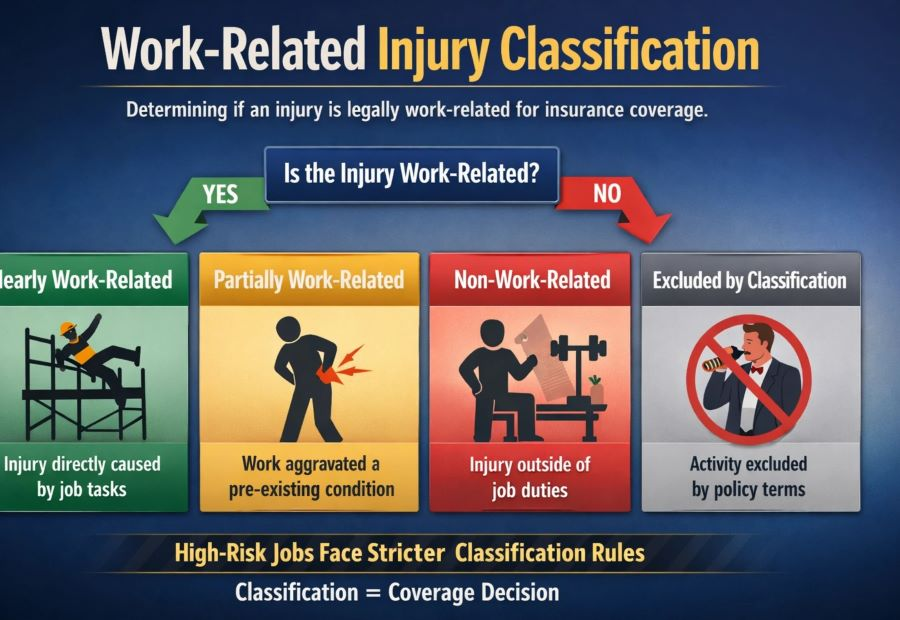

Work-Related Injury Classification is the insurer’s formal process for deciding whether an injury legally and contractually qualifies as work-related for coverage, claims payment, and liability assignment, especially critical in high-risk jobs.

This classification determines which policy responds, what benefits apply, and whether a claim is paid at all.

What it actually means

An injury is considered work-related only if it meets specific, provable criteria set by policy language, underwriting rules, and jurisdictional law, not just because it happened “at work” or while wearing PPE.

Insurers typically assess:

-

Causation – Did job duties materially cause or aggravate the injury?

-

Time & place – Did it occur during compensated work hours or authorized tasks?

-

Scope of employment – Was the worker performing assigned or expected duties?

-

Jurisdictional rules – Local law definitions override assumptions.

-

Policy exclusions & endorsements – High-risk roles often face tighter definitions.

Common injury classification categories

Insurers usually place injuries into one of four buckets:

-

Clearly work-related

Directly caused by job tasks (e.g., fall from scaffolding during assigned work). -

Partially work-related (contributory)

Work aggravated a pre-existing condition; coverage may be reduced or disputed. -

Non-work-related

Injury occurred at the workplace but outside job duties (often denied). -

Excluded by classification

Injury tied to activities excluded for that occupation or risk tier.

Why this matters more for risk-job workers

High-risk occupations face narrower classification tolerance because:

-

Severity-based underwriting increases scrutiny

-

Job misclassification voids coverage faster

-

Cross-jurisdiction or offshore work creates ambiguity

-

Insurers aggressively test causation thresholds

In practice, classification, not injury severity, is the first denial trigger for risk-job claims.

Where classification breaks down (failure paths)

This is where most denials happen:

-

“At work” ≠ “work-related”

Location alone does not establish coverage. -

Informal tasks

Helping outside assigned duties can void classification. -

Pre-existing condition overlap

If medical history isn’t clearly separated, insurers may reclassify. -

Jurisdiction mismatch

Injury occurred under a different legal regime than the policy assumes. -

Role drift

Worker performed higher-risk tasks than declared at underwriting.

How insurers prove (or disprove) work-relatedness

Evidence typically includes:

-

Incident reports & time logs

-

Job descriptions vs. actual tasks

-

Medical causation opinions

-

Witness statements

-

Contractual scope documents

Missing or inconsistent documentation often results in reclassification → denial.

Key takeaway

Work-Related Injury Classification is not intuitive, emotional, or injury-centric.

It is a legal-underwriting determination that decides coverage before benefits are even considered, especially unforgiving for high-risk workers.

Related definitions

- Severity-Based Underwriting

-

Scope of Employment (Insurance Context)

-

Claims Eligibility Thresholds