Underwriting compression is what happens when insurance systems are forced to simplify how they evaluate high-risk jobs because detailed risk analysis is too expensive, too slow, or too uncertain.

It is not better underwriting.

It is less precise underwriting applied to more dangerous work.

For high-risk workers, this often means being treated as a category, not as an individual.

What Underwriting Compression Means

In low-risk insurance, underwriters can afford to:

-

Review duties

-

Consider safety records

-

Adjust pricing

-

Customize terms

In high-risk insurance, losses are larger and margins are thinner.

So insurers compress the process:

-

Fewer variables

-

Broader classifications

-

More default exclusions

-

Less customization

That shortcutting is underwriting compression.

Why High-Risk Jobs Trigger It

High-risk work creates:

-

High claim volatility

-

Long tail losses

-

Uncertain causation

Insurers cannot afford deep, individualized analysis for every worker.

So they rely on:

-

Occupational codes

-

Industry buckets

-

Standardized rules

Precision is replaced by categories.

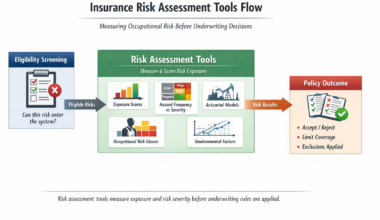

Underwriting compression forces insurers to rely heavily on occupational risk classification instead of individualized job analysis.

Actuarial organizations such as the Society of Actuaries develop the risk models that drive simplified underwriting rules.

How This Affects Workers

Underwriting compression means:

-

Two very different workers may be treated the same

-

Safe practices are not rewarded

-

Unique situations are ignored

-

Policies feel unfairly rigid

The system is not judging effort.

It is managing uncertainty.

These compressed rules help maintain risk pool segmentation by keeping volatile jobs out of standard insurance markets.

Why Appeals Rarely Work

Once compressed rules are applied, there is little room to negotiate.

The system does not know who you are, it only knows what category you belong to.

In the Risk Job Insurance System

Underwriting compression explains why:

-

High-risk workers feel misclassified

-

Policies look one-size-fits-all

-

Exceptions are rare

It is how insurers survive volatility, by reducing complexity.