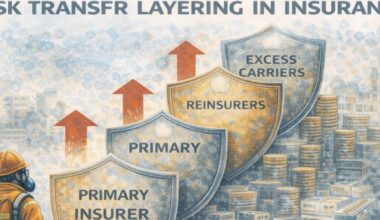

Reinsurance dependence is the degree to which an insurance company relies on other insurers to absorb losses from high-risk jobs before it is willing to offer coverage.

It is not about the worker.

It is about how much risk the insurer itself can survive.

For high-risk workers, coverage often exists only because someone else is standing behind the insurer.

What Reinsurance Dependence Means

Most insurers do not keep all the risk they sell.

They pass large or volatile losses to reinsurers, companies that insure the insurers.

High-risk occupations create:

-

Large claims

-

Unpredictable losses

-

Clustered events

These overwhelm a single carrier’s balance sheet.

So coverage is written only when reinsurers agree to take most of the exposure.

That reliance is reinsurance dependence.

Global reinsurers such as Swiss Re provide the capital and risk-sharing that make high-risk insurance markets possible.

Why High-Risk Jobs Trigger It

Office workers produce small, spread-out losses.

Construction, offshore, mining, and industrial work produce large, spiky losses.

Insurers cannot price that reliably on their own.

So they need:

-

Reinsurance approval

-

Reinsurance limits

-

Reinsurance exclusions

Without it, the policy does not exist.

Because high-risk workers are isolated through risk pool segmentation, insurers must rely heavily on reinsurers to support those smaller, volatile pools.

How It Affects Coverage

When a policy is reinsurance-dependent:

-

Terms are stricter

-

Exclusions are heavier

-

Limits are lower

-

Renewals depend on reinsurance markets

Workers never see this layer, but it controls everything.

If reinsurers pull back, coverage disappears.

When reinsurance support changes, it often triggers coverage fragility, causing policies to be restricted or non-renewed even when workers have done nothing wrong.

Why Coverage Can Vanish Suddenly

Many high-risk workers think their insurer cancelled them.

In reality, the reinsurer left.

And when that happens, the insurer cannot legally or financially continue the policy.

In the Risk Job Insurance System

Reinsurance dependence explains why:

-

High-risk insurance is fragile

-

Markets harden quickly

-

Entire job classes lose coverage at once

It is the invisible backstop behind almost every high-risk policy.