Introduction

Construction workers treated differently by insurance are not being judged individually, but classified based on how occupational risk is structured within insurance systems.

Construction workers are often surprised by how insurance responds to their work. Coverage may be restricted, delayed, limited, or denied in ways that feel inconsistent with effort, experience, or responsibility on the job. Two workers may perform similar roles, face similar hazards, and still receive very different insurance outcomes.

This difference is central to how construction workers insurance functions, where occupational exposure shapes coverage long before any policy detail is considered.

This is not because construction workers are careless, uninsurable, or treated unfairly by default. It is because insurance systems do not evaluate work the way workers experience it.

Insurance does not respond to effort, professionalism, or visible danger. It responds to risk structure. Construction work sits in a category where risk is continuous, physical, and difficult to segment. That reality shapes how insurers classify, limit, and design coverage long before any individual worker applies.

This article explains why construction workers are treated differently by insurance, focusing on insurer logic rather than outcomes. It does not explain specific policies or tell workers what to do. Its purpose is to establish the framework that explains why later insurance decisions often feel unintuitive or frustrating.

This explanation supports the broader foundation of construction workers insurance and fits within the system-level logic of risk job insurance, where occupation shapes coverage behavior more than personal history.

This article explains why insurance systems treat construction work conservatively. For how those systems operate in practice, see how insurance systems actually work for construction workers.

Why Construction Workers Are Treated Differently by Insurance Systems

When construction workers say they are treated differently, they usually mean one of the following:

-

Coverage is harder to qualify for

-

Restrictions or exclusions appear unexpectedly

-

Similar workers receive different outcomes

-

Insurance does not respond the way work risk feels

From an insurance perspective, “different treatment” does not mean discrimination. It means different classification.

Insurance systems exist to group risk into categories that behave predictably over time. Construction work introduces volatility that is difficult to isolate, quantify, or compartmentalize. As a result, construction is often flagged early in underwriting and evaluated more conservatively across systems.

This conservative treatment is structural, not personal.

Why Construction Work Triggers Early Risk Classification

Construction is consistently classified as high risk due to its physical demands, environmental variability, and severity potential, factors reflected in official construction occupational risk exposure research.

Insurance systems assess risk before coverage exists. For construction workers, classification happens early because construction combines several characteristics insurers track closely:

-

Physical exposure

-

Environmental variability

-

Severity potential

-

Cumulative strain

-

Limited task substitution

Construction is not dangerous because incidents happen frequently. It is classified as high-risk because when things go wrong, outcomes can be severe, and because physical demands compound over time.

Insurance systems are designed to protect against unpredictable loss. Construction work introduces multiple forms of unpredictability at once.

This early classification is the reason many workers encounter restrictions or denials before policy details are even discussed, a process explained further in why construction workers struggle to qualify for insurance.

Why Job Titles Matter Less Than Exposure

One of the most confusing aspects of insurance treatment in construction is the weak role of job titles.

From a worker’s perspective, a title defines responsibility, skill, and trade identity. From an insurer’s perspective, a title is only a starting signal.

Insurance evaluates:

-

What tasks are performed

-

How often hazardous duties occur

-

Whether exposure is occasional or continuous

-

How controllable the environment is

This is why two workers with the same title may be treated very differently. The difference is not who they are, but how their workday is structured.

This duty-based logic explains why construction insurance outcomes often feel inconsistent even within the same site or role.

This task-based evaluation is why construction job duties affect insurance approval far more than job titles or trade labels.

Why Skill and Experience Do Not Neutralize Risk

Construction workers often assume that experience, training, and safety awareness should improve insurance outcomes. On site, these qualities matter deeply. In insurance systems, they matter far less.

Insurance operates at scale. It cannot reliably price individual judgment, caution, or professionalism. Instead, it prices exposure.

An experienced worker and a new worker performing the same duties face the same underlying hazards from an insurer’s point of view. Skill may reduce incident likelihood, but it does not eliminate exposure to height, machinery, or physical strain.

This is why insurance decisions can feel disconnected from personal history. The system is not evaluating character or competence. It is evaluating structural risk.

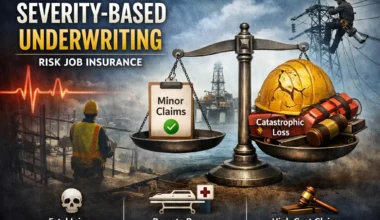

Why Construction Risk Is Hard to Contain Inside Insurance Systems

Insurance works best when risk can be:

-

Clearly defined

-

Time-limited

-

Isolated to specific events

Construction work challenges all three.

Many construction injuries are not tied to a single incident. They develop gradually through repetition, strain, or environmental exposure. Employment arrangements are often temporary or layered. Duties change by project phase.

Insurance systems are built around definitions and boundaries. Construction work frequently crosses those boundaries, creating gaps where coverage becomes uncertain or fragmented.

These gaps are not accidental. They reflect a mismatch between how construction work operates and how insurance systems are designed.

Why Construction Workers Encounter More “Gray Areas”

Construction workers are more likely than many others to encounter gray areas in insurance because:

-

Risk accumulates over time

-

Injuries may be aggravated rather than caused by work

-

Duties are mixed rather than fixed

-

Employment relationships shift frequently

Insurance systems rely on clean categories: work vs non-work, able vs unable, covered vs excluded. Construction rarely fits cleanly into those categories.

When work reality and policy definitions diverge, outcomes feel confusing. The confusion is structural, not the result of misunderstanding or error by the worker.

How This Explains Common Construction Insurance Frustrations

This foundational logic explains why construction workers often experience:

-

Difficulty qualifying for coverage

-

Denials that feel technical or disconnected

-

Restrictions that appear unrelated to effort or safety

-

Inconsistent outcomes between similar workers

These outcomes are not judgments about individuals. They are the result of how insurance systems manage exposure they cannot easily segment or control.

This is why construction workers treated differently by insurance often experience outcomes that feel inconsistent compared to lower-risk occupations.

These frustrations often stem from assumptions that insurance responds intuitively to risk, a disconnect explored in common insurance misconceptions construction workers learn the hard way.

Understanding this framework makes later system-specific behavior easier to interpret.

How This Fits Within Construction Workers Insurance

This article establishes the foundation for understanding construction workers insurance as a whole.

Each insurance system, whether employment-based, income-based, or event-based, applies its own definitions to construction risk. Those systems behave differently, but they all begin from the same premise: construction work carries structural exposure that must be managed conservatively.

Within the broader logic of risk job insurance, construction makes insurer boundaries visible. It shows where systems protect themselves rather than mirror occupational reality.

Final Note

This article does not explain how to qualify for insurance, improve outcomes, or avoid restrictions. Its purpose is clarity.

Construction workers are treated differently by insurance not because of who they are, but because of how their work concentrates physical exposure, severity potential, and unpredictability. Insurance systems respond to that structure long before individual stories are considered.

Once this is understood, later insurance decisions, however frustrating, become easier to interpret. Not because they feel fair, but because they follow a logic that is consistent, even when it is restrictive.