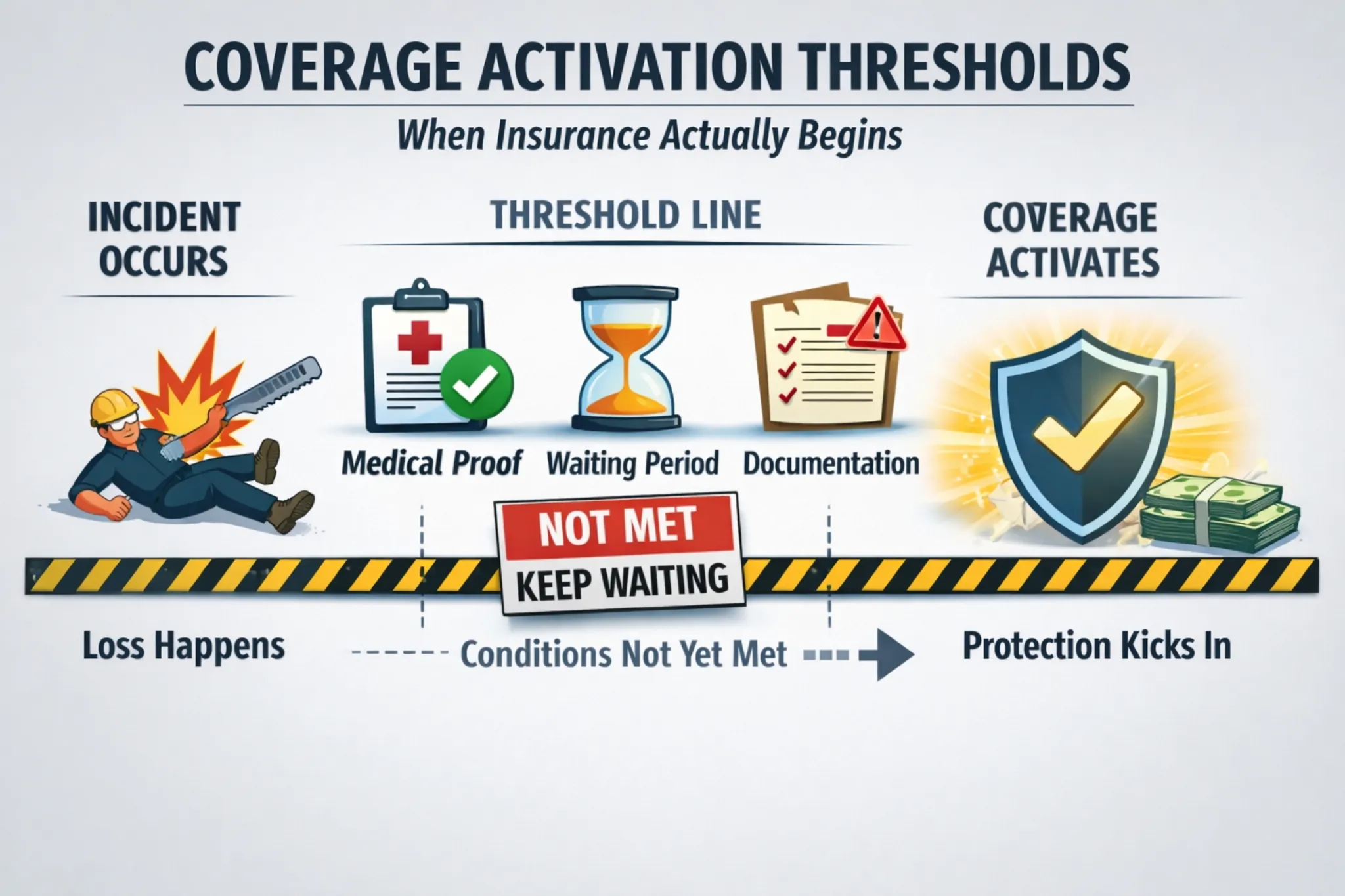

Coverage activation thresholds are the minimum conditions that must be met before insurance coverage officially begins to respond to a loss.

It is not about eligibility.

It is about when protection turns on.

For high-risk workers, coverage often exists in theory but activates only after a defined line is crossed.

What Coverage Activation Thresholds Mean

Insurance does not always respond at the moment something goes wrong.

Instead, many policies require thresholds such as:

-

A minimum injury severity

-

A waiting period

-

Proof of causation

-

Medical confirmation

-

Documentation completeness

Until those thresholds are met, coverage remains inactive.

That trigger point is the coverage activation threshold.

These thresholds help explain coverage latency, where insurance exists but does not respond immediately after a loss.

Why High-Risk Insurance Uses Thresholds

High-risk claims are expensive and complex.

To control exposure, insurers design policies so that:

-

Minor or ambiguous incidents are filtered out

-

Only qualifying losses activate benefits

-

Early-stage costs stay with the worker

Thresholds act as gates, not safeguards.

How This Affects Workers

Coverage activation thresholds mean:

-

Delays before benefits begin

-

Early medical or wage costs paid out-of-pocket

-

Disputes over whether a threshold was reached

Workers experience this as coverage “hesitating” under pressure.

Why Thresholds Are Often Confused

Thresholds are rarely explained clearly.

They are scattered across:

-

Definitions

-

Conditions

-

Claims procedures

Workers assume coverage is immediate until they hit the threshold wall.

Insurance regulators such as the National Association of Insurance Commissioners describe how benefit triggers and waiting periods affect when coverage activates.

In the Risk Job Insurance System

Coverage activation thresholds explain why:

-

Coverage latency exists

-

Claims stall early

-

Insurance feels conditional even after approval

They are the switch that determines when insurance actually starts working.

When thresholds are enforced rigidly, they often combine with coverage conditionality to delay or limit protection for high-risk workers.

This concept is part of the broader Risk Job Insurance Definitions, which explain how insurance systems treat high-risk work.