Introduction: When a Claim Is Denied After Approval

Insurance claims denied in high-risk jobs often come as a shock, even when coverage has been approved and premiums are up to date. For many high-risk workers, the most confusing moment in the insurance process comes after approval. A policy is active. Premiums are paid. Coverage exists. Then a claim is filed, and denied.

This experience often feels personal. Workers assume denial means they did something wrong, misled the insurer, or were never truly covered. In dangerous jobs, that assumption is common, and usually incorrect.

Construction workers, offshore crews, industrial operators, transport workers, and others in hazardous roles experience claim denials more frequently than average-risk workers. Not because they are less honest, but because high-risk work changes how insurance claims are evaluated.

This guide explains why insurance claims are denied in high-risk jobs, what those denials actually mean, and how they fit into the broader risk job insurance system.

What a Claim Denial Actually Is

A claim denial is not a reversal of approval.

It is a determination that a specific event does not meet the policy’s conditions for payment. Denials are based on policy language, definitions, exclusions, limits, and documentation, not on intent or effort.

A denial answers one question only:

Does this specific event fall within the boundaries of coverage as written?

This distinction matters because many workers assume denial means coverage never existed. In reality, coverage may exist broadly while still excluding or limiting specific outcomes.

Common Reasons Insurance Claims Are Denied in High-Risk Jobs

Most claim denials in dangerous work fall into predictable categories.

Mismatch between job duties and disclosures

If actual duties differ from what was described during application, insurers may determine that the risk was not insured as presented.

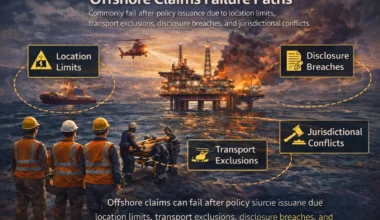

Exclusions triggered

High-risk policies often exclude certain tasks, environments, or conditions. If an injury occurs within an excluded scenario, the claim may be denied even though the policy is active.

Policy definitions not met

Disability, injury, or incapacity must meet precise definitions. Being unable to perform a specific job does not always meet the policy’s definition of inability to work.

Limits already reached

A claim may be denied because benefit limits were exhausted, not because coverage failed.

Insufficient documentation

High-risk claims require detailed medical, occupational, and timing evidence. Gaps or inconsistencies can lead to denial.

These reasons are structural, not moral.

At claim time, insurers compare what happened against the original risk assessment, using the same framework described in how insurers underwrite high-risk jobs.

Why High-Risk Jobs Experience More Claim Denials

High-risk work changes the insurance equation.

Dangerous jobs involve:

-

Higher injury frequency

-

More severe outcomes

-

Longer recovery periods

-

Greater financial exposure

When claims are more likely and more expensive, insurers apply stricter verification. This results in closer examination of facts, definitions, and documentation.

According to global occupational injury data published by the International Labour Organization, hazardous industries experience higher rates of serious and long-term injury. Insurance systems respond by enforcing boundaries more tightly.

This is why denials occur more often in high-risk jobs, not because insurers expect fraud, but because exposure is higher.

How Underwriting Decisions Reappear at Claim Time

Claims do not exist in isolation.

At claim time, insurers revisit:

-

Job duties disclosed during underwriting

-

Risk classifications applied

-

Exclusions and limits set in advance

If the claim scenario does not align with underwriting assumptions, denial becomes more likely.

This is why underwriting decisions made months or years earlier often feel suddenly relevant during a claim. Claims enforce underwriting; they do not reinterpret it.

Many claim disputes trace back to how coverage was approved in the first place, which is why understanding insurance eligibility for high-risk jobs helps explain why some claims face closer review than others.

Why Denials Often Feel Arbitrary

Many high-risk workers compare experiences and feel outcomes are inconsistent.

This perception usually comes from:

-

Different insurers using different risk thresholds

-

Variations in job duties within the same title

-

Timing differences (recent injury vs long-term stability)

-

Different policy structures

What feels arbitrary is often the result of different risk models, not random judgment.

These differences are not random; they exist for the same structural reasons explained in why high-risk jobs require special insurance rules, where dangerous work changes how insurers manage risk and enforcement.

What a Claim Denial Does and Does Not Mean

A denial does not mean:

-

You were dishonest

-

You are uninsurable

-

Coverage never existed

-

The decision is always final

A denial does mean:

-

The event did not meet policy conditions

-

A boundary was enforced

-

Further review may be possible

Understanding this distinction prevents panic and helps workers respond rationally rather than emotionally. When a denial occurs, the next step is understanding insurance appeals for high-risk jobs, where decisions are reviewed based on evidence rather than assumptions.

How Claim Denials Fit Into Risk Job Insurance

Within the risk job insurance system:

-

Eligibility determines whether coverage can exist

-

Underwriting defines acceptable risk

-

Pricing reflects exposure

-

Exclusions and limits set boundaries

-

Claims apply those rules

-

Denials enforce them

Denials are not failures of the system. They are how the system maintains alignment with real-world risk.

Conclusion: A Denial Is a Signal, Not a Verdict

For high-risk workers, insurance claim denials are common, confusing, and emotionally difficult. But they are not personal judgments or proof that coverage was meaningless.

Denials signal that a boundary was reached, not that protection never existed.

Understanding why claims are denied helps workers interpret outcomes accurately, decide whether further action makes sense, and prepare for the appeals and disputes process that follows.

That is where the next guide begins.

This closer review process is explained further in our guide on why claims are scrutinized more closely in high-risk jobs, where enforcement reflects exposure rather than suspicion.