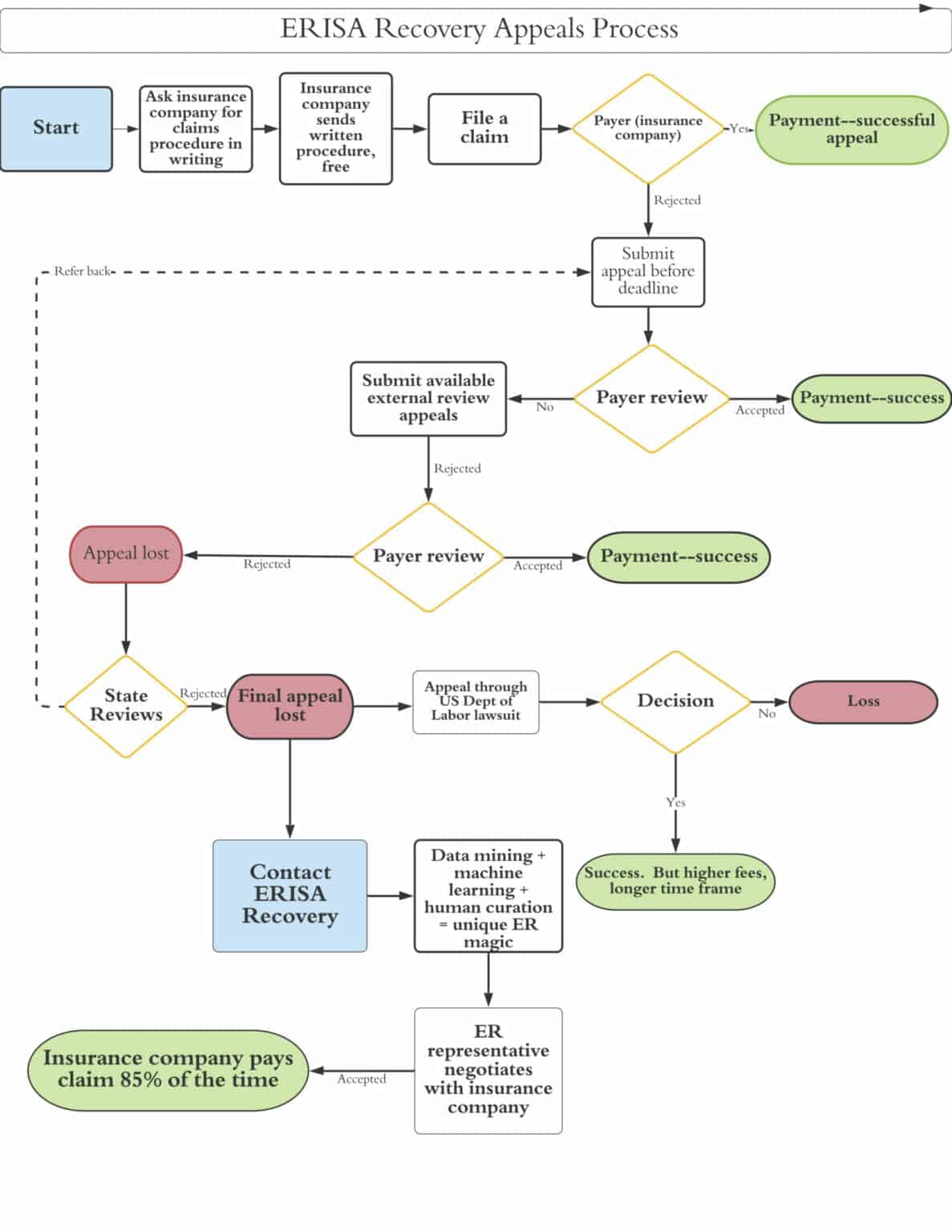

Claims appeals, and dispute resolution in Risk Job Insurance (RJI) refer to the formal mechanisms available to challenge a denied claim, where the policyholder seeks reconsideration, correction, or external review of an insurer’s adjudication decision.

In RJI, appeals do not re-litigate the injury itself. They test whether the claim was denied according to policy structure, eligibility rules, and documented evidence, not fairness, hardship, or intent.

Appeals exist to correct procedural or interpretive failures, not to override risk controls.

Why Appeals Exist in Risk Job Insurance

Risk Job Insurance relies on tight enforcement systems. Because claims denial is often the expected outcome when qualification thresholds fail, insurers must also provide controlled challenge pathways to:

-

Maintain regulatory compliance

-

Correct classification or documentation errors

-

Defend the integrity of underwriting systems

Appeals therefore function as a system audit layer, not a customer service feature.

This logic follows directly from Claims Denial, where denial is a structural enforcement outcome.

Common Grounds for Appeals in RJI

Appeals are only viable when the denial can be challenged on system grounds, such as:

1. Documentation Reevaluation

-

New or corrected incident reports

-

Verified employment or contract status

-

Third-party confirmation previously unavailable

2. Eligibility Misclassification

-

Incorrect worker classification

-

Policy enrollment timing errors

-

Improper application of eligibility gating

(Closely tied to Eligibility Gating.)

3. Policy Interpretation Disputes

-

Ambiguous exclusion language

-

Misapplied coverage triggers

-

Incorrect policy layer assignment

These disputes often trace back to misunderstanding Risk Job Insurance Policy Structure, not insurer misconduct.

What Appeals Do Not Do

This distinction is critical.

Appeals do not:

-

Create coverage that never existed

-

Override activated exclusions

-

Reclassify risk after loss

-

Convert non-covered activities into covered ones

If denial resulted from designed policy enforcement, the appeal will fail, even when injury severity is extreme.

Internal vs External Dispute Resolution

Internal Appeals

-

Conducted by the insurer or program administrator

-

Review original decision for procedural accuracy

-

Most RJI appeals terminate here

External Dispute Resolution

-

Regulatory review

-

Arbitration or mediation

-

Legal escalation

External resolution is rare in RJI and typically pursued only when system misapplication, not risk enforcement, can be demonstrated.

The appeal and dispute resolution mechanisms described here mirror processes observable in large-scale insurance programs such as Owner Controlled Insurance Programs (OCIPs), where claims decisions are formally reviewable but remain constrained by eligibility and scope controls.

What Remains Constrained During an Appeal

While an appeal is under review:

-

Benefit payment remains suspended

-

Coverage obligation does not reactivate

-

Claim evaluation does not expand beyond the appeal scope

-

No new coverage determinations are created

An appeal does not reopen the claim lifecycle.

It temporarily reviews a denial decision within tightly defined procedural limits.

Why Appeals Matter in RJI Understanding

Appeals reveal where insurance systems allow correction, and where they do not.

For high-risk workers, misunderstanding appeals leads to:

-

False expectations of reversal

-

Delayed financial planning

-

Escalation without legal basis

Understanding appeals properly reinforces the core RJI principle:

Insurance systems correct errors, not risk.

This definition forms part of the broader Risk Job Insurance framework, which explains how high-risk coverage systems are structured, enforced, and administered across occupations.

This entry is part of the Risk Job Insurance Definitions hub, which organizes and explains the core systems, terms, and mechanisms that govern high-risk insurance coverage.

Related Definition